Beyond Hormuz

Pakistan’s Case for a Gulf-Owned Strategic Energy Reserve Corridor

The reopening of the Strait of Hormuz after the recent Gulf crisis brought immediate relief to energy markets, but it should not bring intellectual complacency. Reuters reported on June 19, 2026, that oil shipments through Hormuz had picked up after a U.S.-Iran ceasefire arrangement, with 25 commercial crossings recorded on June 18, still well below the pre-conflict level of about 120 daily crossings. That single comparison captures the core strategic problem: even when a crisis appears to be ending, shipping confidence, insurance availability, port clearance, mine-risk advisories and political uncertainty can lag behind the diplomatic headline.

For Pakistan, the lesson is more direct than for many other countries. According to Reuters reporting on a Pakistan government document, Pakistan depends on supplies through the Strait of Hormuz for up to 90% of its oil and LNG imports and lacks strategic petroleum reserves. The U.S. Energy Information Administration separately notes that in the first half of 2025, total oil flows through Hormuz averaged 20.9 million barrels per day, equivalent to about 20% of global petroleum liquids consumption and one-quarter of global maritime traded oil. In other words, Hormuz is not merely a Gulf problem. It is an Asian inflation problem, a South Asian balance-of-payments problem and a Pakistani national security problem.

The usual response to a crisis around Hormuz is diplomatic: de-escalate, escort shipping, reopen lanes, calm markets and wait for normalcy. That is necessary, but insufficient. The bigger question is how to reduce the world’s exposure to the next disruption. Pakistan’s opportunity lies not in pretending it can replace Hormuz, Fujairah, Rotterdam or Singapore. It cannot. Its opportunity lies in becoming a geographically nearby, politically friendly and lower-cost redundancy platform for Gulf producers that want to hold some crude, refined products or LNG outside their immediate conflict geography.

