April 30, 2026

We can almost solve freelancer payments in Pakistan. All we need is one ambitious CEO.

The SBP just cleared the last big regulatory hurdle. The offshore infrastructure exists. The corridor is proven. What is missing is not law or technology. It is willpower.

April 30, 2026

Let me start with a confession. I am not a global payments expert. I have not run a bank, built a payment gateway, or negotiated a Visa acquiring agreement. What I am is someone who has watched this particular problem sit unsolved for the better part of two decades, who spent some time recently trying to understand why, and who believes the honest answer is no longer "the regulation won't allow it." It is closer to "nobody has tried hard enough."

This piece is an initial attempt to map a path leading to a solution. If someone who actually knows this space reads it and tells me three of my assumptions are wrong, I would consider that a win. The goal is to move the conversation from "this is complicated" to "here is a possible shape of a solution, let us stress test it."

With that said:

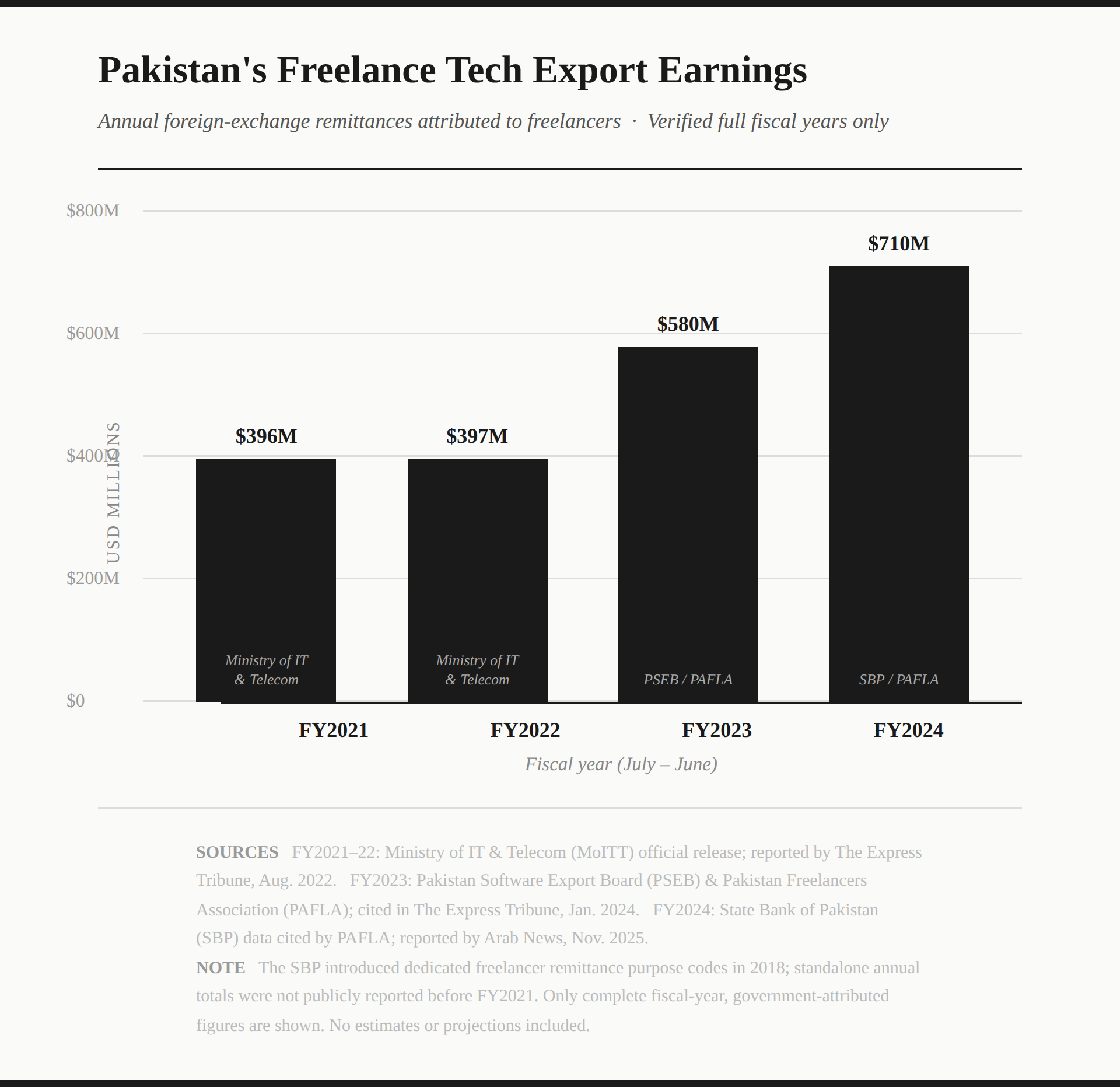

Pakistan has approximately 2.4 to 4 million freelancers (including full time and part time), making it one of the largest freelance workforces in the world. In the first half of FY2025-26 (July–December 2025), Pakistani freelancers collectively earned a record $557 million in foreign exchange, a strong 58% increase compared to the same period last year. Full year earnings for FY2025-26 are on track to approach or exceed $1 billion.

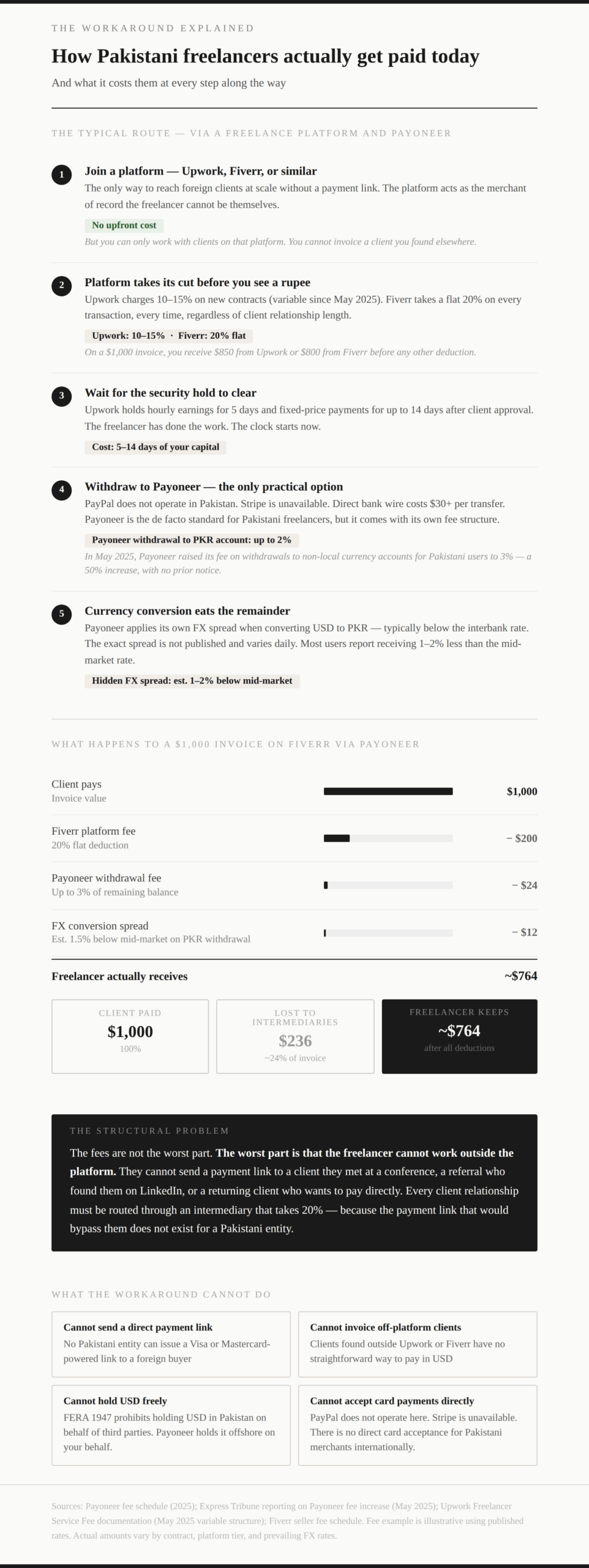

The growing freelancer earnings have clearly been a point of pride for anyone involved. Ministers invoke these numbers at every digital economy summit. The SBP has issued circular after circular in their name. And yet, in 2026, a Pakistani freelancer who wants to send a payment link to a client in Austin still cannot do it. Not from a Pakistani entity. Not through Pakistani infrastructure. The closest thing available is a Payoneer account, which is an American company giving you a virtual US bank account so you can pretend, for the purposes of getting paid, that you do not live in Pakistan.

