There is a new Chair of the US Federal Reserve in town. This is how it could affect Pakistan

As Warsh accelerates the shrinking of the Fed’s balance sheet, the danger to Pakistan is not lower US interest rates by themselves. It is the combination of a renewed oil and inflation impulse from war, a loss of confidence in the Fed's commitment to inflation target, and tighter dollar liquidity.

On the 13th of May 2026 the United States Senate confirmed Kevin Warsh as the seventeenth Chair of the Federal Reserve by a vote of 54 to 45. He took office on 15 May, when Jerome Powell’s term as Chair expired. In an arrangement not seen for roughly eighty years, Powell has chosen to remain on the Board of Governors rather than leave, keeping a seat and a vote on the policy committee.

But what appears to be a routine change of guard at the Fed might have wider implications this time around. This transition means an increased probability of a monetary policy error in the United States. Over the short and medium term that error will seep into Pakistan’s economy.

The how of this is quite clear. The danger to Pakistan is not lower United States interest rates by themselves. It is the combination of a renewed oil and inflation impulse from the conflict with Iran, a loss of confidence in the Federal Reserve’s commitment to its inflation target, and tighter global dollar liquidity as the new Chair accelerates the shrinking of the Fed’s balance sheet. If the front end of the policy rate is cut too early under political pressure while inflation is still being driven by supply, long-term United States yields can rise rather than fall. That outcome squeezes Pakistan’s import bill, reserves, fiscal space, and external refinancing at the same moment, and it does so while the International Monetary Fund programme leaves little room to absorb shocks. But what is behind the increase in this probability?

The Federal Reserve transition and the cost of a policy error

Kevin Warsh and Jerome Powell now occupy very different positions, and the difference matters for how policy will be set. Warsh is the Chair. He served as a Fed Governor from 2006 to 2011, sat alongside Chairman Bernanke through the 2008 crisis, and has spent the years since as a sharp critic of the institution he now leads, going so far as to call publicly for “regime change” at the central bank. His instincts are well documented: he is sceptical of a large Federal Reserve balance sheet, he believes the Fed should stop acting as a backstop for government borrowing, and he wants to speed up the runoff of the trillions of dollars in Treasuries and mortgage securities the Fed still holds.

Powell is no longer Chair, but he is not gone. His separate term as a Governor runs to 2028, and he has elected to keep that seat, an unusual step that has not occurred in roughly eighty years. In practice this creates a shadow Chair: a former leader who retains a vote and considerable institutional weight on the committee, and whose dissent or assent now carries unusual signalling power. The risk is not personal friction; it is policy incoherence and mixed signalling at a delicate moment.

To understand the shift at the Fed, it is important to recap the powers it actually has. For all intents and purposes most central banks and federal reserves all over the world have a couple of levers they can push and pull to exert their influence on the economy. These tools can broadly be put into two categories:

Price-based policy: This is the familiar tool: raising or lowering the federal funds rate. It works through demand. Higher rates make mortgages, car loans, and credit more expensive, so households and firms borrow and spend less.

Quantity-based policy: This works through the balance sheet. Instead of declaring that money is more expensive, the Fed makes money scarcer by removing cash from the banking system. With less liquidity to lend, banks compete less to push it out, and lending spreads and market rates drift up on their own.

In terms we can all understand, a price-based approach is like adding sugar to a cake and then hoping the person on a diet close to the cake will have the willpower not to eat it. A quantity-based approach simply takes the cake off the table.

This difference actually matters. Taking the cake off the table is the exact move Warsh wants to make. The intellectual case for it is that today’s inflation is largely supply driven, coming from an energy shock and geopolitical disruption rather than from excess demand. Interest rates act on demand, so they are a poor instrument for a supply problem. Worse, raising rates lifts the cost of capital for the very firms that would need to invest to relieve a shortage, which can prolong the inflation it is meant to cure. Several large drivers of the current US economy, healthcare spending tied to demographics and the investment supercycle in IT and AI, are also relatively insensitive to interest rates. Raising rates will not stop them and cutting rates will not speed them up. Warsh’s logical conclusion is that the balance sheet, not the policy rate, is the more appropriate tool for the present mix of forces.

Why the cost of an error is unusually high right now (and how Pakistan should read it)

The reason a mistake would be so costly is the inflation backdrop. After the US and Israel went to war with Iran in late February 2026, the conflict disrupted the Strait of Hormuz. Brent crude, which had been comfortable, surged. The effect on United States prices was immediate. Headline consumer price inflation, which had eased to about 2.4 percent before the war, rose to 3.8 percent in the year to April 2026, the fastest pace since May 2023, with energy up roughly 18 percent and gasoline up more than 28 percent. Core inflation, which strips out food and energy, also firmed to 2.8 percent, and the Fed’s preferred core measure was tracking toward its highest level in over two years. For the first time in three years, American wages stopped outpacing prices.

The point for policymakers is that the inflation impulse is real and could reignite on any setback. A supply shock of this kind is easy to mislabel as “transitory.” If it is treated as temporary and policy is loosened into it, and the shock then persists, the central bank can find itself behind the curve with its credibility already spent.

