Can electronic warehouses change how Pakistani farmers sell their crops?

The PMEX and the IFC have entered a partnership to strengthen agriculture commodities trading in Pakistan. The first step is formalising and digitising warehouses.

The Pakistan Mercantile Exchange (PMEX) and the International Finance Corporation (IFC) have agreed to work together on strengthening agricultural commodity futures markets and expanding the country’s electronic warehouse receipt system.

That sounds technical, but the basic idea is fairly simple. Pakistan’s agricultural supply chain is antiquated from seed to table. Every stage of the supply chain is painfully out of date, and while much is made of the deplorable state of seed research, farming techniques, and farm mechanisation in Pakistan, the post-harvest condition of agricultural products is as much of a problem.

Farmers rely on spot markets, selling their products to the closest warehouse or mill they can find before it starts to rot. The result is that the market gets overly saturated during harvest season and prices drop drastically. Only those with warehouses can afford to hold onto their crop until the prices improve. Even then, farmers often need immediate cash to get started on their next crop. As a result, farmers are easily exploited.

But this is not the only way to buy and sell crops in Pakistan. The Pakistan Mercantile Exchange (PMEX) offers the ability to trade in the agricultural commodity futures. A futures market deals with an agreed transaction at a later date. Suppose wheat is selling for Rs3,000 per 40kg today. A farmer fears the price may fall before he is ready to sell. A flour mill, meanwhile, fears that wheat may become more expensive. Through a futures contract, they can agree on a price for wheat to be bought or sold at a future date. The farmer uses the contract to protect himself against falling prices. The flour mill uses it to protect itself against rising costs. PMEX comes in by providing an electronic platform on which standardised contracts can be traded through brokers registered with the SECP. Structurally it is like the stock exchange, except for tangible commodities that exist in a warehouse somewhere and not shares in a listed company.

Even though this structure exists, the problem is scale. While PMEX recorded a massive overall trading volume of Rs 9.77 trillion, the vast majority of it consists of metals, energy, and financial contracts. Only a tiny fraction (less than 1%) of Pakistan's total agricultural crop volume is sold through PMEX. The main hurdle is that for agricultural commodities to be traded on a futures market, they need to be stored somewhere safe and reliable. There also needs to be some sort of digital or electronic proof that the crop exists.

This is where the IFC and electronic warehouse receipts come in. The IFC is a World Bank organisation which focuses exclusively on the private sector in emerging markets. An electronic warehouse receipt (EWR) is a financial instrument that is issued by an accredited warehouse to a farmer in exchange for his crops. Say a farmer goes to an accredited warehouse and hands them 100 tonnes of maize. The farmer will get an EWR that certifies the quantity and quality of agricultural produce deposited by farmers or traders. Using this EWR Since the warehouse is accredited buyers know they can trust the quality of not just the crop, but also how it is being stored. These EWRs then become the core component in trading agricultural commodities futures. Under the partnership agreement, the IFC will help strengthen existing regulatory frameworks and engage stakeholders to promote participation in commodity markets.

How this could work in Pakistan

To understand the potential of this agreement, it is important to understand how things work in Pakistan right now. We can illustrate this with the help of an example:

