April 17, 2026

UBL officially becomes Pakistan’s largest bank by deposits

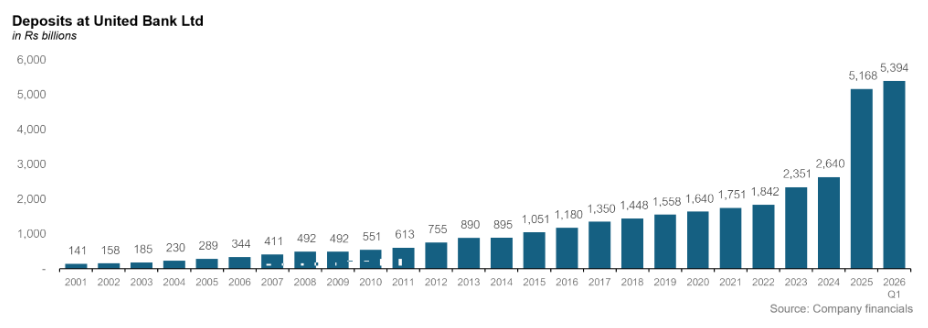

Since 2012, the title of Pakistan’s biggest bank seemed set in stone—until a record-breaking 15 months finally changed the leaderboard.

April 17, 2026

The long-standing hierarchy of Pakistan’s banking sector has been upended. Following Habib Bank Limited’s (HBL) release of its first-quarter results today (Friday), and coming just 48 hours after United Bank Limited (UBL) posted a historic performance for the first quarter of this financial year, the data confirms a significant shift: UBL is now officially Pakistan's largest bank by deposits, the industry's primary benchmark for size.

A tale of two quarters

The two giants showed quite a variance in their first-quarter results. HBL’s consolidated pre-tax profit for Q1 2026 stood at an impressive Rs 33.7 billion, but it paled in comparison to UBL’s performance, which set a new industry record by posting a standalone pre-tax profit of Rs 102 billion for the same period—a first for any bank in Pakistan. The shift in the "largest bank" title, however, was settled in the deposit column. HBL’s unconsolidated deposits declined during the quarter, falling to Rs 5.07 trillion. Meanwhile, UBL’s deposit base continued its aggressive climb, reaching Rs 5.39 trillion and officially overtaking its rival.

For context UBL had started the year 2025 as the third largest bank in Pakistan and in just fifteen months it has now become the largest after having more than doubled its deposits during this short period of time. The last time a bank achieved a similar growth spurt was way back in 2012 when HBL overtook the National Bank of Pakistan to become the largest bank in Pakistan by deposits.

Ranking by asset size and equity

Notwithstanding the latest deposit lead, UBL had taken over the title of Pakistan’s largest bank measured by total asset size some time ago. But despite UBL’s larger asset book, the title of the largest bank remained with HBL, as UBL’s massive assets of Rs 12.7 trillion compared to HBL’s 7.7 trillion is a somewhat deceptive measure to size up a bank. This is because a significant portion of UBL’s assets are driven by massive Open Market Operation (OMO) borrowings, which currently stand at Rs 6.6 trillion. Essentially, the bank is borrowing trillions from the SBP to finance heavy investments in government T-bills.

While HBL still holds the lead in terms of shareholders' equity (book value) at Rs 454.3 billion compared to UBL's Rs 416.2 billion, investors have signaled a clear preference for UBL’s growth trajectory. With a market valuation exceeding Rs 1 trillion, UBL is now the largest bank in Pakistan by market cap and the second-largest listed entity on the entire Pakistan Stock Exchange (PSX), trailing only OGDC.

| Top 5 Pakistani banks by market capitalisation | ||

| Bank | Market Cap | Status |

| UBL | Rs 1.0T | #1 Bank / #2 PSX Overall |

| Meezan Bank | Rs 891B | Strong #2 |

| MCB | Rs 493B | #3 |

| HBL | Rs 458B | #4 |

| NBP | Rs 449B | #5 (Ex-Dividend) |

How did UBL do it?

The accounts for the latest quarter are not detailed and only give the broad numbers. A look at UBL’s annual accounts ending December 2025 can give us an idea of how the bank managed this surge over the past year and a half.

The bank saw its deposits from individuals increase by 42%, while deposits from corporate clients increased by 127% compared to the previous year. Taken together, these two categories of depositors—the most diversified kind a bank can have—account for over 58% of the increase in deposits that took place at UBL. Yes, the bank’s deposits from government entities and non-banking financial institutions (NBFIs) rose by abnormally large amounts—344% and 403% respectively—but those two categories account for less than 35% of the increase in deposits. This is substantial, to be sure, but it does not appear to be a case of winning only a handful of relationships to pump up the numbers, at least from the data available.

Neither does this appear to be a case of attracting deposits by offering abnormally high interest rates, at least not in quantities that would become a meaningful problem for the bank. The Current Account to Savings Account ratio (CASA) fell from about 91.5% of total deposits to 84.3%, a noticeable drop, but hardly a catastrophic one. They grew relationships with individuals and businesses, with the government, and with financial institutions.