Here is the tension at the heart of the next six months. The President of the United States has made no secret that he expects the new Chair to lower interest rates, having criticised the previous chair repeatedly for keeping policy too tight. That is pressure toward price-based easing, cutting the funds rate, at the very moment the supply shock and sticky core inflation argue against it.

A critical mechanism for Pakistan to understand is the back end of the yield curve. Short-term rates are set by the Fed. Long-term yields, such as the ten-year Treasury, are set by the market and reflect expected inflation and the compensation investors demand for holding long debt. If the Fed cuts the short rate while investors doubt its resolve on inflation, long yields can rise even as short rates fall. The curve steepens for the wrong reason. The ten-year yield is already near 4.5 percent and touched a sixteen-month high around 4.7 percent in late May. Because the ten-year Treasury is the global benchmark against which emerging-market borrowing is priced, a rising back end raises the cost of capital everywhere, including for Pakistan, regardless of what the Fed does at the front end.

The market’s base case is that the new Chair holds rates steady, and a notable body of opinion argues that even today’s settings are not actually restrictive. The probability the market assigns to a rate increase by December has risen. The expert debate sorts into recognisable camps, ranging from those who see a deal with Iran clearing the way for cuts, to structuralists who argue the neutral rate is higher and that the Fed may need to hold or even hike to keep inflation expectations anchored.

Suppose the new Chair, under political pressure, signals or delivers at least one cut before year end while also advancing his preferred balance-sheet shrinkage. Markets are likely to read the front-end cut as inflationary, push the back end of the curve higher, and price in lost credibility. Some committee members would very probably dissent in earnest, and the public conversation would shift openly to the language of a “policy error.” The result is not the gentle easing of global financial conditions that an emerging market would welcome. It is a higher and more volatile long-end and tighter dollar liquidity as the balance sheet contracts. That specific combination is what carries the heaviest consequences for Pakistan.

What this means for Pakistan

Pakistan enters this period in a better but still fragile position. The economy is recovering under the 37-month Extended Fund Facility agreed with the IMF in September 2024 and the accompanying Resilience and Sustainability Facility. The third review was completed on 8 May 2026 and released about 1.3 billion dollars, bringing cumulative disbursements to roughly 4.8 billion. Gross reserves had risen to about 16 billion dollars at the end of December 2025, and the rupee has been broadly stable near 278 to 279 to the dollar. Growth is running near 3.6 percent and inflation near 7 percent. The Fund itself, however, has warned that the war in the Middle East clouds the near-term outlook, and it has raised its inflation forecast for the next fiscal year to 8.4 percent while trimming growth. Crucially, Pakistan sources roughly 90 percent of its energy imports from the Middle East region, which places the country directly in the path of the shock described above.

How will this shock reach Pakistan? It is worth being precise about the channel, because the obvious one is not the most important one here. The danger is not mainly Pakistan’s own oil-import bill. It is the second-round effect of this potential policy path. If the Fed cuts too soon, or if the market simply comes to fear a policy error, the working assumption becomes that inflation stays elevated for longer. That single expectation drives two things that matter for Pakistan, none of which depend on the price of oil.

Higher commodity prices broadly, not just energy. If markets price in persistent inflation and a Fed unwilling to lean against it, the response shows up across the commodity complex, in industrial metals, building materials, and food inputs, not only in oil. For an import-dependent economy, that raises the landed cost of the materials and inputs Pakistan must buy regardless of where commodities trade, feeding domestic inflation and squeezing the State Bank’s room to keep easing.

A higher back end of the curve. Most important of all, a loss of confidence in the Fed lifts long-term United States yields. Because the ten-year Treasury is the global benchmark against which emerging- market debt is priced, a higher back end raises the cost of capital everywhere, including for Pakistan, regardless of what the Fed does at the front end.

Can Pakistan do something to prepare?

The risks of the Fed transition are staring us in the face. But there are ways to mitigate these challenges. The first step would be to refinance at the front end, not the long end. The policy-error risk is a higher long end of the curve, so concentrate new borrowing and refinancing in short maturities. Borrowing short avoids locking in elevated long-term yields and keeps the debt stack cheap while the back end is at risk.

Secondly, if a long-dated dollar issue is unavoidable, execute it in the narrow window right after the war is resolved but before the dissent and inflation debate opens up among Fed members. That is when long yields are lowest: the oil relief is already priced in, while the credibility fight that lifts the back end has not yet started. Miss that window and the cost rises.

And finally, it is imperative to hedge the commodity prices that drive the import bill. Lock in forward or hedged pricing on key procured inputs (fuel, fertilizer, wheat, and similar) so a renewed spike in the broader commodity complex doesn't blow out import costs. Hedge while prices sit in the calm, not after the next move higher.