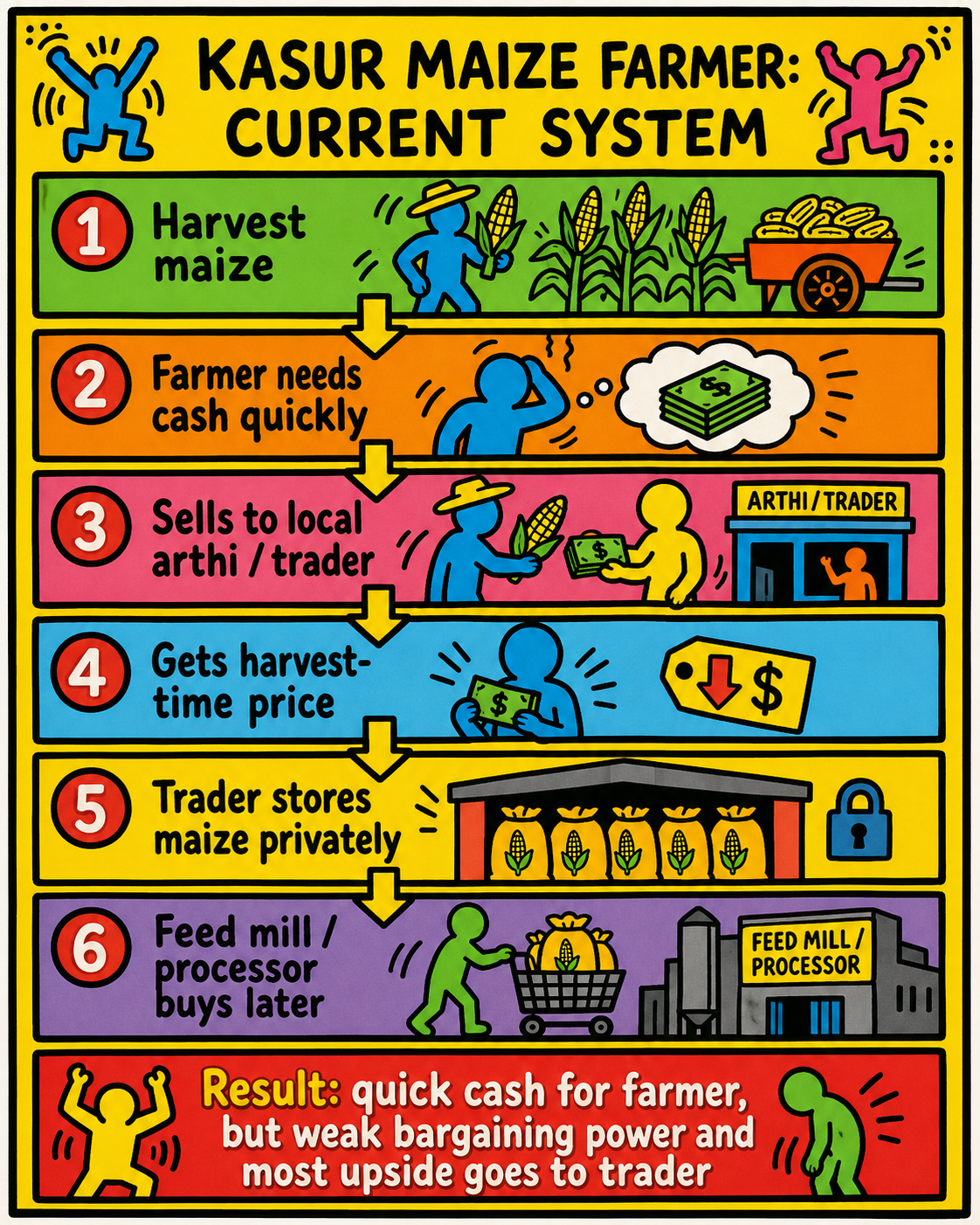

A farmer normally harvests a large quantity of crop at the same time as thousands of other farmers. This causes three connected problems. First, prices are often weakest during the harvest period because supply suddenly increases. Second, many farmers need cash immediately to repay input loans, meet household expenses or prepare for the next crop. They cannot afford to wait several months for prices to improve. Third, most farmers do not have proper storage. Keeping grain in an ordinary room or in gunny bags creates risks involving moisture, pests, contamination, theft and deterioration.

As a result, a farmer may be forced to sell immediately to a local trader or commission agent, even when the farmer believes the price is too low. These are the dreaded “arthis” that have long been a source of pain for farmers. The buyer has greater bargaining power because the buyer has cash, transport, storage and market connections.

Consider a maize farmer near Kasur. The farmer harvests 100 tonnes of maize. At harvest time, the local market is offering Rs2,400 per 40kg because large quantities of maize have arrived at once. The farmer believes the price could improve after three months, but needs money now for fertiliser, household expenses and the next crop. Under the traditional system the farmer may have little choice but to sell immediately for Rs2,400. The trader buys at the low harvest price, stores the maize and sells it later if the price rises. The trader receives most of the benefit from having storage and working capital.

But if the farmer had access to an accredited warehouse with the ability to issue an electronic warehouse receipt (EWR) the story would flip. The farmer delivers the maize to an accredited warehouse. After testing and grading it, the warehouse issues an electronic receipt for 100 tonnes of a specified grade

That receipt is effectively a verified digital ownership document stating that a specified quantity and quality of maize is stored at a particular accredited facility. The farmer can then take that receipt to a participating bank. Because the bank can verify that the maize exists and is being professionally stored, it may lend the farmer a portion of its value. The farmer now has cash without selling the crop immediately. Three months later, the farmer can sell the receipt when prices are more favourable. The buyer receives ownership of the stored maize through the electronic transfer. The farmer must still pay storage, testing, insurance, financing and transaction costs. Therefore, waiting only makes sense when the expected price improvement is greater than these costs.

Meanwhile, the commodities market is also bolstered by the presence of these accredited warehouses. Suppose PMEX shows a price of Rs2,650 per 40kg for maize to be delivered after three months. The farmer may decide to lock in that price rather than gamble on where the market will be after three months. A poultry-feed producer worried about rising maize prices could take the opposite position and lock in its purchase cost. The farmer gains certainty over revenue. The feed producer gains certainty over raw material costs. An investor or commodity trader may provide liquidity by accepting some of the market risk. The final result will not always be exactly Rs2,650 because of quality differences, location, transport costs, exchange charges and differences between futures and physical market prices. But the basic purpose is to reduce uncertainty.

PMEX’s EWR-based maize contract, for example, provides for physical delivery through the transfer of the electronic warehouse receipt from the seller to the buyer. This means the stored commodity does not have to be unloaded, moved and inspected again every time ownership changes.

