PTCL closes Telenor deal, rises to second-largest telecom

The next telecom battle to be fought on the 5G front

PTCL announced on Wednesday that it has completed its Rs 108 billion acquisition of Telenor Pakistan and Orion Towers, a deal that reshapes the country's telecom landscape.

The transaction brings both companies under full PTCL ownership, joining Ufone and U Microfinance Bank in the group's portfolio. Telenor Pakistan and Ufone will now be merged into a new entity, tentatively called MergeCo, which will operate as a wholly-owned PTCL subsidiary.

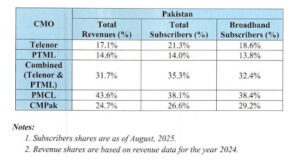

The acquisition vaults PTCL into second place among Pakistan's telecom providers. Jazz remains the market leader with 38% of subscribers, but PTCL now commands 35%, up from its previous position. Zong trails at around 26%.

Looking ahead, PTCL has signaled its intention to bid in the upcoming spectrum auction, with ambitions to expand bandwidth and roll out 5G services. How aggressively the company can pursue new spectrum remains uncertain, however, given the debt it has taken on to finance the Telenor deal and broader industry concerns about spectrum pricing.

Concerns around the deal

This deal was a long time coming. There were concerns about this merger potentially leading to a more monopolized telecom landscape by further consolidating the market into fewer companies.

Those wary of the proposed merger argued that it would strengthen PTCL’s position, where it could cross-subsidize PTCL and Ufone, and with expanded reach could push the competition out, or at least put them under heavy pressure.

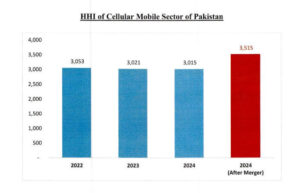

In fact, PTA’s official estimates and calculations show how this proposed merger would impact the market concentration in the local telecom industry. Herfindahl Hirschman Index (HHI) is a metric that measures this concentration. An HHI value of 10,000 means that there’s a monopoly in place, while a value of 0 signifies a highly competitive market. In Pakistan’s telecom industry’s case, the HHI value has been hovering around 3000 for the past 3 years. But, if this merger were to occur, it was estimated that the HHI value would rise to 3515, making the market more concentrated.

At the same time, the Competition Commission of Pakistan (CCP) had raised concerns about the lack of transparency in PTCL’s investment post-merger plans. Questions were also raised about the company’s business conduct, and discrepancies in data related to international direct dialling (IDD) services were highlighted.

The concerns, however, were allayed – at least on paper, and PTCL was able to obtain approval from the CCP and an NOC from the Pakistan Telecom Authority (PTA). The reasoning given by the CCP was that the merger was conditional upon certain safeguards to preserve competition.

These included, among other things, the provisions that PTCL and the merged entity would have separate boards; that an independent third party reviewer would monitor compliance and audit transactions and submit quarterly reports to the CCP for 5 years; that PTCL would ensure non-discriminatory access to capacity and infrastructure for all operators and pricing would be subject to PTA’s approval; that CCP reserved the right to divest assets in case of violations, and so on.

The deal was funded primarily by a USD 400 million loan from a consortium led by the International Finance Group, the World Bank’s private sector arm. Beside giving PTCL a higher market share, this merger has also given it access to more revenues. In 2024, while PTCL reported total revenues of Rs 219.7 billion, Telenor posted a figure of Rs 123 billion. On the surface, this would mean more than a 50% increase in revenues. The deal would obviously also expand the infrastructure network owned or managed by PTCL, a fresh, perhaps much-needed, injection into this company that has been making losses for the past few years now.

Persisting fears

In fact, one of the issues which remains to be seen is how this deal will impact the profitability of PTCL, which in 2024 had posted a loss of over Rs 14 billion. Would access to more money be the solution? It could be well a part of it, but surely on its own it is probably not sufficient to turn the company’s fortunes around. In fact, earlier this year, the Central Monitoring Unit (CMU) of the Ministry of Finance had warned that if the acquisition was not properly managed, it might impede the group’s digital transformation goals and erode its ability to effect and sustain investments in its key growth areas.