The growing freelancer earnings have clearly been a point of pride for anyone involved. Ministers invoke these numbers at every digital economy summit. The SBP has issued circular after circular in their name. And yet, in 2026, a Pakistani freelancer who wants to send a payment link to a client in Austin still cannot do it. Not from a Pakistani entity. Not through Pakistani infrastructure. The closest thing available is a Payoneer account, which is an American company giving you a virtual US bank account so you can pretend, for the purposes of getting paid, that you do not live in Pakistan.

This is not just a minor inconvenience, it is a structural tax on every knowledge worker in the country. The details of how a Pakistani freelancer actually gets paid today is mapped in the infographic below:

The actual problem

The actual problem

Let us get one thing straight: the issue has never really been receiving money. SWIFT, the Society for Worldwide Interbank Financial Telecommunication, is a secure, global messaging network used by financial institutions to send information and instructions for cross-border transactions. It does not transfer funds directly but acts as a trusted, standardized system for directing money transfers between banks worldwide.

It is available and works in Pakistan.

The Exporters' Special Foreign Currency Account (ESFCA) facility introduced by the State Bank of Pakistan (SBP) was designed for freelancers and IT exporters to receive, hold, and manage foreign currency. It allows freelancers to retain up to 50% of earnings in foreign currency. The SBP's remittance channels have handled billions in inflows for years.

Receiving has never been the problem.