The Strategic Idea: From Transit Country to Reserve Host

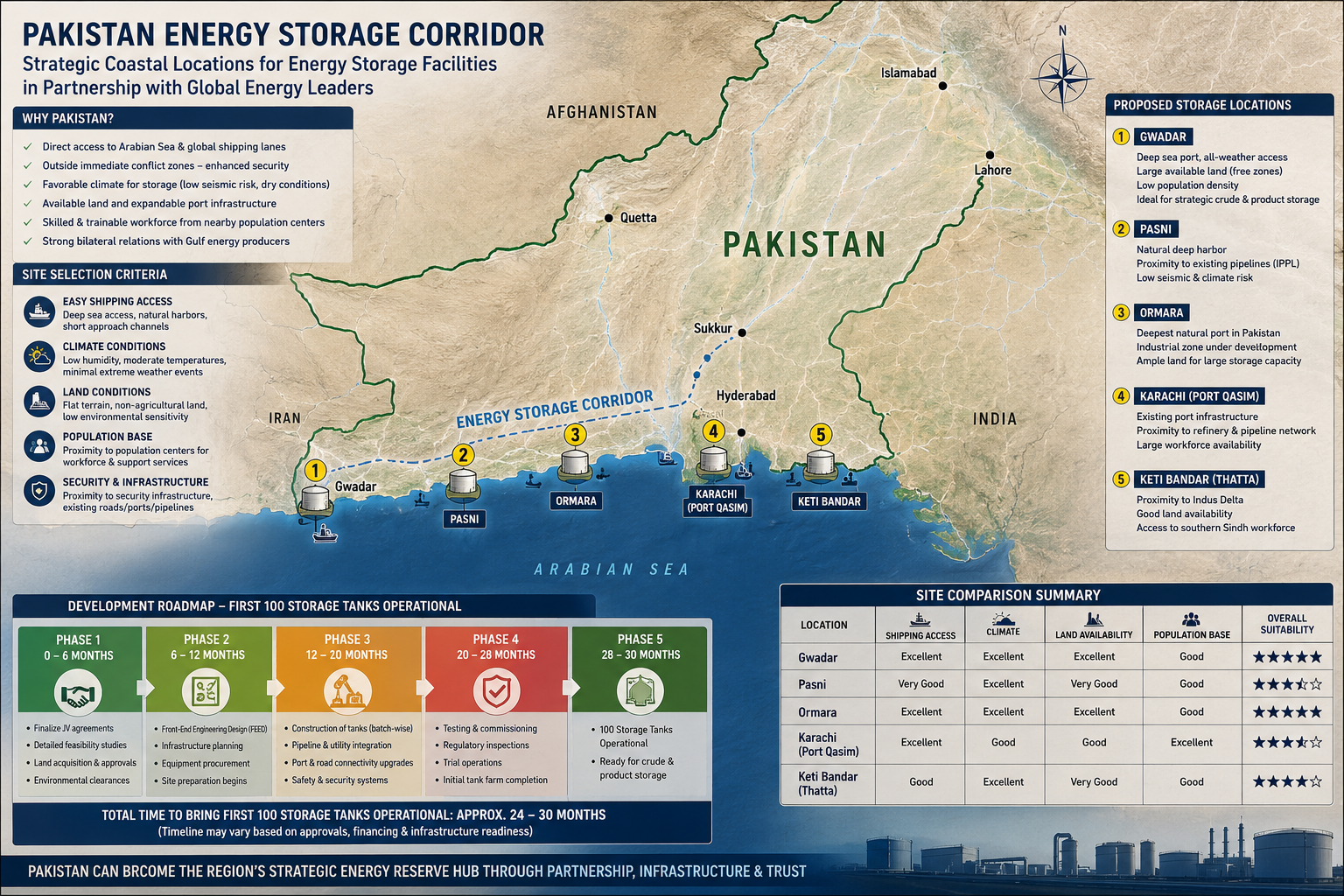

Pakistan should propose a “Pakistan Strategic Energy Reserve Corridor” stretching from Gwadar to Port Qasim, with selected nodes at Pasni, Ormara, Hub/Karachi and eventually Keti Bandar. The core concept would be simple: Saudi Arabia, the UAE, Qatar, Kuwait, Oman, Bahrain and potentially Iraq could own or jointly own dedicated storage assets on Pakistan’s coastline. The stored inventory would belong to the foreign national oil company or its JV vehicle. Pakistan would provide land, customs-bonded treatment, security, port access, utilities, long-term legal protections and emergency coordination. In return, Pakistan would receive foreign direct investment, lease income, port fees, throughput charges, skilled jobs, local infrastructure, technology transfer and negotiated emergency access rights for its own crises.

The proposal should not be framed as foreign sovereign territory. That phrase would create constitutional, political and public sensitivities in Pakistan and unnecessary geopolitical anxiety abroad. The better formulation is “treaty-backed bonded strategic reserve zones under Pakistani sovereignty.” This structure is closer to a special economic zone, a bonded warehouse regime, a long-term port concession and a bilateral emergency stockholding agreement. The International Energy Agency already recognizes that countries can hold emergency oil stocks abroad under bilateral arrangements that guarantee access during a crisis. Pakistan can learn from that principle without needing to become an IEA member or surrendering sovereignty over land.

This structure also answers a public concern: why should foreign countries store oil in Pakistan if Pakistan itself is energy insecure. The answer is that Pakistan should not borrow billions merely to fill tanks with imported oil. Instead, it should invite foreign-owned inventories to be held on Pakistani soil, while negotiating limited emergency draw-rights, first-refusal rights, rotation rights and domestic supply support during severe disruptions. This converts Pakistan from a passive importer into an active host of regional resilience.

