March 26, 2026

How far can increased financing to build homes go in Pakistan?

The government's “Mera Ghar, Mera Ashiana” scheme now offers financing up to Rs 1 crore with a subsidised markup rate for the first 10 years of the loan. However, structural problems continue to plague Pakistan’s housing market.

March 26, 2026

A house of one’s own remains a luxury in Pakistan. According to some estimates, the housing shortfall stands at around 10 million units, with around 350,000 additional units being added each year. Given that housing remains a cornerstone of Pakistan’s economy, closely tied to indicators such as inflation, this is a big problem. This is more so for a population that stands at over 24 crores.

The government recently announced a scheme to facilitate prospective homeowners in making a home for themselves. This financing scheme, called ‘Mera Ghar; Mera Ashiana’ was introduced in September 2025, where it stipulated loans at fixed markup rates for those looking to buy or construct their first houses. It was a tiered system with rates of interest depending on the size of the loan. The financing was limited to a maximum of Rs 35 lacs.

Less than six months later, the government has expanded the scope of the scheme, enlarging the available financing to Rs 1 crore as well as a uniform mark-up rate for loan amounts across the board, removing the tiered system. The loans, in continuation of the original scheme, would be available for a period of up to 20 years, of which for the first 10 years the markup rates would be subsidized by the government.

For a country with rising inflation levels and very high poverty rates, such measures are more than simply welcome; they are necessary. The availability of a house to sleep in and protect oneself against the elements remains not only a core economic prerogative, but is also one of our most human requirements. Such schemes would therefore aid the expansion of the opportunity to own a house to more people than would have been able to afford it otherwise.

Yet such schemes might not be sufficient on their own to really make a substantial difference. Pakistan’s housing market suffers from certain limitations which schemes like the ‘Mera Ghar; Mera Ashiana’ might not be able to undo the effect of on their own. The situation of Pakistan’s housing market and the role of formal financing in it has been limited by a number of issues including recovery for banks and access for potential clients.

As Zafar Masood, Chairman of the Pakistan Banks Association, pointed out in a recent article, not only is the vast majority of housing financing done through informal channels, institutional and social attitudes towards enforcements also hinder the growth and widespread acceptance of such financing mechanisms. Similarly, the absence of ‘patient capital’ exposes people who have taken out loans to great volatility in interest rates, eroding their ability to sustain their everydays. Unless measures are taken to increase the penetration of formal financing, such schemes on their own might not live up to their promise.

The Scheme and the Update

In September 2025, the federal government announced the commencement of the ‘Mera Ghar; Mera Ashiana’ scheme. It was instituted as a measure to promote affordable housing by providing subsidized mark-up rates.

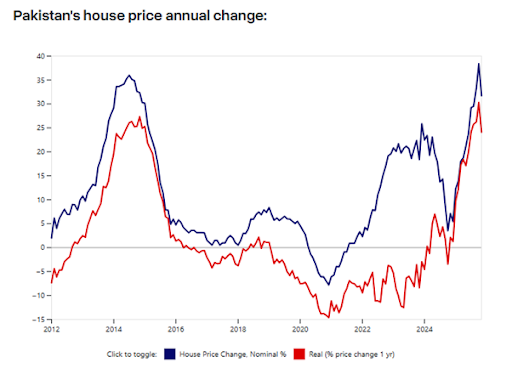

This was done in light of rising property prices in Pakistan, which since the Covid had rushed to mountainish heights. While the real value of housing prices had fallen to -14 percent in December 2020, these rose sharply afterwards, reaching a peak of 30 percent increase by October 2025. With largely stagnant per capita incomes, economic uncertainty, and the consequent slowdown in economic activity in the middle, avenues for purchasing houses kept slipping out of the reach of the many.

Source: Global Property Guide

It was in this context that the ‘Mera Ghar; Mera Ashiana’ scheme was announced. Only people who were first time owners or had no housing unit (house, flat, apartments etc.) in their name were eligible to apply. The scheme covered financing for three main types of house-making: purchasing a housing unit, constructing new units on already owned land, and purchasing and constructing on a piece of land.