To put it simply there was no single path to getting here for UBL. The ambition to grow fast was complimented by an aggressive management strategy that prioritised gaining new business. The story is more about a diversified approach with the ambition to grow as fast as possible despite already being a large bank with a comfortably steady stream of profits from its existing business lines. But that does raise the question: if a bank isn't competing on better rates, then what exactly is it doing to grow its share of current accounts, which pay zero interest?

A big part of the growth story is how the bank is being run. Senior-level staff at UBL confirmed to Profit that, unlike other banks where each department works in silos and has its own targets to achieve, UBL runs like a one-man show. The bank’s President, Jawaid Iqbal, drives the strategy and everyone else is then given the autonomy to make decisions to have that strategy implemented. The instructions from the top are to get as many current accounts as possible and offer other freebies and incentives to achieve that single-focused goal, as long as the overall deal makes a profit for UBL.

To give an example, one employee reiterated how they secured a billion-rupee-plus current account from a big supermarket chain in Punjab. The person dealing with the CFO of the supermarket offered a 0% MDR on the card machines, meaning UBL was making a loss on the cards business and paying issuer fees from its own pocket. But in return, it was promised that the primary working capital bank accounts (current)—where all collections from supermarket sales are deposited and from which suppliers are paid—would be given to UBL. "We make a Customer Profitability Report (CPR) when we are approaching a big corporate customer for their current account business. We make projections on the average balance of the current account and the interest rate savings, and deduct from it the cost of the perks and privileges that are given to the customer in return. As long as the net number is positive, we go ahead with the deal. At other banks, there are lengthy approvals because other departments, like the cards team, would not want to compromise on their profitability numbers just to get current accounts. At UBL, we just see if this is overall good for UBL, then we do it as we have the full support from the top."

The strategy to get cheap deposits doesn't stop here; Jawaid Iqbal is also very aggressive in terms of his HR policies. He hires people and gives them targets; if these are achieved, staff receive bonuses and extraordinary promotions. Another UBL staff member confided that unlike other banks where it takes years to get promoted from one grade to the other, at UBL they now get double and even triple promotions. Another bank President said that UBL is now known in the industry as a bank with a culture of incentives and accountability. If you perform well you are rewarded, but if you slack you can't stay unnoticed and survive for long. Other than promotions, staff responsible for deposit growth are given cars as incentives. A regional head recently got a Land Cruiser LC300 worth approx Rs 80- 90 million as his official car (the same car that the President is entitled to) as a reward for achieving a current account portfolio of Rs 300 billion. "This is the official policy now: if you can grow your current account portfolio to Rs 300 billion, you get an LC 300 from the bank." A certain executive in the UAE branch was even given a Porsche by the bank for securing a large account.

Identity problems

A commercial bank’s primary job is to take deposits and lend them to the private sector (Advances). And while there seems to be no doubt that UBL has mastered the deposit and investment sides of the balance sheet, its core advances (lending) have not kept pace with its growth and have actually seen a decline to Rs 1.48 trillion. When combined with the fact that Rs 30.5 billion of its quarterly income came from gains on the sale of securities, critics raise a fundamental question: Is UBL still operating as a traditional commercial bank, or has it transitioned into a government-backed investment house?

Can we expect a cola-like war?

Despite the milestones, UBL’s leadership appears keen to downplay their performance. No press releases were issued when they posted the highest-ever quarterly profit by a bank on Wednesday, and none were issued today (Friday) when, after HBL’s results, it was evident that UBL had taken the number one slot. Instead, in an investor briefing on Wednesday, UBL President Muhammad Jawaid Iqbal clarified that the bank is not pursuing growth for the sake of a trophy. "We have no ambition to be No. 1," he remarked, adding that the bank would not mind slipping to No. 4 if that proved to be a more profitable position. Iqbal emphasized that UBL’s strategy remains laser-focused on acquiring "cheap" current account deposits rather than chasing high-interest, loss-making deposits simply to pad the balance sheet.

That said, it is entirely possible that HBL will take the deposit differential in stride. There is always a psychological tint to the “No 1” spot and HBL has built its brand equity over the years on being Pakistan’s biggest bank among other things. It has also leveraged its size to secure the lion's share of corporate mandates and government business.

But despite losing the deposits crown, HBL has been and still remains the biggest lender to Pakistan’s private sector. On top of that, HBL’s focus in recent times has clearly matured beyond headline rankings. The increased focus on agriculture lending in an environment where Pakistani banks are still slow on the uptake and their interest in promoting SMEs mean HBL is playing its own ballgame.

It is entirely possible and some analysts expect that HBL will at some point, though perhaps not immediately, take UBL on in a "deposit war." Since HBL's deposits fell this quarter, it suggests they may have been shedding expensive deposits to protect their own margins. But HBL is unlikely to allow UBL to cement this lead without a fight.

That said, HBL is a bank that has its own goals and philosophies. Perhaps that is why UBL is also underplaying the milestone, and HBL does not immediately seem too bothered.

Babar Nizami is Executive Editor, Profit at Pakistan Today. He can be reached via email at [email protected]. He tweets @Bnizami

View all articles →10 Comments

No comments yet. Be the first to join the discussion!