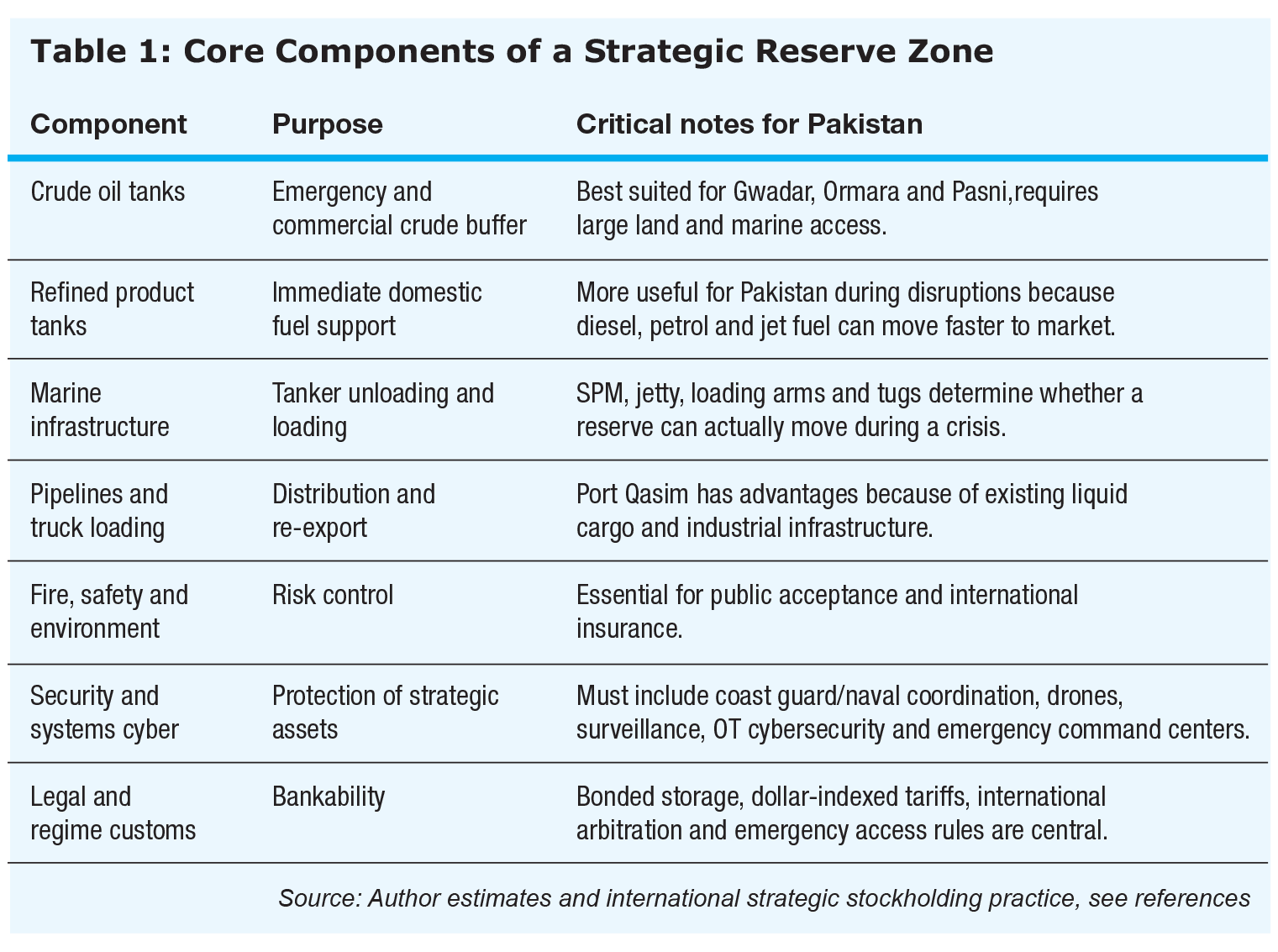

What Exactly Would Be Built

A strategic reserve is not simply a tank farm. A bankable reserve zone requires a complete energy security system: crude oil tanks, refined product tanks, firewater reservoirs, foam systems, bund walls, oil-water separators, pumps, pipelines, metering systems, control rooms, laboratories, security fencing, drones, radar, cybersecurity, truck loading bays, emergency response units, power backup, water supply or desalination, environmental monitoring, marine loading arms, jetties or single-point moorings, and a dispatch regime that determines who can move which product under normal and emergency conditions.

