Pakistan is ready to see a drop in fuel price, but it may never return to its old level

Media reports suggest a Rs 20 drop this week, here is a breakdown of the price drop and when Pakistanis can see a bigger relief

As soon as news of the United States-Iran agreement reached global markets, oil prices fell sharply. Brent crude dropped 4.76% to $83.17 a barrel, while West Texas Intermediate fell 4.87% to $80.75. Two days later, another wave of selling pushed Brent down 5.1% to $78.96 and West Texas Intermediate down 5.8% to $76.05, their lowest levels since early March.

And for Pakistani consumers, this market reaction raised an immediate question. When will the fall appear at petrol stations?

Media reports started emerging, suggesting that petrol prices could decline by around Rs20 per litre and diesel by as much as Rs35. This was based on a release of ex-refinery price at Rs 225 for MS petrol, falling from Rs 245.

But this is an important time to read how this shift will be seen in the Pakistani market, immediately and in the medium term of 2 to 3 months.

As most of the readers know, the size and timing of any reduction cannot be read directly from the fall in Brent or West Texas Intermediate, that is because on previous occasions Pakistan hasn’t exactly realised the actual gain from these indices . To understand why, one must first understand how Pakistan prices its fuel.

Fuel Pricing in Pakistan

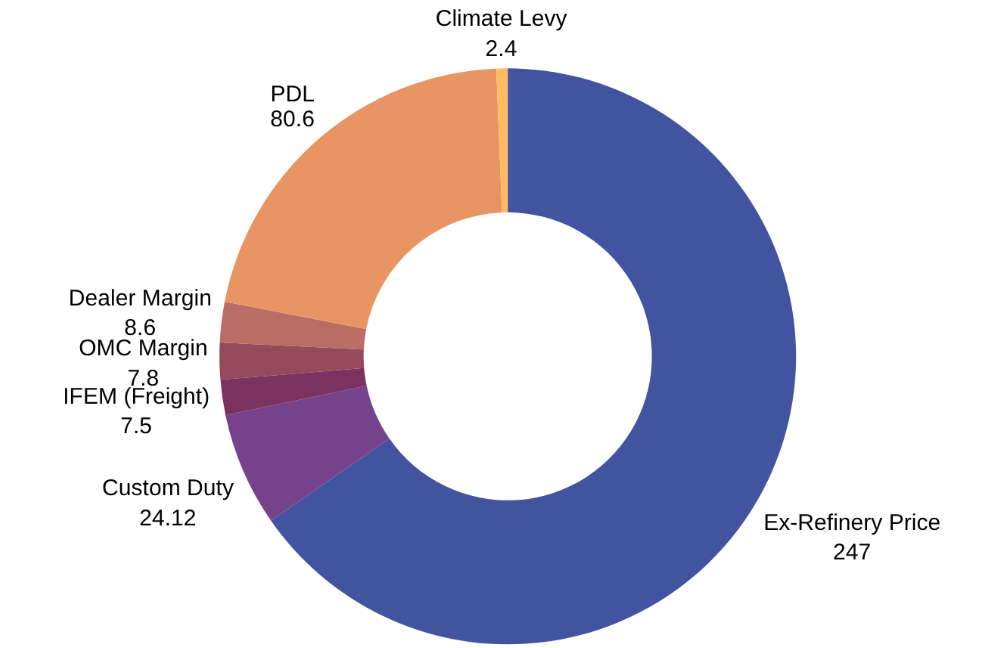

The government sets the retail, or ex-depot, prices of motor spirit (Petrol) and high-speed diesel (HSD).

The retail price begins with this ex-refinery value. It then absorbs the Inland Freight Equalisation Margin, oil marketing company margin, dealer commission, the Petroleum Development Levy and any applicable taxes or charges. Following is a complete breakdown of the current fuel price.

As can be seen, most things apart from the ex-refinery price depend upon local policy making. So the international component of this price is reflected mostly through the ex-refinery price. The amount at which locally produced fuel is valued before freight, margins, levies and other charges are added.

More importantly, the international benchmark used in this calculation is not simply Brent or West Texas Intermediate. While those are important crude-oil benchmarks. Pakistan’s pricing mechanism relies more closely on Arab Gulf assessments for refined petroleum products published by Platts, part of S&P Global Commodity Insights. The distinction is however important because crude oil and finished petrol do not always move by the same percentage or at the same speed.

This was reflected when during the conflict, Platts itself had to suspend parts of its normal bid-and-offer assessment process for Gulf petroleum products, because shipping through the Strait of Hormuz had become too dangerous and irregular. So even when crude prices began falling, the market for physically available petrol and diesel remained distorted.

The premium on war

The ex-refinery formula also includes an import premium. This is the additional amount buyers (refineries) must pay above the benchmark price to secure a physical cargo and bring it into the country.

In normal conditions, the premium used in Pakistan’s pricing mechanism has been capped at around $15 per barrel. At the height of the war, however, the premium reportedly approached $35 per barrel, as PSO got their last shipment.

