As Afghanistan slashes coal prices again, can cement and power companies profit?

Royalties slashed by Rs 1,060 per ton, and customs duties slashed by Rs 4,400 per ton

In a move to stay competitive amidst the global downturn in coal prices, Afghanistan’s Ministry of Mines and Petroleum has announced a significant reduction in the royalties for coal. The royalties, previously set at 2,500 Afghani per ton, have been slashed to 2,200 Afghani. Furthermore, the customs duty has seen a substantial decrease from $45 to $30.

The decision by the Afghan government seems to be a clear attempt to maintain the allure of its coal exports in a challenging market environment.

“These changes equate to a decrease of Rs 1,060 per ton in royalties and a decrease of Rs 4,400 per ton in customs duties,” explains Waqas Ghani, the Deputy Head of Research at JS Global Capital.

“As a result of these changes the price of Afghan coal is expected to hover around Rs 38,000 per ton,” Ghani adds. “However, companies based in the southern regions of Pakistan may face slightly higher prices,” Ghani adds further

Prior to this, Afghan coal commanded a price of approximately Rs 43,000 per ton to Rs 45,000 per ton for firms situated in the northern regions of Pakistan. However, the cost escalated for those based in the southern areas, owing to the increased expenditure on transportation.

The question then is: will local cement manufacturers and power generation companies benefit from the Afghan government’s decision?

Not enough for the power sector to care

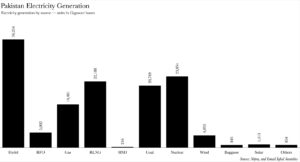

In the fiscal year of 2022-23, the power sector of Pakistan emerged as the primary consumer of coal, with a staggering consumption of 7.297 million metric tons during the July-March period, as reported in the Economic Survey of Pakistan 2022-23.

Coal contributed to a significant 16% of the total electricity generated in the fiscal year 2023-24, amounting to 129,591 gigawatt hours. However, the decision by the Afghan government may not have a substantial impact on the energy sector.

“Local power generation primarily relies on imported non-Afghan coal and Thar coal. Afghanistan, not being a significant global player, is unlikely to instigate price competition for market share,” elucidates A.A.H Soomro, an independent economic analyst. “The impact would be negligible, if at all,” Soomro further expounds.

“I don’t foresee a substantial benefit to the energy sector. Imported prices are currently low, and the energy sector is capable of procuring fuel,” explains Fahad Rauf, Head of Research Ismail Iqbal Securities. “The primary beneficiaries would be industries with captive generation,” Rauf asserts.

“Most of our coal plants are now considering incorporating some local coal into the mix, i.e., Thar coal. This would represent a significant development in terms of overall savings once implemented,” Rauf elaborates.

However, it is likely that the Afghan coal might not end up in thermal power plants to begin with.

“The National Electric Power Regulatory Authority (NEPRA) permits the purchase of Afghan coal only if the landed cost is lower than that of imported coal from other sources,” clarifies Dr Fiaz Chaudhry, Director of the LUMS Energy Institute and former Managing Director of the National Transmission & Despatch Company.

With a spot rate of 1$:Rs 297.13, Indonesian coal equates to a free-on-board price of Rs 21,467 per ton, rendering it significantly cheaper than the rates quoted for Afghan coal. Consequently, it’s a non-starter in terms of electricity generation.

Now, what about cement companies?

Bonanza for North based companies

“The move is positive for North based cement companies and will potentially translate to a reduction of Rs 5,500/ton (assuming an exchange rate of 1$:Rs 296),” adds Ghani. This paints a rosy picture for companies.

The term ‘Northern region companies’ is a reference to those enterprises nestled in the upper reaches of Pakistan’s cement sector. This sector, a mosaic of 16 companies, is neatly partitioned into two distinct regions: North and South. The North, a vibrant tapestry of Punjab, Khyber Pakhtunkhwa, and Azad Jammu and Kashmir, contrasts with the South’s expanse of Sindh and Balochistan.

However, this rosy scenario is marred by one glaring issue: these cement behemoths are already awash with more capital than they can effectively deploy, and their sales appear to be stagnating. This conundrum has been previously explored in depth by Profit for those interested.

Read more: Lucky Cement pays out dividend after hiatus of three years

Moreover, 2023 has seen these cement companies not only developing a penchant for doling out dividends but also displaying an insatiable appetite for share buy-backs. With demand languishing at a low ebb and predicted to remain so for some time, one can’t help but wonder if these cash-rich entities might consider slashing prices to stimulate sales."

Is a reduction in cement prices on the cards?

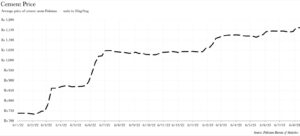

Cement prices have been on a relentless ascent for the past 18 months, soaring from a modest Rs 738 per bag in January of last year to a staggering Rs 1,161 per bag in the current month. This prompts an intriguing question: what could possibly instigate a precipitous decline in these prices?

“Cement companies in the northern zone are awash with a substantial inventory,” states Yousuf Farooq, Director of Research at Chase Securities. “Even the tax abatement by the Afghans might not immediately catalyse a significant surge in sales. If inventory continues to accumulate, it could potentially incite a decline in coal prices,” Farooq adds.

“Pakistan has been reliant on Afghanistan for its coal imports due to complications with accessing letters of credit, thereby curtailing supplies by sea. As the situation ameliorated, the demand for Afghan coal has ebbed, engendering a decrease in Afghan coal prices,” elucidates Farooq.

“Given that the Afghans are bereft of other substantial markets due to international trade settlement issues and exorbitant transportation costs to access the nearest seaports, they are likely to attempt to offload their production in Pakistan,” adds Farooq.

“This could exert additional downward pressure on prices,” Farooq asserts.

The author is a member of the staff, and covers the automobile, energy and advertising insdusties as a sector analyst. He can be reached at [email protected]

View all articles →197 Comments

No comments yet. Be the first to join the discussion!