A large above-ground crude tank can hold about 500,000 to 1 million barrels. A 10 million barrel crude block therefore requires roughly 10 to 20 tanks depending on tank size. Refined products are more complicated because petrol, diesel, jet fuel and furnace oil cannot simply be blended at will, they require separate product tanks, quality controls and more frequent rotation. LNG is in a different category altogether. It requires cryogenic tanks, specialized insulation, boil-off gas handling, regasification equipment, safety exclusion zones and high-specification marine infrastructure. For Pakistan, crude and refined products should be phase one. LNG should be treated as a separate, more expensive Qatar/UAE/Oman track once the first petroleum corridor has credibility.

Cost: The Tank Is One Bill. The Oil Inside It Is Another

The most important analytical distinction is between infrastructure cost and inventory cost. A reserve project can look manageable when discussed as tanks and pipelines, it becomes far larger when the stored oil is included. Industry and policy estimates vary by site conditions, port access, land preparation, seismic design, environmental rules, imported equipment costs and security standards. As a rule of thumb, a coastal tank farm connected to marine infrastructure can cost tens of dollars per barrel of storage capacity before inventory is purchased. LNG costs are much higher: VINCI’s 2023 contract for a single 180,000 cubic metre LNG tank in the Netherlands was valued at €160 million, while the earlier Gate terminal in Rotterdam involved an €800 million investment for a regasification plant, two jetties and three 180,000 cubic metre tanks.