That increase happened because during a war, tanker shortages, war-risk insurance, security threats, scarce cargoes, financing costs and uncertainty over passage through the Strait of Hormuz all made each available barrel more expensive to transport. Across international markets, buyers paid premiums exceeding $30 per barrel for some replacement crude grades as refiners scrambled for supply.

The premium tells it how difficult that product is to obtain. During a war, the second number can become almost as important as the first.

Why the fall does not fully reach consumers

The media report cited earlier states that documents placed the ex-refinery price of petrol at around Rs225 per litre as of June 15, implying a reduction of roughly Rs 20, a decrease of almost 5%. Meanwhile international indices, including the Platts which showed resistance earlier, over multiple trading sessions, have now dropped over 10%.

At first glance, the fuel price drop of Pakistan may appear smaller than the fall in international crude prices. But Pakistan’s price does not reset every time Brent loses 5% in a trading session.

The government formula encapsulates the average value of crude oil over the relevant pricing period, rather than a single day’s closing price. Usually this is for a 30 day average but in the current times of high volatility, it was reduced to a 15 days period.

Only a few days of lower Platts assessments had entered the calculation by that point. The average for the period still carried the much higher prices recorded before the agreement. A sharp fall at the end of the pricing window can therefore produce only a partial domestic reduction. If lower prices persist and the drop continues, the next review may capture a larger decline.

The import premium also remains elevated. If the reported Rs225 ex-refinery price still contains a premium above $30 per barrel, a second round of relief could come when that premium begins moving back towards its normal level.

The arithmetic is significant. At an exchange rate of roughly Rs279 to the dollar, every $10-per-barrel decline in the import premium is equivalent to approximately Rs17 per litre before other pricing adjustments.

$10 × Rs279 ÷ 159 litres = approximately Rs17.5 per litre

A fall in the premium from $30 to $15 could therefore remove more than Rs26 per litre from the landed cost, assuming the exchange rate and other components remain unchanged.

Is the Strait of Hormuz really open?

So the real question is, when will the premium be reduced? The premium will not return to normal merely because a permanent ceasefire has been announced. The Strait of Hormuz must first become predictably safe for commercial shipping.

That means clearing maritime mines, restoring navigational security, persuading insurers to reduce war-risk charges, clearing the backlog of stranded vessels and restarting damaged or suspended oil and refining infrastructure. Pakistan is particularly exposed because as much as 90% of its oil and liquefied natural gas imports normally pass through the Strait.

Even optimistic recovery estimates are measured in months rather than days. Reuters reported that Gulf refineries could require 40 to 60 days to recover most of their capacity, while broader Middle Eastern oil output may take three months to reach 70% of its former level and six months to reach 90%.

Until ships can move regularly and safely, suppliers will continue charging for the risk that the peace agreement may fail. Platts prices have fallen, but they have not yet returned to the levels that would prevail under completely normal Gulf trade. The conditional reopening of Hormuz has removed the worst-case scenario; it has not removed the cost of uncertainty.

The budget has put a floor under petrol prices

Even if international prices and import premiums continue falling, Pakistan’s new federal budget creates another obstacle to a full return to earlier petrol prices, a higher the Petroleum Development Levy.

The government has projected levy collections of Rs1.727 trillion for FY27, up 17.6% from the Rs1.468 trillion target for the outgoing year. Spread evenly across the year, the new target requires average monthly collections of about Rs143.9 billion:

Rs1.727 trillion ÷ 12 = Rs143.9 billion per month.

The previous target required around Rs122.3 billion per month:

Rs1.468 trillion ÷ 12 = Rs122.3 billion per month.

Unless fuel consumption rises substantially, the government will have to maintain higher levy rates, or keep them elevated for longer, to collect the additional Rs21.6 billion required every month.

The implications are visible in the current price structure. At the reported ex-refinery price of Rs225 per litre, adding a petroleum levy of around Rs80 already produces a subtotal of Rs305, before inland freight, oil marketing company margins and dealer commissions are included.

That makes a retail price below Rs300 impossible at the present ex-refinery level. Even to return to the earlier price of around Rs260, the ex-refinery component would have to fall below Rs180 per litre if every other cost except the levy were assumed to be zero. Since freight and commercial margins cannot actually be zero, the required ex-refinery price would have to fall further.

This does not create a single mechanical threshold at which Brent must fall below $70. Pakistan prices refined products, not crude alone, and the outcome will also depend on the rupee, Platts assessments and the import premium. But if the premium remains elevated and the levy stays near Rs80, a return to petrol around Rs260 would require a far deeper international correction than the one seen so far.

The ceasefire has removed part of the war premium from global screens. It has not yet removed it from the cargoes Pakistan buys, the formula the government uses, or the revenue target embedded in the new budget. The first price cut may arrive quickly. The larger relief will depend on whether peace survives long enough to reach the tanker, the refinery and, eventually, the pump.

The author is a Business and Finance journalist at Profit and can be reached via email at [email protected] and via twitter @shahnawaz_ali1

View all articles →Comments

No comments yet. Be the first to join the discussion!