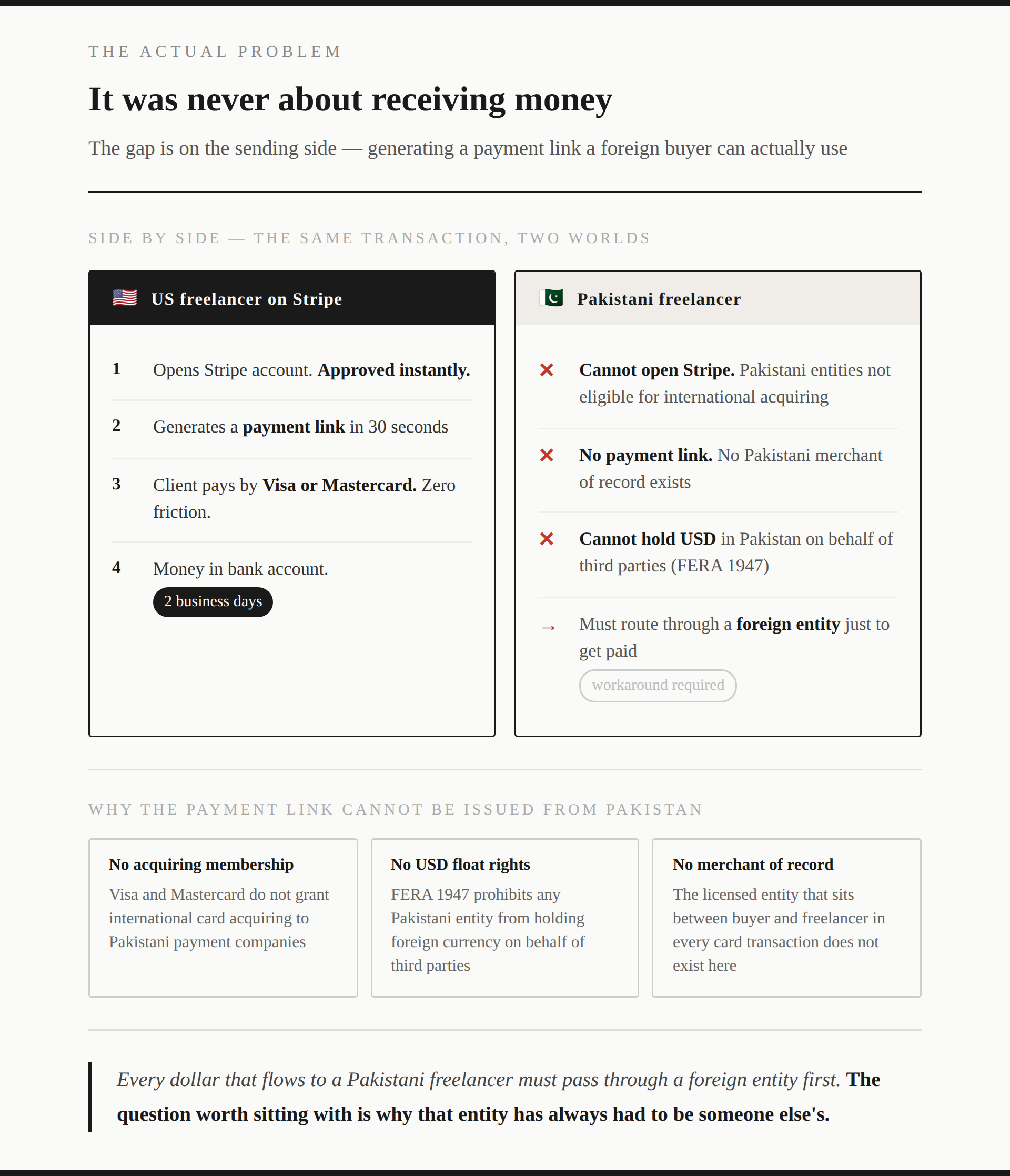

The problem is that foreign clients do not get the same easy payment experience they are used to elsewhere. In many countries, a freelancer or business can create a Stripe payment link in seconds. The client pays by card or bank transfer, the payment is processed smoothly, and the money reaches the seller without the client having to think about banking complications.

Pakistani freelancers cannot offer that same experience. This is because Pakistan does not have a locally recognised payment company that can act as a merchant of record for international card payments, hold foreign currency on behalf of users, and then settle the money into Pakistani bank accounts. Visa and Mastercard do not allow Pakistani payment companies to directly acquire international card payments in this way, while Pakistan’s foreign exchange rules also restrict companies from holding dollar balances for third parties. As a result, payments to Pakistani freelancers usually have to pass through a foreign company first. The real question is why Pakistan has never built its own system to do this.

What the SBP just changed and what’s missing

On April 6, 2026, the SBP issued two circulars, FECL6 and FECL7, that quietly resolved the single biggest operational bottleneck in this space.

They abolished Form R on a per transaction basis.

For context, Form R was the documentation freelancers had to submit for every single incoming foreign payment. Every invoice settled meant a separate form, manually filed, constantly causing delays and lost payments. The SBP has replaced all of that with a single declaration at account opening. From that point, incoming IT export receipts flow without per transaction paperwork.

The same reforms mandated one day processing for inward export receipts, standardized documentation requirements across all banks so the rules are the same everywhere, raised the enhanced reporting threshold to $25,000, and allowed ESFCA debit cards for direct USD spending on international services.

The ESFCA framework already permits 50% retention of export proceeds in foreign currency, with a floor of $5,000 per month, and no SBP approval is required for business expenses paid from that balance.

The receiving pipe is now as clean as it has ever been in Pakistan's history. The SBP has done its initial part. What remains is the sending side. The payment link. The merchant of record. The offshore entity that takes a foreign buyer's card payment and routes it cleanly into a Pakistani freelancer's ESFCA.All this, needs new laws. Till legislative changes happen we need innovative and legally compliant solutions that help us solve this for free lancers fast. The natural question is, what still remains to be done, and how is it being done across the border in India? Let’s first address that before we get into non-legislative solutions using existing optionality. The comparison can be seen in the infographic below:

The Saudi model and why it deserves a closer look

Now, there have been workarounds to this that many in the freelancing and IT exports space in Pakistan have been using to make payments easier for their clients. One model that has been common in fintech circles for some time goes roughly like this: You register a UAE free zone company, obtain a Stripe account, and use that entity as the front end for Pakistani freelancers. This works at a basic level. But I do not think it is the most strategic version of the idea for two reasons.

Firstly, Stripe is not the only rail. Airwallex, now incorporated in Saudi Arabia following Ministry of Investment approval in September 2025, offers multi currency accounts, global payment acceptance, and payment links that are in some ways better suited to a sub merchant model than Stripe. Checkout.com, Adyen, and Worldpay offer comparable products. The payment link function is a vendor choice that can be revisited. The entity structure and the jurisdiction are the strategic decisions that matter.

