What does the continued closure of the Strait of Hormuz mean for Pakistan?

On February 28, 2026, U.S.-Israeli airstrikes on Iran set off a chain of events that effectively sealed one of the most important 21-mile stretches of water on Earth. Within days, over 150 tankers had anchored outside the Strait of Hormuz rather than risk transit. Maersk, Hapag-Lloyd, and MSC suspended sailings. Not just that but shipping diversions surged 360%. To add insult to injury, oil prices jumped 10–13% in the first week alone.

For most of the world, this is a serious disruption no doubt. But for Pakistan, it is something closer to an existential economic crisis — one unfolding in slow motion across four interconnected pressure points: energy, fertilizer, labor, and technology. Let’s go by it sector by sector.

There is no petroleum cushion

Pakistan’s structural position going into this crisis was already precarious. The country imports 80–85% of its petroleum requirements, with the vast majority of those shipments historically routed through the Strait of Hormuz before reaching Karachi and Port Qasim. Its strategic petroleum reserves cover roughly 10 to 14 days of normal consumption. This is in sharp contrast to India’s significantly larger buffer, something that should trigger concern in those concerned with national security.

Then there is LNG. Pakistan has been importing liquefied natural gas since 2015 as domestic gas reserves have declined, and LNG now powers nearly a quarter of the country’s electricity. The problem is where that gas comes from: Qatar and the UAE together account for 99% of Pakistan’s LNG imports. Both countries’ export infrastructure now sits inside a closed maritime corridor, with QatarEnergy having halted production entirely and declared force majeure on its contracts.

“Pakistan and Bangladesh have limited storage and procurement flexibility, meaning disruption would likely trigger fast power-sector demand destruction rather than aggressive spot bidding.” — Go Katayama, Principal Insight Analyst, Kpler

That phrase “demand destruction” is a clinical way of saying rolling blackouts. Not just higher electricity bills but actual loss of power to homes, shops, hospitals, and factories.

Every $10 increase in global oil prices raises Pakistan’s annual petroleum import bill by approximately $1.8–2.0 billion. In the worst-case scenario, analysts at PIDE (Pakistan Institute of Development Economics) have warned that a three-month disruption could push oil to $120–$150 per barrel and raise Pakistan’s monthly oil import bill to between $3.5 and $4.5 billion; this would consume the country’s foreign exchange reserves at catastrophic speed.

The government’s response has included: a four-day workweek for government employees, two-week school closures, a ban on in-person government meetings, caps on wedding guest lists, and — most jarring — the largest fuel price increase in the country’s history. Petrol jumped 20% in a single week.

Pakistan is also attempting to reroute crude purchases. A Pakistan National Shipping Corporation vessel has reached Saudi Arabia’s Red Sea port of Yanbu and is heading to Karachi with 73,000 tonnes of crude. It is a creative workaround, but an expensive and uncertain one — especially since the Red Sea route now faces increased risk of Houthi attacks (in solidarity with Iran), and routing entirely around Africa’s Cape of Good Hope adds weeks and millions of dollars per voyage.

Fertilizer is a crisis within the crisis

Roughly one-third of global seaborne fertilizer trade passes through the Strait of Hormuz. The Gulf is not only one of the world’s primary production regions for fertilizers, but also facilitates a good chunk of trade for it as well. Cheap natural gas from Qatar and Saudi Arabia provides the feedstock for nitrogen fertilizers like urea and ammonia. When the gas stops flowing, so does fertilizer production. This is dire for Pakistan as many powerplants in the country heavily rely on Qatari LNG to meet their operational needs.

Pakistan’s domestic fertilizer producers have been forced to curtail output. At the same time, imported urea prices have already risen roughly 25% since the conflict began, reaching around $591 per tonne globally. That figure is climbing, and it is yet to be seen if Pakistan can rely on other major trading partners to address the shortfall.

The timing also presents challenges. The closure happened during Pakistan’s pre-Kharif planting window — the months when farmers lock in fertilizer purchases for the summer crop cycle, which produces the bulk of the country’s wheat, rice, cotton, and sugarcane. If farmers reduce fertilizer use now, it’s reasonable to expect yields to fall in six months. And lower yields mean higher domestic food prices, reduced rice and agricultural exports (two of Pakistan’s primary foreign exchange earners). It also deepens food insecurity in a country already suffering food hyper-inflation.