There were some restrictions on the available financing, however. The size of the eligible housing unit was restricted to 5 marlas for houses and up to 1360 sq ft for flats and apartments. The loan size was divided into two tiers. Tier 1 included loans up to PKR 20 lakh, while Tier 2 included loans that were between 20 and 35 lakh. 35 lakh was the maximum limit one could borrow under this scheme.

The markup rates were different for both the tiers. For Tier 1 loans, the rate was fixed at 5 percent, while for Tier 2, this rate was at a fixed 8 percent. These rates were for the first 10 years due to a government subsidy for that duration. After 10 years, the mark-up rates would be determined by the bank under the formula of KIBOR rate + 3 percent. The maximum tenor of the loan could be 20 years under this scheme.

This was before. Now, the government has modified this scheme. The key changes pertain to most of the above-mentioned clauses. The maximum size of the housing unit has been increased to 10 marlas for houses, and 1500 sq ft for flats and apartments. The maximum amount that can be loaned under the scheme has also been increased to PKR 1 crore. The tiered system has been abolished, and there is now a flat 5 percent markup rate for the first 10 years under the government subsidy. The rate after 10 years remains the same as before, i.e. KIBOR + 3 percent. Similarly, the maximum tenor of the loan also remains the same. The other conditions stay the same, as well.

How Hopeful Can One Be?

It doesn’t seem a stretch to deduce that this new change would make things easier for many. They can now finance bigger houses, can take out bigger loans to finance them, and the markup rate would be the same as if they had taken smaller loans, so no added ‘cost’ for them. But certain questions rise and complicate one’s hopes.

Leaving aside the fact that availing these loans requires belief in the long-term ability to pay these loans, which itself is contingent on hope for one’s own future, for which admittedly there is little room to be positive about, such a scheme as this will still have to contend with the dynamics of the local housing market. As Zafar Masud points out, much of the local housing finance is conducted through informal channels. People save up, sell their jewelry or borrow money from their families. This list is non-exhaustive, of course.

Using personal savings (or informal sources of finance) accounts for anywhere between 50 and 70 percent of the housing financing available in the country. Developer financing, whereby housing developers are provided with institutional financing in an attempt to encourage them to provide more affordable housing, accounts for 20 to 40 percent of the total financing available for housing. Formal financing, through banking channels, for instance, covers a meagre range of 5 to 20 percent. In an economy which is 43 percent informal, the housing financing is almost 80 percent informal. Compared to India where the formal housing finance penetration is between 10 and 12 percent of the GDP, in Pakistan, this figure is as low as between 3 to 5 percent.

Even if avenues for more financing are opened – such as the ‘Mera Ghar; Mera Ashiana’ scheme – it would require a great shift for consumers to build trust in such systems. This is especially the case since a great reason for the informal nature of much of our economy is the people’s general distrust and fear of being involved with the tortuous official and bureaucratic systems, with their labyrinthine requirements and stipulations, often much more complicated than could be reliably internalized by an average person. Similarly, the lukewarm social attitudes towards loan repossession also mean that such loan schemes might not turn out the way they are supposed to. The courts grant stay orders upon non-payment of loans (or parts of loans), and in cases where loan amounts are smaller, the recovery costs remain disproportionately high.

At the same time, the market suffers from a lack of long-term fixed-cost ‘patient capital’, which would have allowed the borrowers to maintain enough cash flows to deal with changing interest rates. Such capital for long duration funding is usually done through pension funds and life insurance companies. In Pakistan, much of this capital, however, is invested in government securities, meaning less is available for loans to the private sector. Compared to the regional economies such as Bangladesh and India where the pool of long-term investable capital stands at respectively 13 and 25 percent of the GDP, in Pakistan, yet again, this figure is much lower: 3 to 4 percent of the GDP.

Such structural and economic hurdles cannot simply be overcome by a housing financing scheme such as the ‘Mera Ghar; Mera Ashiana’. The problems are compounded by the lack of transparent data, especially for land records, which expose the buyers to unnecessary yet cumbersome legal disputes. Unless such schemes are buttressed by broader reforms to encourage formal financing and to increase the pool of long-term investable capital, such schemes on their own might not be able to achieve what they intend to do.

6 Comments

No comments yet. Be the first to join the discussion!