Second, Saudi Arabia has a claim to being a better jurisdiction than Dubai for this specific purpose, and I think this part of the argument is genuinely underappreciated.

Saudi Arabia sends more money to Pakistan than any other country on earth. In October 2025 alone, Saudi remittances to Pakistan reached $820 million. Over the first four months of FY2025 26, the Kingdom contributed $3.13 billion to Pakistan's inflows. The corridor between Saudi Arabia and Pakistan is the single most liquid, most trusted, most SBP seasoned money pipe that exists.

When money arrives from Saudi Arabia, the entire Pakistani financial system is calibrated to receive it without friction. The correspondent banking relationships are fifty years deep, rooted in the Gulf labour migration corridor. The SBP's purpose code infrastructure is fully mature for this flow. Pakistani banks have dedicated teams for processing Saudi inflows. A UAE free zone structure carries more scrutiny at the Pakistani end because such structures are sometimes associated with opaque corporate ownership arrangements. A Saudi entity with a genuine business presence does not carry that association in the same way.

A Saudi company registered as an IT services and digital payments entity can open accounts with Airwallex Saudi Arabia, hold USD at Al Rajhi Bank or Riyadh Bank, and accept global card payments without depending on a ‘Western Only’ domiciled processor at all. That is a meaningful degree of independence from infrastructure that has historically been unavailable to Pakistani-linked businesses.

For all intents and purposes, Saudi Arabia is a more natural partner for Pakistani freelancers and IT companies to send payment links and to receive them as well because of how the financial relationship between Pakistan and the Kingdom is calibrated. The infographic below explains why Saudi Arabia has more of an edge:

Two ideas that could make the model stronger

While the infrastructure to use Saudi Arabia for this purpose exists, there are ways to make it stronger and more efficient. I want to flag two structural additions that, to my non expert eye, seem worth exploring seriously. People with more experience in these areas will know better than I do whether they hold up.

- Settlement via a Standby Letter of Credit

The obvious approach to moving money from the Saudi company to Pakistani freelancers is a SWIFT transfer per payment received. This works mechanically, but it generates a high volume of small cross border transactions, each carrying its own processing overhead, FX conversion cost, and correspondent bank fee. At scale, that overhead becomes significant.

A Standby Letter of Credit may be a more elegant settlement mechanism. Under this structure, the Saudi entity establishes an SBLC with a Pakistani bank, perhaps a facility sized at $5 million as a starting point. The Pakistani bank, backed by the SBLC as collateral, pre-credits freelancers' ESFCAs as payments accumulate on the Saudi side. Rather than hundreds of individual SWIFT transfers each day, the Saudi company makes periodic bulk settlements against the SBLC, weekly or fortnightly, and the Pakistani bank draws down the balance to reconcile.

This collapses the transaction overhead dramatically. It gives a Pakistani bank a meaningful and profitable role in the product. It converts a high frequency micro settlement problem into a clean treasury operation. The SBLC is a standard instrument that every Pakistani bank already understands, so the compliance path is well established rather than novel. Whether this structure survives contact with the actual regulatory and banking requirements on both sides is something I genuinely cannot say with certainty. But it seems worth a serious conversation with the relevant parties.

- The merchant of record problem through Visa and Mastercard's own frameworks

The concern I would raise about any structure where the Saudi entity is the sole merchant of record is this: Pakistani freelancers would have no direct relationship with the card networks. They would be invisible to Visa and Mastercard. If the Saudi entity ever ran into problems, the payment history of thousands of Pakistani freelancers would disappear with it.

This is a real concern. But it may have a direct answer from within the card networks' own rulebooks.

Both Visa and Mastercard have formal Payment Facilitator programmes. A Payment Facilitator underwrites merchants and signs acceptance agreements on their behalf, holds the acquiring relationship, and settles to what are called sub merchants. The important point is that sub merchants have formal registered status under the PayFac. They are not invisible. Stripe operates exactly this model.

