Customs Directorate revises import values for perfumes from all origins

Customs values for imported perfumes, eau de toilette and eau de cologne have been revised under Valuation Ruling No. 2094/2026; New C&F rates apply by brand categories and PCT codes, with exceptions for certain sister-concern imports

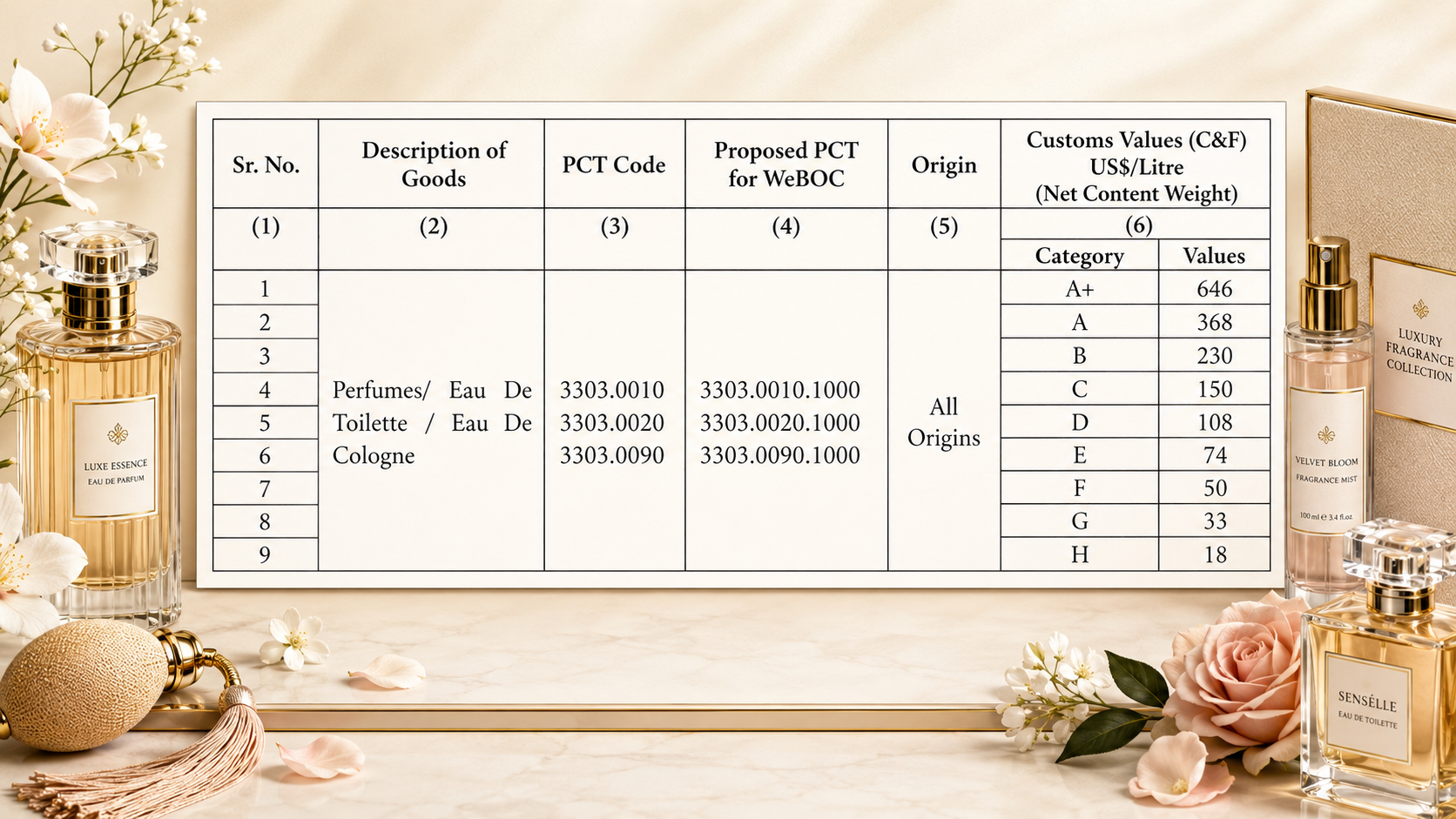

The Directorate General of Customs Valuation has revised customs values for imported perfumes, eau de toilette and eau de cologne from all origins. The new values have been issued through Valuation Ruling No. 2094/2026, under Section 25A of the Customs Act, 1969.

The ruling supersedes Valuation Ruling No. 1840/2024, dated January 12, 2024.

According to the ruling, the earlier values had remained in the field for a considerable period and required review due to changes in international prices, import trends, declared values, brand categories, market conditions and the overall valuation position of the goods.

The Directorate held stakeholder meetings on March 18 and April 8, 2026, where issues related to valuation of perfumes, eau de toilette and eau de cologne were discussed.

Stakeholders were asked to submit import invoices, sales tax invoices, import data, market evidence, price lists and other documents to support their declared transaction values.

The Directorate said it reviewed stakeholder submissions and available import data with reference to declared values, assessed values, description of goods, brand categories, origin, quantity, packing size and other relevant factors.

Market enquiries were also conducted to determine prevailing prices of the goods.

The ruling said the transaction value method could not be solely relied upon due to variation in declared values and absence of complete and verifiable information. Identical and similar goods methods were also found insufficient because of differences in brands, categories, packing sizes, commercial levels, declared values and market positioning.

The computed value method was also not applied due to non-availability of credible data on material costs, manufacturing expenses, conversion costs, overheads and related expenses in the country of export.

The customs values were therefore determined under Section 25(9) of the Customs Act, 1969, read with Section 25(7) and Rule 121(2) of the Customs Rules, 2001.

Under the new ruling, A+ category perfumes, covering premium, luxury and niche brands, have been valued at $646 per litre on C&F basis.

A category perfumes, covering high-end designer brands, have been valued at $368 per litre, while B category, covering upper mid-tier designer brands, has been set at $230 per litre.

C category perfumes, covering mid-tier designer brands, have been valued at $150 per litre, while D category, covering lower mid-tier and mass premium brands, has been fixed at $108 per litre.

E category perfumes, covering mass and drugstore designer brands, have been valued at $74 per litre.

F category, covering local premium and boutique perfumes, has been set at $50 per litre, while G category, covering local and mass Pakistani brands, has been valued at $33 per litre.

H category, covering all other, generic and unbranded perfumes, has been fixed at $18 per litre.

The ruling applies to goods falling under PCT codes 3303.0010, 3303.0020 and 3303.0090, with separate proposed PCTs for WeBOC.

The Directorate clarified that the revised values will not apply to imports made directly by multinational companies from sister concerns of the same name. Such consignments will be assessed under Section 25 of the Customs Act, 1969 and kept under close watch.

Any anomaly in such consignments will be reported to the Directorate General.

For brands not mentioned in the ruling, clearance Collectorates may assess values using the identical or similar goods method under Section 25(5) and 25(6) of the Customs Act, 1969.

If an item is imported in a gift or kit set, each item in the set will be assessed separately according to values mentioned in the relevant valuation rulings.

Variants of listed brands that are not separately mentioned in the ruling will be assessed on the value determined for the main brand.

The ruling further states that where declared or invoice values are higher than the customs values fixed in the ruling, assessment will be made on the higher value under Section 25(1) of the Customs Act, 1969.

For consignments imported by air, the difference between air freight and sea freight will be added for assessment.

The Collectorates of Customs have been directed to implement the valuation ruling and report any anomaly to the Directorate immediately.

Comments

No comments yet. Be the first to join the discussion!