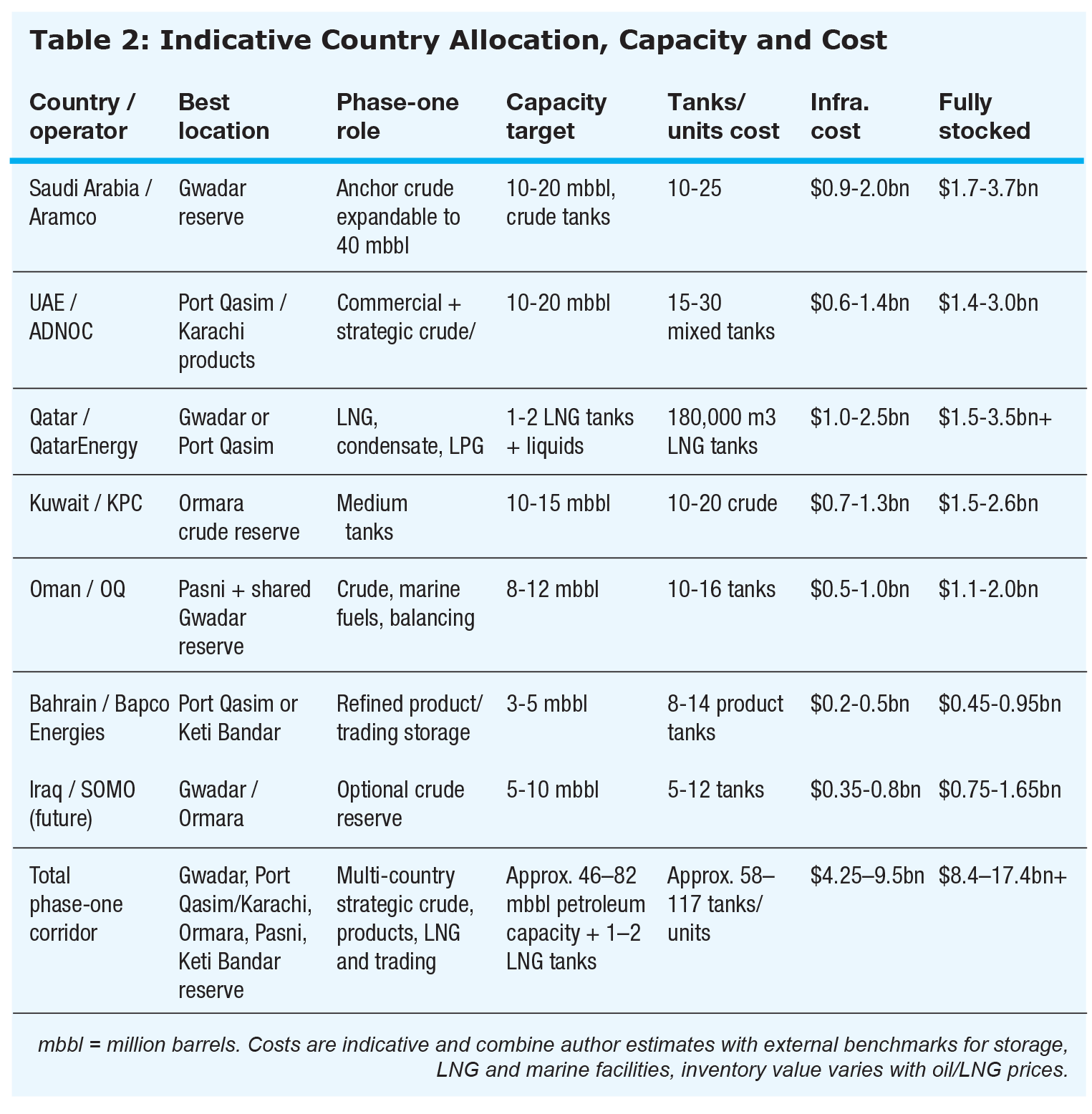

For the Pakistan corridor, a practical first-generation target should be 60 million to 80 million barrels of crude and refined products, not an immediate 200 million barrel mega-reserve. At an indicative infrastructure cost of $60 to $90 per barrel for greenfield coastal facilities and $40 to $65 per barrel for brownfield or semi-brownfield facilities, the first-generation petroleum corridor could require around $4 billion to $7 billion in physical infrastructure. Filling 60 million to 80 million barrels at $75 to $85 per barrel would require another $4.5 billion to $6.8 billion in inventory. Therefore, a realistic petroleum corridor could require $8 billion to $14 billion including stored oil, depending on product mix and phasing. If LNG is added at scale, the number rises materially.

This is why Pakistan should not finance the inventory itself. The infrastructure can be financed by foreign equity, project finance, port concession models, sovereign wealth funds and Pakistani JV participation. The oil and LNG inventory should be owned by Saudi Aramco, ADNOC, QatarEnergy, Kuwait Petroleum Corporation, OQ Oman, Bapco Energies or other participating companies. Pakistan’s contribution should be land, regulation, security, utilities and the political framework that makes the investment bankable.

Country-by-Country Reserve Allocation

The corridor should not treat every Gulf country in the same way. Saudi Arabia is the anchor crude investor. The UAE is the trading and refined-products partner. Qatar is the LNG and condensate specialist. Kuwait is a crude and refinery-linked reserve participant. Oman is the maritime-balancing partner with strong logic for Pasni and Gwadar. Bahrain is better suited to a smaller refined-products or shared reserve block. Iraq can be a later-stage participant if the corridor is positioned as a neutral South Asian energy platform rather than a GCC-only project.

Site Selection: Why One Location Is Not Enough

A single mega-site would defeat the purpose of redundancy. Pakistan should build a corridor, not a monument. Each site has a different logic. Gwadar offers land and strategic proximity to the Gulf, but it needs deeper supporting infrastructure, stronger local legitimacy and climate resilience planning. Port Qasim offers existing liquid cargo capability, including FOTCO and LNG-linked infrastructure, but faces land congestion, urban proximity and environmental constraints. Ormara offers strategic defensibility and distance from the Karachi urban belt, but requires more greenfield marine investment. Pasni offers a useful secondary node between Gwadar and Ormara, especially for Oman or shared Gulf facilities. Keti Bandar should be considered a long-term expansion zone, not the first anchor site, because it would require larger supporting investments.

Port Qasim is the fastest route to a credible first win. The Port Qasim Authority describes FOTCO as an oil terminal developed on a build-own-operate basis with an initial cost of $87 million, capacity of 9 million tonnes per year and potential growth to more than 27 million tonnes with three additional berths. It also notes that 77 acres have been earmarked for a POL storage tank farm. This does not mean Port Qasim alone can host the corridor, but it does mean Pakistan already has a liquid cargo base from which an ADNOC, Aramco or Bapco-led product reserve could move faster than a greenfield coastal site.