Visa runs a CEMEA Payment Facilitator Certification Programme specifically designed for Middle East markets, with a tiered entry structure. New payment facilitators processing under $100,000 per month can enter through a Conditional Participation Agreement, which is a lighter, faster route to certification. A Saudi acquiring bank sponsors the PayFac. The Saudi entity registers as the certified PayFac under that sponsor. Pakistani freelancers register as sub merchants, visible in Visa's system, with formal agreements and their own transaction histories.

Mastercard has an equivalent structure. Sub merchants require direct registration with Mastercard once they exceed $1 million in annual volume, which gives the product a natural maturation path.

This is not a workaround. It is the mechanism that every major global payment platform uses to operate at scale. The card networks have already solved this problem. The question is whether someone is willing to go through the process of becoming a certified PayFac in the Saudi context, and use that relationship to formally bring Pakistani freelancers inside the tent.

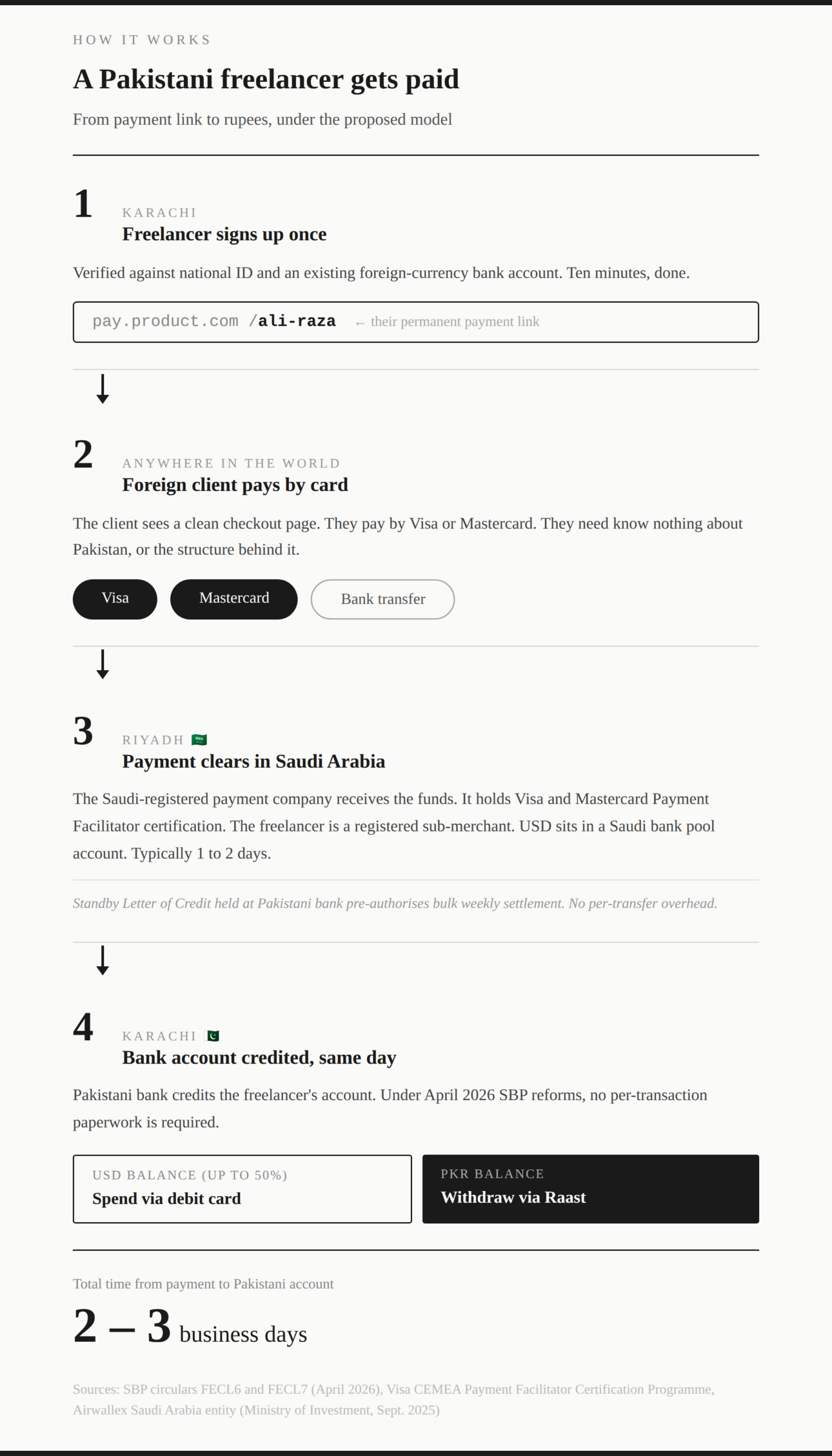

What the freelancer actually experiences

Sign up once. Verify identity using your CNIC and your ESFCA details. Ten minutes, done.