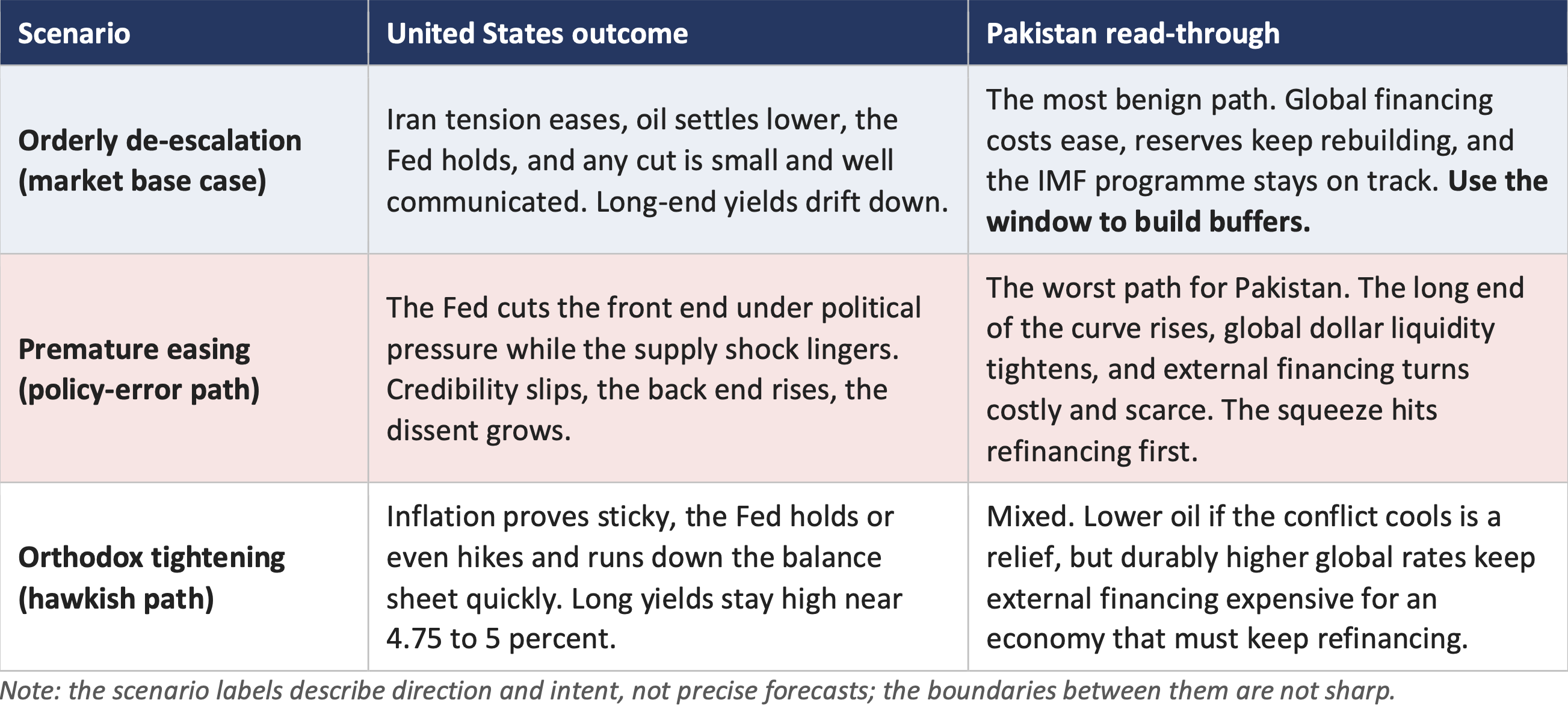

Of course, global realities change fast. Take a look at the scenarios and their read-through for Pakistan in the table below:

However the situation develops, what matters most is knowing this in advance, but also knowing what to watch. The shock to Pakistan would arrive through prices, the currency, and financing conditions weeks to months after the signals appear in Washington and in global markets. Watching the right indicators converts a surprise into a managed risk. The following are the most useful early-warning signals, in rough order of lead time:

Federal Reserve communication around the 16 to 17 June meeting and after: any shift toward cutting the funds rate while inflation is elevated. This is the trigger condition for the policy-error scenario.

The United States 10-year Treasury yield and the shape of the curve. A back end that rises while the Fed eases is the clearest market signal that Pakistan’s external financing is about to get more expensive.

Dissents at the Fed, A visible split, especially one involving the former Chair, would confirm the policy-error narrative is taking hold.

The state of the Iran ceasefire and the status of the Strait of Hormuz, given Pakistan’s direct energy exposure and its diplomatic role between the parties.

In sum, the change of Chair is not, by itself, the threat. The threat is a specific and plausible sequence in which political pressure, a live supply shock, and a credibility-sensitive market interact to raise the global cost of money rather than lower it, at least in the short term. Pakistan is exposed to that sequence chiefly through the cost and availability of external financing, through higher commodity prices, and through the imported inflation those prices carry, and it is exposed while its margin for error is thin. Recognising the sequence early, and acting in the calm rather than the storm, is the advantage this report is meant to provide.

The writer is chairman of the Punjab Board of Investment and Trade.

The writer is chairman of the Punjab Board of Investment and Trade

View all articles →Comments

No comments yet. Be the first to join the discussion!