March 23, 2026

How UBL (nearly) doubled in size in just one year

Pakistan’s third largest bank has become its second largest, and is rapidly chasing the number one title, under an ambitious new CEO. Here is how they have done this

March 23, 2026

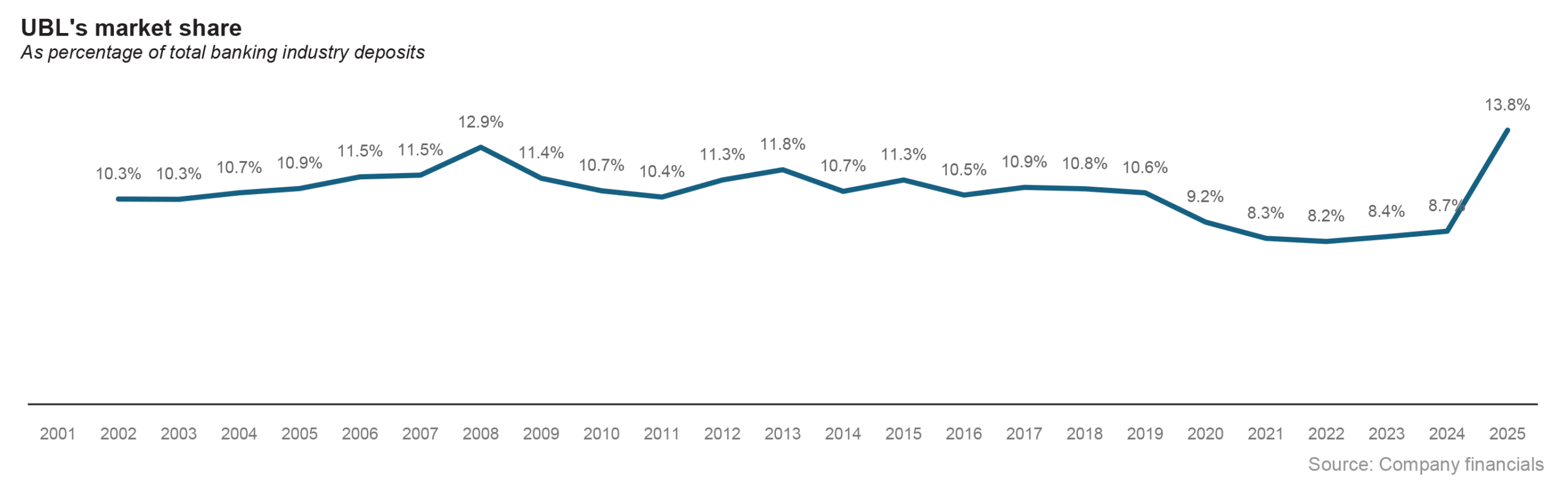

In 2025, United Bank Ltd increased its market share in terms of deposits by more than any bank in Pakistan over the past 25 years.

And just to be clear, we do not mean the total amount of the increase in deposits, which is a number that would axiomatically go up because of inflation each year. No, we mean in terms of percentage of total deposits that it gained in one year was greater than any one year increase we have been able to find in the past 25 years of Pakistani banking industry data.

Indeed, it is so much of an outlier that the single-year increase in market share that UBL achieved in 2025 is greater than any other three-consecutive-year cumulative market share increase by any Pakistani bank in the past 25 years.

Yes, you read that correctly: UBL did more in one year than any other bank has done over a three-year period in Pakistani banking sector history after the modern, competitive sector came into being in the early Musharraf era.