Gwadar is the strategic prize, but it should be sequenced carefully. The Gwadar Port Authority describes Gwadar as Pakistan’s third port intended to address limitations at Karachi and Port Qasim, including Karachi’s physical constraints arising from its location within the city. Gwadar also offers a free zone and expansion space. But the honest assessment is that Gwadar must first prove execution reliability: water, power, road access, local hiring, community buy-in, environmental safeguards, customs performance and port throughput. A Saudi-led 10 million barrel starter reserve is a more credible first move than a 50 million barrel announcement that sits on paper.

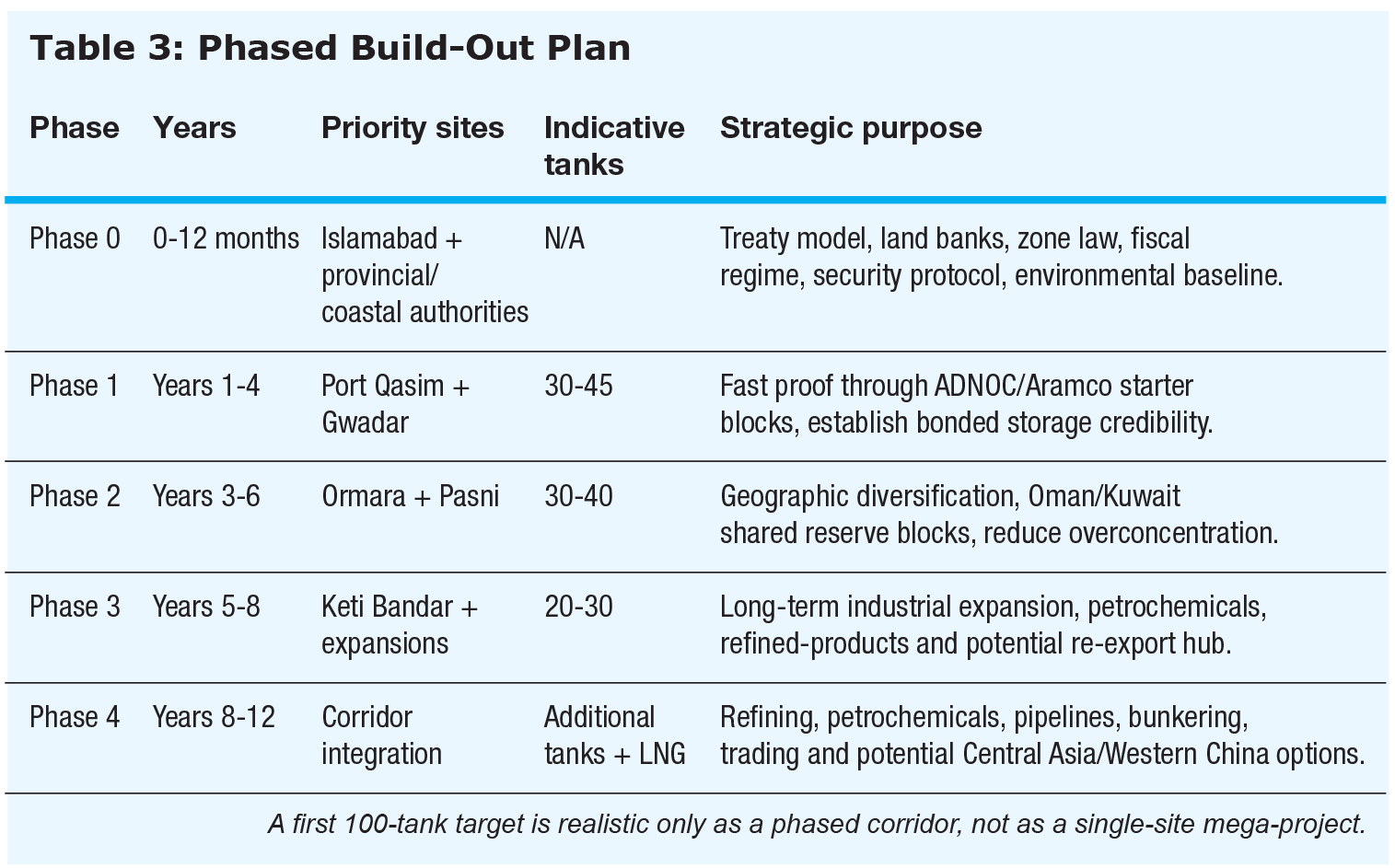

Timeline: First 100 Tanks, Not 100 Separate Sites

The phrase “first 100 storages” should be reframed as “first 100 tanks.” One hundred separate sites would be commercially irrational and impossible to secure. One hundred tanks across four to five properly designed coastal reserve zones is plausible. If the average tank is 500,000 barrels, 100 tanks create about 50 million barrels of storage. If the average is closer to 1 million barrels, 100 tanks create about 100 million barrels. A practical first target should be 60 million to 80 million barrels across mixed crude and refined-product capacity.

A credible timeline for the first 100 tanks is six to eight years, not two to three years. Port Qasim product storage can move faster because of existing infrastructure. Gwadar can deliver a strategic starter block if land, power, water and security are resolved early. Ormara and Pasni should come in phase two because they require more greenfield work. Keti Bandar should be treated as phase three. An aggressive fast-track could deliver the first 40 to 50 tanks within four years, but that requires treaty framework, land demarcation, environmental approvals, financing and marine design to be completed upfront.

A Corridor, Not an Enclave

Pakistan’s strongest legal proposition would have five layers. First, a Federal Strategic Energy Reserve Zones Act that defines bonded petroleum and LNG reserve areas, investor eligibility, customs treatment, safety standards, land rights, tariff regulation and emergency access. Second, bilateral government agreements with each participating country guaranteeing that foreign-owned stocks can be accessed by the owner during crisis, while also defining Pakistan’s domestic emergency rights. Third, concession agreements for the operating companies, whether 100% foreign-owned, JV-owned or public-private. Fourth, international arbitration and political risk insurance to reduce investor fear of policy reversal. Fifth, provincial/local development compacts to ensure that local communities see employment, training, health, water and contractor opportunities.

