Customs Directorate revises ammunition valuation, adds .22 and .222 calibre categories

New ruling includes ELEY brand ammunition from the UK and replaces Valuation Ruling No. 2036/2026 after stakeholder consultations and market review

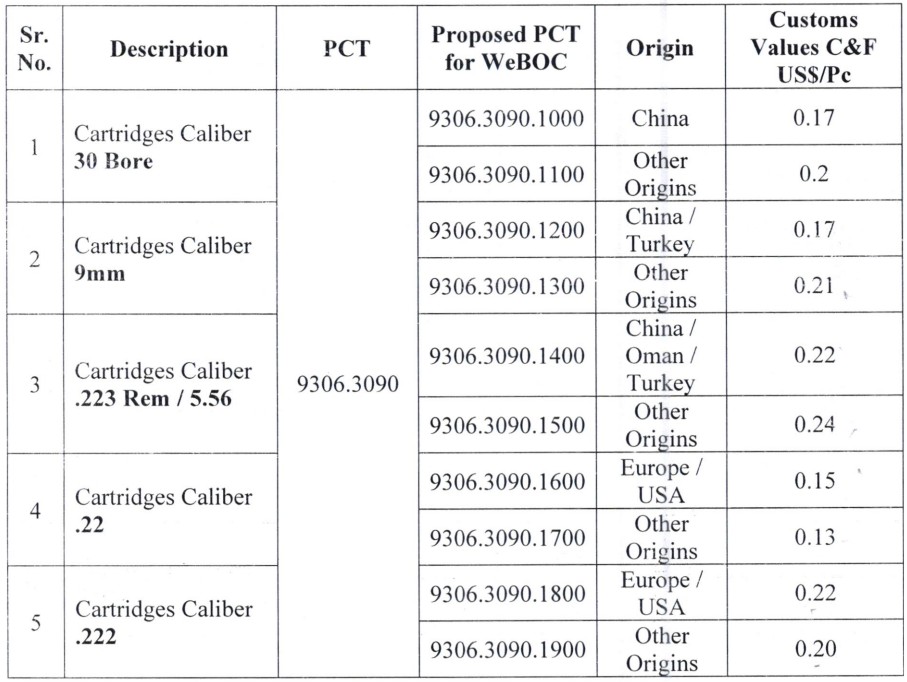

The Directorate General of Customs Valuation has revised customs values for imported ammunition and incorporated new categories, including .22 calibre ammunition of the ELEY brand from the United Kingdom and .222 calibre ammunition, through Valuation Ruling No. 2087/2026.

The new ruling supersedes Valuation Ruling No. 2036/2026 dated January 16, 2026, and will remain in force until revised or rescinded under Section 25A(4) of the Customs Act, 1969.

According to the ruling, the revision was initiated after representations were received from M/s Bandookwala and other stakeholders seeking inclusion of .22 calibre ammunition, particularly ELEY brand ammunition of United Kingdom origin, which had not been specifically covered under the previous valuation ruling.

Stakeholders also requested the inclusion of .222 calibre ammunition and sought a review of customs values for ammunition already covered under the existing ruling in light of prevailing market trends, available declared values and current assessment practices.

To determine revised customs values, the Directorate conducted a valuation exercise under Section 25A of the Customs Act, 1969. A meeting with relevant stakeholders was held on April 30, 2026, attended by representatives of M/s Bandookwala and other importers.

During the consultations, M/s Bandookwala informed customs authorities that it imported ELEY brand .22 calibre ammunition from the United Kingdom at actual transaction values that were significantly higher than those declared by some other importers for comparable products.

The company requested the inclusion of ELEY brand ammunition in the valuation ruling to ensure uniform assessment and address concerns relating to under-invoicing. Other stakeholders supported the inclusion of .222 calibre ammunition and called for a revision of existing customs values based on market conditions and available import data.

The Directorate asked stakeholders to provide supporting documents, including import records, invoices, sales tax invoices, market evidence and other documentary material to substantiate their claims and declared values.

As part of the review process, customs authorities examined available import data, scrutinising declared values with reference to product descriptions, calibre, brand, country of origin, quantity and invoice values.

According to the ruling, analysis of import records showed that importers other than M/s Bandookwala had declared and imported ELEY brand .22 calibre ammunition from the United Kingdom at values considerably lower than those declared by M/s Bandookwala for comparable goods.

Market inquiries were also conducted to determine prevailing market prices for ammunition of different calibres, brands and origins. The Directorate compared import data, invoice values, reference values, stakeholder submissions and market inquiry findings before finalising the revised customs values.

The ruling states that customs authorities evaluated valuation methods prescribed under Section 25 of the Customs Act, 1969 in sequential order before determining the values.

The transaction value method under Section 25(1) was examined but could not be relied upon because of wide variations in declared values and the absence of complete and verifiable information in some cases.

The identical goods method under Section 25(5) and the similar goods method under Section 25(6) were also considered. However, customs authorities found significant variations in declared values, quantities and commercial levels, limiting their applicability.

The computed value method under Section 25(8) was reviewed but could not be applied due to the unavailability of credible and verifiable information regarding production costs, manufacturing expenses, overheads and related costs in exporting countries.

As a result, the Directorate determined customs values under Section 25(9), read with Sections 25(5), 25(6) and 25(7) of the Customs Act, using available import data, market inquiries and other relevant information.

The Directorate stated that the revised values were determined after considering prevailing market trends, stakeholder submissions and customs assessment practices.

Under the ruling, importers may file a revision petition under Section 25D of the Customs Act, 1969 before the Director General Customs Valuation within 30 days of the issuance of the valuation ruling.

Comments

No comments yet. Be the first to join the discussion!