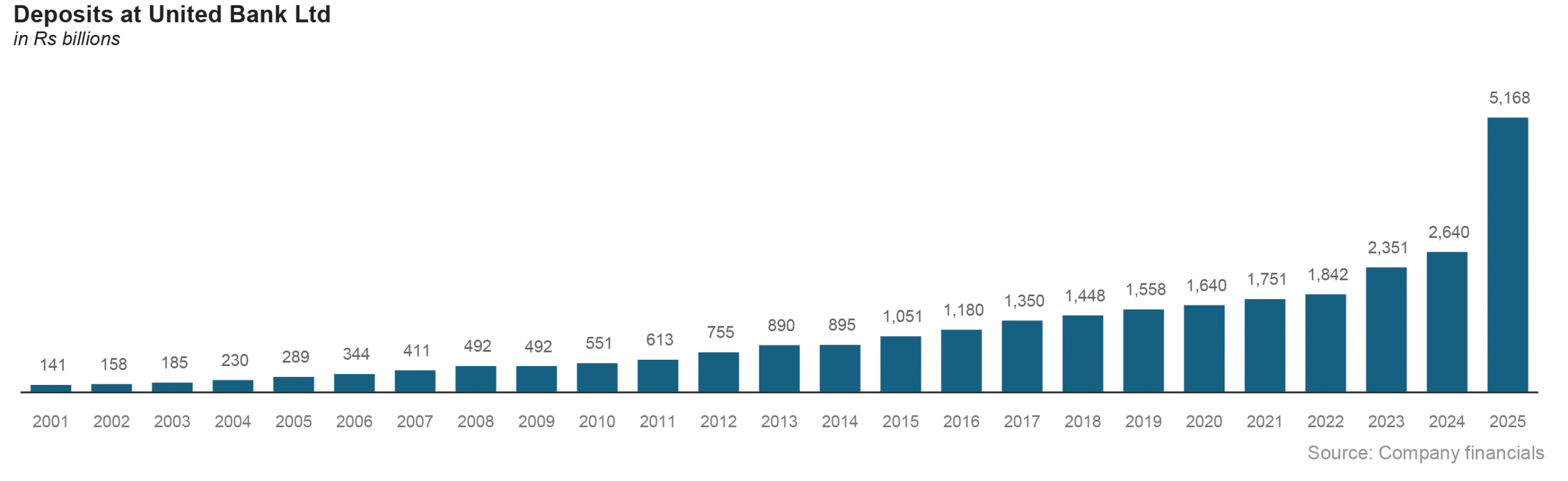

Here is what we are talking about: as of December 31, 2025, United Bank Ltd had Rs5.2 trillion in deposits, which is 13.8% of the banking industry’s total deposits. As the end of 2024, that number was Rs2.6 trillion, or 8.7% of the banking sector’s deposits. In absolute terms, this was a 95.7% increase in deposits (nearly doubling in just one year), and an increase of 509 basis points (bps) in its market share. One basis point is one-hundredth of one percent.

The previous record for the highest single-year growth in market share was in 2012 by Habib Bank Ltd (HBL), when it grew its share by 328 basis points, and overtook the National Bank of Pakistan to become the largest bank in Pakistan by deposits (functionally, the most important measure by which the size of Pakistani banks is determined).

This, ladies and gentlemen, was big. It would have been a major achievement for any bank to have accomplished in a single year, but the fact that UBL did it as the third largest bank in Pakistan, and as a bank that has been established for the past 66 years (it was founded in 1959) makes it more remarkable still. UBL started the year 2025 as the third largest bank in Pakistan and ended it as the second largest. It is now just 6.8% smaller than the still-largest HBL.

There is a very real possibility that, within calendar year 2026, UBL could overtake HBL as the largest bank in Pakistan. This is the story of how this bank, and its new, very ambitious, energetic CEO, made this happen.

The story of UBL

Ambition was perhaps baked into the bank’s inception. It was founded by Agha Hasan Abedi, the banker who is most famous for the downfall of the bank he founded later, the Bank of Credit and Commerce International (BCCI) on charges of money laundering and a slew of other financial crimes.

But before he did all of that, Abedi was the epitome of a young man with a chip on his shoulder and a lot to prove.

He was born in 1922 in Lucknow to a family that had, prior to the 1857 War of Independence, had been advisors to the Nawab of Awadh, arguably the nawabiest of nawabs. But by the time Abedi was born, the Nawab’s kingdom was gone, and all that were left were tall tales of the good old days from over a century ago, and the nawabi graces that came with those, but not the money to fund the sedentary lifestyle they were meant to accompany.

Abedi joined Habib Bank when he was 24 and the following year, when Partition happened, moved with the bank to Pakistan. For the next 12 years, he worked at Habib Bank, helping develop the new country’s banking system after virtually all of the old banks that held people’s money left because they were owned by people who either migrated to, or always lived on, the other side of the new border.