Get a payment link with your name on it. Send it to a client anywhere in the world. They pay by Visa or Mastercard. They see a clean checkout. They do not need to know or care about the structure behind it.

Within 48 hours the payment is in the Saudi company's USD account. The Pakistani bank, backed by the SBLC facility, credits your ESFCA. The USD balance sits there, spendable directly via your ESFCA debit card for software subscriptions, cloud infrastructure, or any other international business expense. The PKR portion converts automatically and arrives the same day via Raast.

For domestic clients, the same dashboard generates a PKR payment link over Raast. One product, one account, both markets covered. It is explained in detail in the infographic below:

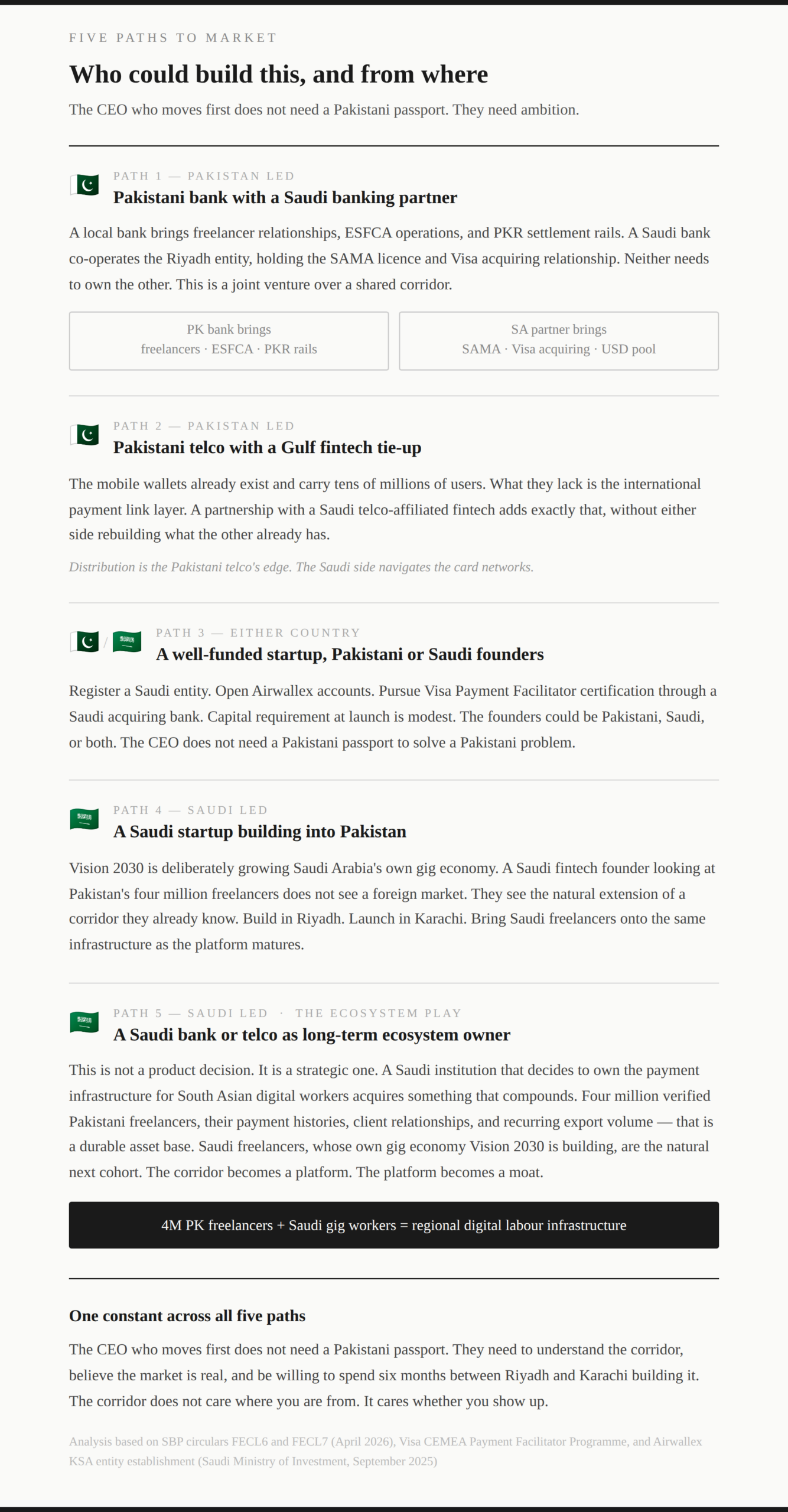

Who could build this?

There is no single right answer to this question, which is part of what makes it interesting. The opportunity is ripe for the taking. The structure supports several different entry points, and the ambition of the outcome does not depend on which one a builder chooses.

Take a look at the infographic below before reading the rest of the analysis:

A Pakistani bank with genuine digital ambitions can register a Saudi subsidiary or negotiate a joint venture with a Saudi banking partner. The Pakistani bank brings what it already has: millions of freelancers with ESFCA accounts, PKR settlement rails, and existing KYC infrastructure. The Saudi partner brings what the Pakistani bank cannot easily obtain from Karachi: a SAMA licence, a Visa acquiring relationship, and a USD pool account with a Saudi bank. Neither needs to own the other. The structure is a revenue sharing arrangement over a jointly operated corridor, not an acquisition.

A Pakistani bank with genuine digital ambitions can register a Saudi subsidiary or negotiate a joint venture with a Saudi banking partner. The Pakistani bank brings what it already has: millions of freelancers with ESFCA accounts, PKR settlement rails, and existing KYC infrastructure. The Saudi partner brings what the Pakistani bank cannot easily obtain from Karachi: a SAMA licence, a Visa acquiring relationship, and a USD pool account with a Saudi bank. Neither needs to own the other. The structure is a revenue sharing arrangement over a jointly operated corridor, not an acquisition.