The merger does promise to provide substantial operational savings, with the merger of the tower infrastructure into a single grid. Similarly, Telenor’s strength in rural and northern areas combined with Ufone’s urban and southern coverage, would likely create a truly nationwide reach. But, as the CCP had mentioned, “these [efficiencies] are neither assured nor independently verifiable in their current form”. And PTCL’s record with transparency hasn’t been exactly stellar.

We cannot ignore, at the same time, the fears of the rise of a nascent monopoly in the form of PTCL. Since four players (Jazz, PTCL, Telenor, Zong) have become three, what is to prevent three from becoming two, and two from becoming one?

Given that PTCL, beside being a telecom giant, is also the major provider of IP bandwidth, holding 64.5% of the market share (the rest is held by Transworld Associates), a margin differential would seep in, with PTCL’s competitors Jazz and Zong forced to access it at market rates. Over time, this could strengthen PTCL’s position at the expense of its competitors’. Whether the safeguards CCP put in place would prove effective in preventing this from happening, only time would tell.

One thing that we can predict with fair certainty, however, is that in the short term this merger would - by providing transparency regarding PTCL - remove a major roadblock to the spectrum auction for 5G services in Pakistan.

5G spectrum auction

A spectrum, essentially, is the range of frequencies upon which wireless signals can be carried. Within a spectrum are certain bands of the said frequencies, with lower bands suited for maximum coverage, while higher bands leading to greater transmission speeds. So, a given spectrum has multiple bands, each suited for a particular purpose.

In Pakistan, the current spectrum is 274 MHz. It is not a lot, especially when we take into context the size of our population (250 million). For some context, Bangladesh, which has a population of around 175 million, operates within a spectrum of 600 MHz.

What a smaller spectrum essentially does is restrict capacity. A broader spectrum means more frequencies can be used to produce more capacity to meet rising demand, and support digital transformation goals across industries.

The government now plans to auction 600 MHz of total spectrum, increasing by more than twofold our current spectrum capacity. Within this new spectrum, the government would also be auctioning newer bands. The bands planned to be auctioned include: 700MHz, 1800MHz, 2100MHz, 2300MHz, 2600MHz and 3500MHz. The 2600MHZ band is considered to be the most suitable for 5G, and it is expected that 190MHz of the total 600MHz spectrum would be offered from this band.

The auction is expected to take place in February 2026, with an improvement expected in the quality of 3G and 4G services, to be followed by the rollout of 5G services. Although concerns had been raised by telecom operators regarding the viability of rolling out 5G – the underutilization of 5G, the dearth of 5G compatible devices, and so on – the government in its bid to usher in a new chapter in Pakistan’s digital landscape is sold on increasing capacity, aiming for the availability of a minimum 100 Mbps of capacity to users over the next five years.

What can we predict?

In light of this impending spectrum auction, we can predict some possible scenarios of how this proposed merger could unfold.

The first is where, even though MergeCo survives, fundamental structural problems persist. The infrastructure investment remains insufficient, and despite a marginal improvement in service, it is no match for regional peers. Ultimately, this might lead to the consolidation of the market in even fewer hands.

The second possible way the merger could develop is by jolting the policymakers into instituting comprehensive reform. Taxes on ICT could be reduced from the current 34.5% to the regional normal of 20-25%. Other policies such as adopting GSMA’s recommendations of spectrum pricing, significantly lowering reserve prices, and cost-reducing infrastructure sharing policies, could eventually lead to a more sustainable ecosystem, where there might actually be competitive development in the local digital infrastructure.

The third way is where although the merger proceeds, the broader policy failures offset these benefits. The government prioritizes - in the spectrum auction - its own revenue at the cost of encouraging sector sustainability. While the operators bid, the financial pressures stretch them thin, and though the spectrum is allotted, the deployment fails to deliver on its promises.

Yet, whatever it may portend, PTCL’s acquisition of Telenor at least positions it, through its new subsidiary MergeCo, to be a meaningful participant in Pakistan’s 5G spectrum auction. Given its increased market share with the considerable bulk of Telenor now under its fold, PTCL’s consolidated financial status and the expanded depth of its current bands means that it is well-poised as a strong 5G deployer, should things work out.

2 Comments

No comments yet. Be the first to join the discussion!