“Oil powers cars. Nitrogen powers crops. If the Strait of Hormuz closes, the most consequential price may not be Brent crude but the cost of feeding the world.” — The Conversation / UN University

The remittance lifeline is under threat

Pakistan’s economy has often been described as running on three main engines: exports, foreign borrowing, and remittances. Of the three, remittances from the Gulf are both the most substantial and the most vulnerable right now.

Approximately 4.9 million Pakistanis work in GCC countries; they are the second-largest expatriate community in the Gulf after India. In February 2026 alone, Pakistan received $3.3 billion in foreign remittances, with the UAE and Saudi Arabia contributing the top two shares at $696 million and $685 million respectively. The full-year projection stood at $38 billion — a lifeline that has kept Pakistan’s current account and foreign reserves from collapsing during repeated economic crises.

Iranian strikes have targeted energy facilities, airports, and commercial infrastructure across parts of the Gulf, including areas near Dubai’s Jebel Ali port. Even Dubai International Airport (the world’s busiest airport) has been forced to temporarily suspend operations. Hotels, construction projects, and retail businesses across the UAE and Qatar have also experienced disruptions. These sectors happen to employ large numbers of Pakistani blue-collar workers, particularly in construction, hospitality, and logistics.

If remittance flows were to fall by even 30–40%, Pakistan could face a monthly gap of roughly $500–700 million. In a more catastrophic scenario, wherein the Gulf economies face broader economic disruption, the shortfall could move closer to $1.5 billion per month. Combining falling remittance inflows with increased reliance on imports, the pressure on foreign exchange reserves could escalate quickly, potentially forcing emergency discussions with the IMF.

There is also a human dimension that economic analysis tends to paper over. Millions of families in Lahore, Karachi, Multan, and smaller cities depend directly on monthly transfers from fathers, sons, and brothers working in Riyadh, Dubai, and Doha. For those families, the Gulf crisis isn’t just another geopolitical development — it determines whether school fees get paid, rent is covered, and basic household expenses can be met in the coming months.

There is a crisis in tech as well

The technology impact on Pakistan is less dramatic than the others, but it is real and compounding.

Pakistan’s IT sector has been one of the country’s genuine recent success stories: it contributes via growing exports, establishing a large freelancer base (already under threat of unemployment thanks to AI), and increasing foreign exchange contributions. It is also a sector with specific dependencies on the Gulf supply chain that are now strained.

Most IT hardware entering Pakistan — servers, networking equipment, consumer electronics — transits through Dubai’s Jebel Ali port, the Middle East’s largest container hub. With Jebel Ali partially disrupted by Iranian strikes and now congested with diverted cargo that cannot reach Gulf-side ports, inbound hardware shipments face delays, surcharges of $2,500–$3,500 per container, and deep uncertainty about routing timelines. One could argue that Pakistan’s technology importers are navigating the most disrupted logistics environment since the COVID-19 pandemic.

More acutely, Pakistan’s IT sector depends on reliable power. Remote workers, software houses, data centers, and the freelancers contributing to foreign exchange earnings all need stable electricity — which has always been a consistent problem and is now at further risk from the LNG shortfall. Prolonged rolling blackouts would hit Pakistan’s tech export capacity directly and sharply.

There is also a cloud infrastructure dimension. Pakistani businesses and developers rely heavily on Microsoft Azure and AWS nodes hosted in the UAE and Qatar as their nearest low-latency cloud infrastructure. Both providers have reported latency issues and service disruptions at Middle Eastern nodes following strikes on Gulf facilities. For a sector that runs on connectivity and uptime, even degraded digital infrastructure is a meaningful operational setback.