A Pakistani telco has a different kind of edge. The mobile wallets already exist and carry tens of millions of users who trust them for everyday transactions. What those wallets have never had is an international payment link layer. A partnership with a Saudi telco affiliated fintech adds exactly that, without either side rebuilding what the other already has. Distribution is the Pakistani telco's asset. Regulatory access to Visa and Mastercard acquiring is the Saudi partner's. Put them together and the product exists.

A well funded startup, with founders from either country or both, is the lightest version of the structure. Register a Saudi entity, open Airwallex accounts, pursue Visa Payment Facilitator certification through a Saudi acquiring bank. The capital requirement at launch is modest relative to the market being addressed. What matters here is not the nationality of the founders but whether they are willing to spend the time in both cities that the structure requires.

Then there is the version that comes from the Saudi side entirely. Vision 2030 is deliberately growing Saudi Arabia's own gig and digital services economy. A Saudi fintech founder who looks at Pakistan's four million freelancers does not have to see a foreign market. They can see the natural extension of a corridor they already live in. Build the product in Riyadh, launch it in Karachi, and add Saudi freelancers onto the same infrastructure as the platform matures. The corridor already exists. The question is who claims it first.

The largest version of the idea is the one that a Saudi bank or telco with serious ambitions should be thinking about. An institution that decides to own the payment infrastructure for South Asian digital workers is not building a product feature. It is building a moat. Four million verified Pakistani freelancers, their payment histories, their international client relationships, and their recurring export volume are an asset base that compounds over time. Saudi freelancers, whose own gig economy Vision 2030 is actively trying to grow, are the natural next cohort on the same rails. The Pakistani corridor and the Saudi digital labour market are not two separate opportunities. They are one platform, seen from two ends of the same money pipe.

What is consistent across all five paths is this: the CEO who moves does not need a Pakistani passport. They need to understand the corridor, believe the market is real, and be willing to do the work in both cities. The corridor does not care where you are from. It cares whether you show up.

3 Comments

No comments yet. Be the first to join the discussion!