This model is better than a symbolic sovereign corridor because it is more legally acceptable and more financeable. Investors do not need flags over their tank farms,they need enforceable rights, secure access, dollar-indexed tariff recovery, operational autonomy, predictable taxes, customs clarity, insurance acceptance and crisis protocols. Pakistan does not need to give up sovereignty,it needs to give up policy unpredictability.

What Pakistan Would Earn

The economic case is not merely rental income. During construction, a first-generation corridor could generate tens of thousands of jobs in civil works, steel fabrication, pipeline installation, marine construction, electrical systems, safety systems, surveying, trucking, port services and security. During operations, the permanent job base would be smaller but higher quality: terminal operators, maintenance engineers, instrumentation technicians, safety officers, environmental monitors, customs specialists, port logistics planners, cybersecurity teams and emergency responders.

The larger value would come from ecosystem formation. If Pakistan hosts credible storage for Aramco, ADNOC, QatarEnergy, KPC, OQ and others, supporting industries will follow: inspection companies, calibration labs, marine service firms, bunker suppliers, tank cleaning specialists, insurance surveyors, energy trading desks, refinery upgraders, pipeline operators and industrial training institutions. That is how storage hubs become economic hubs. Fujairah did not become important merely because it had tanks, it became important because storage, bunkering, trading and shipping reinforced one another.

Pakistan should also negotiate knowledge transfer. Every JV should include Pakistani engineering apprenticeships, emergency response training, scholarships, local university partnerships, port management training, industrial cybersecurity programs and minimum local procurement thresholds. Without this, the corridor risks becoming a fenced-off foreign asset that creates resentment. With it, the corridor can become a coastal industrial capability program.

Why the Idea Could Fail

The largest risk is not engineering. It is credibility. Gulf investors will ask whether Pakistan can maintain a 30- to 50-year policy framework across multiple governments, currency crises, IMF programmes and changes in petroleum taxation. They will also ask whether Pakistan can protect critical infrastructure during political unrest, insurgency, cyberattacks or regional conflict. If the answer is uncertain, the project will not move beyond memoranda of understanding.