By 1959, he managed to develop enough contacts with the bank’s high net-worth clients, including the man who would later become the President of the United Arab Emirates – Zayed bin Sultan al-Nahyan – who helped finance the bank’s founding.

Agha Hasan Abedia, seen here meeting with President Jimmy Carter, leveraged contacts with high net-worth clients he met as a banker to start what was then known as the Bank of Credit and Commerce International (BCCI). He was later implicated in a host of financial crimes and money laundering cases.

It started its life as the fourth local bank (the Pakistani banking sector had many foreign bank branches back then) and rapidly began growing with the economy.

Then two disasters struck. First, the 1970 Bangladesh war of independence resulted in the bank losing all of its branches and deposits in what had previously been East Pakistan. And then, in 1974, the disaster that was Zulfikar Ali Bhutto struck Pakistan’s banking sector, and United Bank, along with all other locally owned banks, was nationalized.

The next 23 years of the bank’s history are a haze of nationalized, bureaucratic blur. Then, when Nawaz Sharif returned as Prime Minister, he restarted the privatization drive for the banks. In his first term from 1990 through 1993, he had privatized MCB Bank and Allied Bank. Now, he turned his attention to the bigger challenges at HBL and UBL. At HBL, he appointed Shaukat Tarin to lead the turnaround effort. At UBL, it was another ex-Citibanker, Zubyr Soomro.

Soomro led the bank from 1997 through 2000, a period of intense retrenchment of the excess employees who had been hired by successive governments for political reasons, the kind of futile and costly “jobs” program that socialists like to dream up. Death threats from the thuggish union leaders leveled towards the bank’s executives were common.

But after finally implementing a massive “golden handshake” program (read “bribes to unions to make them go away without violence”) and restructuring the holes on the bank’s balance sheet, it was ready to be privatized.

Zubyr Soomro was appointed to lead the cleanup at UBL in 1997 so it could be privatised, a feat that was eventually achieved in 2002. He returned to Citibank after this stint at UBL.

In 2002, a consortium of the Abu Dhabi Group (led by a different member of the Nahyan family) and British Pakistani billionaire Sir Anwar Pervez’s Bestway Group won the bid for a 51% stake and management control in the bank. At the time, UBL was still the fourth largest bank in the country, a position that it had occupied virtually uninterrupted since the early 1970s.

The post-privatization evolution

The bank we know today as UBL is a product of what transpired next: a bank that sought to go back to its ambitious roots as a meaningful disruptor in Pakistani financial services.

In 2005, it was publicly listed on the Karachi Stock Exchange, and in 2007, it became the second Pakistani company to launch a Global Depositor Receipt listing on the London Stock Exchange, raising $650 million from foreign investors in the process. Back then, London was still a prestigious global financial center. It was in the latter half of the Musharraf era that UBL firmly overtook MCB Bank as the third largest bank in Pakistan, a status it occupied from 2005 through 2024.

Also in 2005, it opened up the first retail branch of an asset management company in Pakistan. In 2007, it launched its own property and casualty insurance company called UBL Insurers. In 2010, it launched a branchless banking division called UBL Omni. And during this whole time, it also kept expanding its physical branch network throughout Pakistan as more and more cities became part of larger metropolitan regions and started needing connectivity to more formal financial services.

The driving force behind much of this were the bank’s longtime CEO Atif R. Bokhari, who held the position from 2004 through 2014.

The board support for that innovation and ambition came from the Bestway shareholders, with the Abu Dhabi Group mostly focusing on their other bank in Pakistan, Bank Alfalah. The conflict of interest between being a major shareholder in two prominent banks eventually became unwieldy enough that, in two transactions between 2011 and 2013, the Bestway Group bought out the Abu Dhabi Group’s entire shareholding in UBL. And in 2014, the government of Pakistan sold off its remaining 19.8% share in the bank for $387 million.

The men (and woman) who led the bank

Between 1997 and 2023, all of the five people who held the title of CEO of UBL had either a foreign education, or significant foreign work experience, and frequently both. The current CEO, Muhammad Jawaid Iqbal, appointed in 2023, has neither. (His Harvard Business School certificate is not a degree and the kind of thing one emphasizes in one’s profile after a lifetime of having been made to feel inferior by the Anglophone Pakistanis who have historically dominated the senior echelons of the non-public part of the Pakistani banking sector.)