The effects will compound

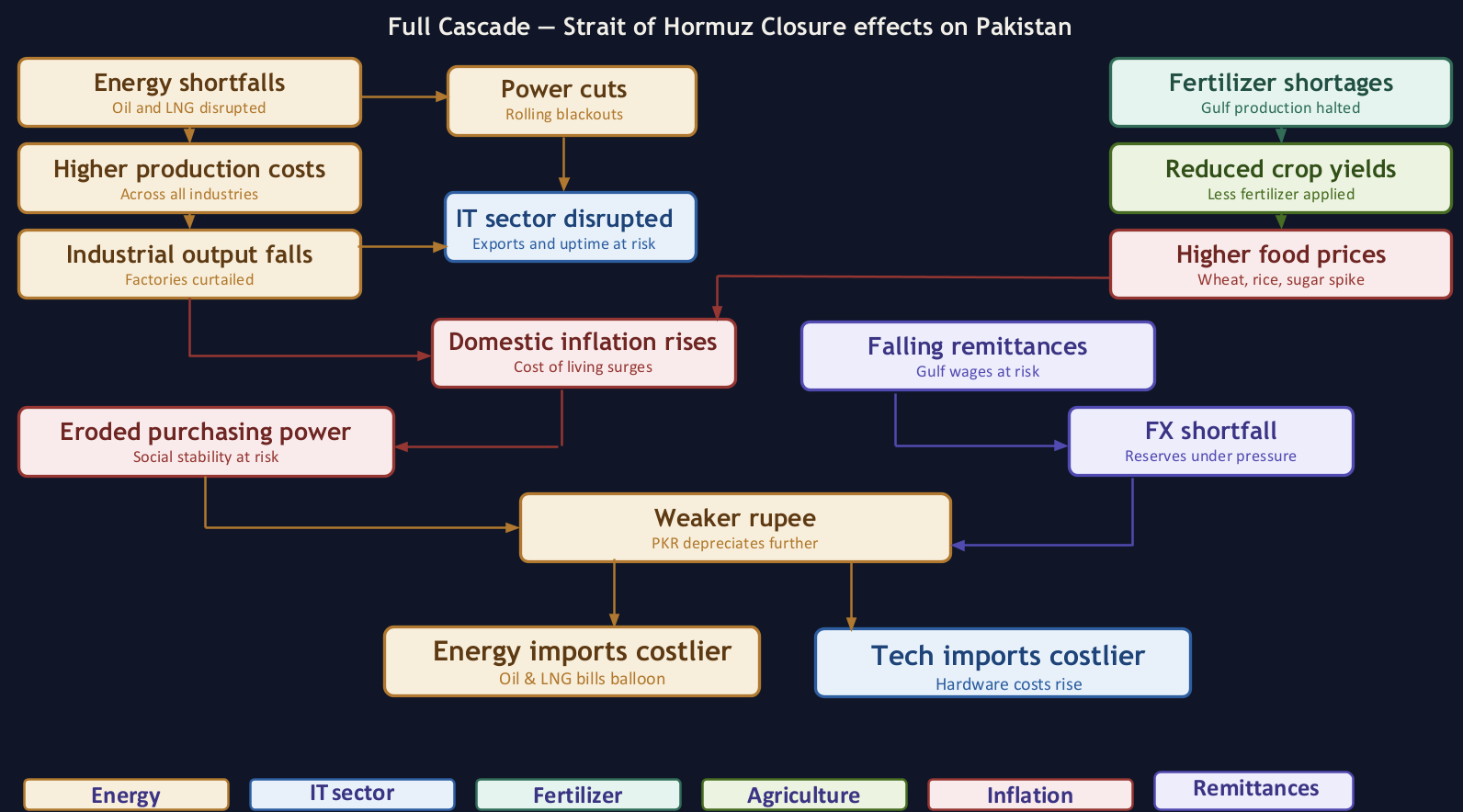

What makes Pakistan’s position uniquely fragile is not any single one of these channels in isolation — it is how they reinforce each other.

Energy shortfalls raise production costs and cause power cuts. Power cuts hit industrial output and the IT sector. Fertilizer shortages reduce agricultural yields and increase food prices. Higher food prices increase domestic inflation, eroding purchasing power and social stability. Falling remittances reduce the foreign exchange available to pay for energy imports. A weaker rupee makes energy and technology imports more expensive in local currency terms, thus worsening the trade deficit even more.

Analysts at Pakistan Institute of Development Economics have modeled a three-month maximum-intensity disruption scenario and arrived at cumulative losses approaching $9 billion. This is much more devastating than the balance-of-payments crises in the past that have repeatedly forced Pakistan to the IMF for emergency support.

Pakistan entered this crisis with 10–14 days of petroleum reserves, near-zero fertilizer stockpiles, an almost total LNG dependence on the now-disrupted Qatari corridor, and a remittance base centered in the conflict zone. The government’s emergency austerity measures — fuel price hikes, government shutdowns, school closures, navy escorts for merchant vessels — are buying time. They are not resolving the structural vulnerability.

The Pakistan Navy has launched escort operations for merchant vessels carrying essential cargo. The government has formed a high-level cabinet committee meeting daily to monitor petroleum stocks, foreign exchange exposure, and supply chain disruptions. These are the actions of a government managing a crisis in real time, not a government in control of one.

This article is based on current reporting as of mid-March 2026. The Strait of Hormuz crisis remains active, and conditions are changing rapidly.

Comments

No comments yet. Be the first to join the discussion!