The second risk is local legitimacy. Gwadar and the Makran coast cannot be treated as empty land. Fishing communities, water stress, climate vulnerability and local employment expectations matter. The Makran coastline also faces seismic and tsunami hazards associated with the Makran subduction zone, which means site design must include robust geotechnical, coastal flooding, storm surge and emergency evacuation planning. A reserve corridor that ignores local communities will face political resistance. A reserve corridor that visibly improves local water, training, health, roads and jobs will gain durable acceptance.

The third risk is geopolitical perception. India may view large Gulf-owned reserves in Pakistan through a strategic lens. China may welcome investments that strengthen Gwadar, while the United States may scrutinize the role of Chinese-linked infrastructure. Gulf states will not want the corridor to look anti-Iran. Pakistan must therefore present the project as neutral energy resilience for South Asia, not as a military asset or bloc project. The more commercial and legally transparent the model, the less vulnerable it becomes to geopolitical suspicion.

The fourth risk is competition. Fujairah, Singapore and Rotterdam already have deep credibility. Pakistan cannot compete with them by claiming instant hub status. It must compete on a specific proposition: Gulf-owned emergency and commercial stocks located close to South Asian demand, outside the immediate Gulf conflict geography, on lower-cost land, with treaty-backed access and potential linkage to Pakistan’s own demand, Western China and Central Asia. That is a narrower but stronger claim.

The Best Case Vision - Build Pilots First, Scale Toward a $35 Billion Corridor

Pakistan can begin with a vision for a $35 billion mega-project announcement. However, it should start with two bankable anchor projects. The first should be a Saudi Aramco-led Gwadar Strategic Crude Reserve of 10 million barrels, expandable to 30 million barrels. The second should be an ADNOC-led Port Qasim Commercial and Strategic Product Reserve of 10 million to 15 million barrels. These two pilots would test both strategic and commercial models: Gwadar as the long-term reserve hub and Port Qasim as the faster operational trading/product hub.

Once those two are bankable, Oman can be brought into Pasni or a shared Gwadar-Pasni block, Kuwait can be offered Ormara, Qatar can be offered LNG and condensate, Bahrain can join a refined-product block at Port Qasim or Keti Bandar and Iraq can be considered as a later optional participant. Two or more countries can share a zone, but they should not share legal ambiguity. Each country’s tanks, inventory ownership, access rights, insurance responsibilities and emergency drawdown rights must be ring-fenced. Shared jetties, utilities, fire systems and security can reduce cost by 15% to 25%, but shared assets only work if dispatch priority and crisis rules are settled in advance.

The Lesson of Hormuz

The recent crisis has shown that energy security is no longer only about who produces oil. It is about where oil is stored, how quickly it can move, who controls the route, how markets price political risk and how much redundancy exists when a chokepoint becomes uncertain. The Strait of Hormuz will remain central to world energy. But the smarter strategic response is to build buffers around it.

Pakistan’s coastline gives it a rare opportunity to move from being a vulnerable importer to becoming a host of regional resilience. The idea is ambitious, but not fanciful. The IEA stockholding framework already recognizes the principle of stocks held abroad under bilateral agreements. Pakistan is already discussing bonded storage and strategic petroleum reserves with major oil companies and trading firms. Port Qasim already has liquid cargo infrastructure. Gwadar has the land and strategic location. The missing element is not geography, it is execution credibility.

If Pakistan turns this idea into another headline without legal clarity, local legitimacy and phased financing, it will fail. If it builds a serious treaty-backed, bonded, Gulf-financed strategic reserve corridor, it can attract investment, create jobs, improve energy security, transfer knowledge and make its coastline central to the next generation of South Asian energy resilience. The end of the crisis should not end the conversation. It should begin the build-out.

The writer is an NDU alumni, Stanford GSB Lead 26 & a digital health innovator

View all articles →Comments

No comments yet. Be the first to join the discussion!