Zubyr Soomro, the CEO who led the restructuring prior to the privatization process, is the epitome of his generation of Anglophone Pakistanis: educated at Karachi Grammar School from where he graduated in 1966, then the London School of Economics for an undergraduate degree in Economics in 1970, followed by a long stint at Citibank, in London, the Middle East, and Pakistan, culminating in the Citibank Pakistan country head position from which he retired shortly before the 2008 financial crisis. Soomro’s stint as CEO of UBL from 1997 through 2000 was effectively a sabbatical from his Citibank tenure.

Then came Amar Zafar Khan, who trained in the early 1970s as a chartered accountant in the UK at a small firm called Bennet Nash Woolf & Company, before joining Pricewaterhouse in 1978. Shortly thereafter, in 1981, he joined Citibank, serving in Saudi Arabia, Nigeria, and the UK for the next 11 years. He then set up a securities brokerage firm in Nigeria on behalf of the World Bank’s International Finance Corporation in 1992, before returning to Pakistan in 1996 and shortly afterwards, joining Zubyr Soomro’s team to help prepare UBL for privatization.

When Soomro went back to Citibank, Amar Khan took over as CEO at UBL, where he served until 2004 and was CEO at the time Bestway and the Abu Dhabi Group took management control. He stayed on for two years after their takeover, following which he retired.

The next CEO was Atif R Bokhari, the first CEO who was appointed by the new shareholders, and one who went on to serve as the bank’s head for the next 10 years, giving the bank much of its current shape. Bokhari, unlike his two predecessors, was not a Citibank alumnus. Educated at the University of Central Missouri from which he graduated with an MBA in 1983, Bokhari spent the formative part of his career at the Bank of America from 1985 through 2000, mainly in their Pakistan branches before the bank exited the Pakistani market entirely.

He had joined the pre-privatization HBL before he was tapped in 2004 to lead UBL. His strategy was simple: Pakistan’s financial services sector was expanding, and UBL should tap into all of it. He added 300 more branches to the already 1,000+ branch network for the bank. He significantly bolstered the investment into the asset management subsidiary, and started the insurance subsidiary. He pushed for the creation of the Islamic banking operations, and the branchless banking operations.

But the growth that Bokhari saw in the bank came at a pace that was set in large part by the growth in the banking sector as a whole. The single fact that attests to this is that when he took over in 2004, UBL’s share of total banking sector deposits was 10.7% of the industry and when he left in 2014, despite having fluctuated up and down in the intervening years, it was at 10.7% of banking deposits. Almost exactly unchanged.

Next came Wajahat Husain, the IBA alumnus from the class of 1982 who had spent the bulk of his career at banks in the United Arab Emirates and had initially joined UBL in its UAE operations in 2005. He took over as CEO in 2014, lasted three years, and left in 2017 with no major developments taking place during his tenure.

Then the UBL board did something unprecedent in the country and decided to appoint the first woman to head a major Pakistani bank: Sima Kamil.

Also a Karachi Grammar School alumna (graduating in 1976), Kamil had an undergraduate degree from Kingston University in London and an MBA from the City University of London. She began her Pakistani banking career in 1986 at American Express Bank before moving to ANZ Grindlays in 1988, where she then stayed for 11 years, mainly in Pakistan but also briefly working in Melbourne for two years during that time. As part of ANZ’s sale to Standard Chartered, she joined SCB’s operations in Pakistan in 2000 before moving to HBL in 2001.

At HBL, she held several positions, heading up wealth management, the asset management subsidiary, and the branch banking network. She was the person leading HBL’s branch banking network from 2011 through 2016, a period during which it became the largest in the country. In 2017, she was appointed the new CEO of UBL.

Sima Kamil was the first woman to become the head of a major Pakistani bank.

In an earlier era, Kamil’s credentials might have been overlooked, but this was the peak of the MeToo era, and boards were looking to promote more women. Kamil’s impeccable credentials made this an easy choice: on her own merits, a qualified candidate, and the fact that she was a woman was an added bonus.

Her tenure was also largely uneventful, and in 2020, she left the bank to join the State Bank of Pakistan as a deputy governor.