The scalability problem

It is nice to imagine something working in Pakistan. If PMEX can be strengthened and farmers are allowed to sell their products through either accredited warehouses or even through futures contracts it would give them more tools to deal with the complicated timelines and realities of the agriculture sector. The problem, however, is scale. Remember what we said in the beginning? Less than 1% of Pakistan’s domestic crops are sold through PMEX.

Pakistan currently has just 37 accredited warehouses under the electronic warehouse receipt system, with a combined listed capacity of 461,550 tonnes. All of them are in Punjab, and their space is shared between wheat, maize, rice and paddy.

To understand how small that network is, compare it with Pakistan’s wheat crop alone. The country produced about 29.6 million tonnes of wheat in 2025-26. Even if every accredited warehouse were emptied and used exclusively for wheat, they could hold only around 1.6% of one year’s production. In practice, the proportion would be lower because those facilities also store other crops.

As things stand, this system can only serve selected agricultural districts and commercial participants, but not farmers across Pakistan.

Consider a small wheat farmer in interior Sindh. To obtain an electronic warehouse receipt, the farmer must first find an accredited warehouse, transport the wheat there, have it weighed and graded, and pay for handling, storage and insurance. With no accredited facilities currently listed in Sindh, the transport cost alone could make the exercise pointless.

Even in Punjab, distance matters. A trader moving several hundred tonnes can spread transport and handling costs across a large consignment. A farmer with five or ten tonnes cannot. If wheat prices are expected to rise by 6%, but storage, transport and bank financing cost 7%, waiting to sell leaves the farmer worse off.

Financing creates another obstacle. A warehouse receipt confirms that a crop exists and gives the bank collateral, but it does not guarantee a loan. Farmers may still need to provide identity documents, evidence of farming activity and a satisfactory credit record. Banks may also prefer larger borrowers because processing a small loan can involve almost as much work as approving a much larger facility.

What the agreement actually does

As far as the agreement between PMEX and IFC is concerned, it is not an immediate gamechanger but it is a start. We do not mean to deride what can only be seen as a positive move, but we simply wish to put it in context.

The agreement does not mean that a new national system will suddenly appear. Nor does it mean farmers will immediately start trading wheat contracts on their phones. What it does is bring PMEX and IFC together to review regulations, develop suitable futures contracts, involve banks, warehouses, traders and processors, and build awareness around a system that already exists in a limited form.

The people behind the agreement, at least, are very clear about what it can achieve. “A modern, efficient commodities market is essential for unlocking Pakistan’s agricultural potential. By strengthening price discovery, expanding private sector warehousing, and promoting electronic warehouse receipts, we can help farmers secure better returns, reduce losses, and access finance,” says Mr.Simon Andrews, IFC Director for Pakistan. “This is a critical step towards building a more resilient and market-driven agri-food sector”, he added.

“This partnership with IFC marks an important step towards modernizing Pakistan's agricultural markets. Efficient commodity futures markets and electronic warehouse receipts can improve price transparency, strengthen risk management, encourage investment in storage infrastructure, and provide farmers, traders, processors, and investors with better market access. Together, we aim to create a stronger and more resilient agricultural marketing ecosystem for Pakistan”, said Mr. Khurram Zafar, Chief Executive Officer of PMEX.

If it works, the system could give farmers more freedom over when they sell their crops, give banks greater confidence when lending against agricultural produce, provide processors with more predictable prices and create better information about how much grain is stored and where. The problem is that Pakistan is still a long way from making this accessible to most farmers.

For the system to reach ordinary farmers, it must be simpler than expecting each farmer to arrange transport, negotiate with a warehouse, deal with a bank and understand PMEX contracts independently. A scalable model would use village collection points, farmer groups, cooperatives or credible aggregators. Several farmers could combine their produce into a larger consignment. The aggregator could arrange transport, testing, storage and financing. Each farmer would receive a digital record showing his share of the stock and the money advanced against it. A big part of this would involve government support. The government, luckily, is on board.

“The government has launched the Agriculture Innovation and Growth Program (AIGP) for the capacity building of farmers. The federal government is also working on reforms to modernize the agriculture sector regulatory framework and is in the process of finalizing the national Wheat Policy, which will be a giant leap for the agriculture sector as a whole,” said Mr. Ahmed Umair, Coordinator to the Prime Minister on Agriculture and Food Security.

Banks would need to approve small loans quickly, ideally within a day or two. Farmers who wait a week for funds will continue selling to traders offering immediate cash. Warehouses would need to be located close to production centres. The government would also need predictable policies on wheat procurement, imports, exports and stock releases. Sudden policy changes can destroy the price assumptions on which futures markets depend.

Abdullah Niazi is senior editor at Profit. He can be reached at [email protected]

View all articles →2 Comments

No comments yet. Be the first to join the discussion!