Next came Shazad Dada, yet another alumnus of Karachi Grammar School. Dada was a graduate of the elite Wharton School at the University of Pennsylvania, from where he did both a bachelors degree in 1990 and an MBA in 1996. He worked for 20 years at Deutsche Bank, in New York and London, before moving back to Pakistan in 2010 to lead Barclays’ mistimed entry into the Pakistani banking market. He worked there for four years, following which he left to lead Standard Chartered Bank Pakistan in 2014, a position he stayed at for nearly 6 years. His very first position at a Pakistani entity was as CEO of UBL.

Dada’s tenure at UBL appears to have prematurely been cut short, since his 3-year contract was not renewed and it was unclear as to why he left.

Jawaid Iqbal and his approach

The new CEO, appointed after Dada left, is different from all of the others. In a pedigree obsessed industry, he is an alumnus of Bahauddin Zakaria University, who worked all his life in Pakistan at banks like Emirates Bank International, National Bank of Pakistan, and Allied Bank. At the time that he was tapped to lead the bank, he was running a personal investing company called Providus Capital.

But this CEO is also known for injecting a degree of ambition into what is normally thought of as the most sluggish portion of an already sclerotic industry. Pakistani banks do not innovate, and hardly even lend to entities that are not the government of Pakistan. And into this foray has jumped in Muhammad Jawaid Iqbal – possessing possibly the most common of Pakistani male names – and delivered what appears to be uncommonly energetic results.

The increase in deposits has come not from a single trick, but appears to be an across-the-board expansion that the bank has been able to achieve in its balance sheet.

For the financial year ending December 31, 2025, the bank saw its deposits from individuals increase by 42%, and corporate clients increase by 127% compared to the previous year. Taken together, these two categories of depositors – the most diversified kind that a bank can have – account for over 58% of the increase in deposits that took place at UBL.

Yes, the banks’ deposits from government entities and non-banking financial institutions (NBFIs) rose by abnormally large amounts – 344% and 403% respectively – but those two categories only account for less than 35% of the increase in deposits: substantial, to be sure, but this does not appear to be a case of winning a handful of relationships to pump up the numbers, at least from the data available.

Nor is this a case of attracting deposits by offering abnormally high interest rates, at least not in quantities to become a meaningful problem for the bank. Current accounts and savings accounts fell from about 91.5% of total deposits to 84.3% of total deposits, a noticeable drop, but hardly a catastrophic one. More importantly, clearly not even a plurality of the increase in deposits that the bank was able to achieve in 2025.

The broader story is both more mundane and more impressive: that UBL was able to grow its deposit base – and double from an already very high base – by pulling on all levers available to management in order to grow its deposits.

They grew relationships with individuals, and businesses, with the government, and with financial institutions. It is a broad growth story, which suggests that the key ingredient in growth, more than anything else, is likely just the ambition to wanting to grow as fast as possible despite being a large bank with a comfortably steady stream of profits from its existing business lines.

Jawaid Iqbal was appointed President and CEO of UBL in April 2023. His predecessor, Shahzad Dada, served a single three-year term as the head of the bank which was not renewed "for personal reasons."

One possible area to look at deeper is the foreign deposits, which more than doubled from Rs594 billion at the end of 2024 to Rs1,237 billion at the end of 2025. But even here, the overwhelming majority of the increase came from current accounts by individuals, and given the fact that individual foreign currency accounts increased by about $1.9 billion, it is highly unlikely that this increase came from a highly concentrated set of depositors. And given the fact that these are current accounts, it also means that the bank is not taking on an abnormally large interest rate liability either.

In short, Jawaid Iqbal, the man unlike any of his predecessors at UBL, appears to be leading the bank in a manner unlike any of his predecessors. Part of that might be explained by the fact that he owns more of the bank than they did: Iqbal personally, and entities controlled by Iqbal collectively, own about 4% of the bank, based on estimates made by Profit from the disclosures made by UBL.

In other words, the most important thing that distinguishes Iqbal from his predecessors is not his credentials, but the fact that he is more of an owner-operator than anyone else previously in his position, except perhaps Abedi himself. Let us hope Iqbal’s career ends on a happier note than Abedi’s.

Managing Editor, Profit Magazine. He can be reached at [email protected]

View all articles →24 Comments

No comments yet. Be the first to join the discussion!