March 16, 2026

Why the Packages’ bid to buy AkzoNobel fell through, and what comes next

AkzoNobel is exiting Pakistan as a once proud business that finds itself in the doldrums. Despite the many business problems, there is still a lot that the paint manufacturer can offer a potential buyer

March 16, 2026

Syed Hyder Ali, the head of the Packages Group and the heir to Syed Babar Ali, wanted to buy AkzoNobel Pakistan. Multiple sources told Profit he was advised against it from the outset. A number of senior leaders and advisors of the Packages Group had expressed apprehensions regarding the acquisition, saying it was not a good fit for the group.

It did not matter. In October 2025, IGI Holdings, the investment arm of the Packages Group and Syed Babar Ali family, informed the stock exchange that its subsidiary, IGI Investments, had approved the acquisition pending due diligence. An initial figure for the sale was also discussed privately between the two parties. Packages and AkzoNobel naturally declined to comment on what this figure was considering the deal has still not reached an official conclusion. However, a senior executive of a different paint manufacturing company told Profit the figure circulating in the industry was Rs16 billion — including all of AkzoNobel’s real estate assets.

Nearly six months later that deal is on the verge of falling through. The initial amount discussed, it seems, did not stand up to the scrutiny of the due diligence team, and the Packages Group revised the offer downwards by as much as 40%. Since then, there has been complete silence from the parties involved. No official statement has been made by either company or notification given to the PSX, which means a time-of-death has not officially been called. Profit reached out to Syed Hyder Ali, other representatives of the Packages Group, their communications team and other office bearers. After some back and forth it was clarified that they did not intend to comment on the matter.

For AkzoNobel, this marks another moment of crisis and reflection in a decade where they have faced set back after set back. The Dutch paint manufacturer has been reconsidering its position in Pakistan since at least 2020, when it delisted from the Pakistan Stock Exchange (PSX). While AkzoNobel’s financial performance was publicly available so long as it was traded on the stock exchange, there has been radio silence in terms of how it has performed in the years since. Profit gained access to AkzoNobel’s accounts after it was delisted, and the highlight numbers do not paint a pretty picture. It is a story of margins tanking, volumes in tailspin, and a shrinking market share: essentially nothing to inspire confidence in a potential buyer.

But that does not mean the company has nothing to offer. It is, for starters, one of the most historic companies in Pakistan. What is today AkzoNobel Pakistan was once the consumer facing division of the grand old British era Imperial Chemical Company (ICI). For the Indian subcontinent, the ICI name represented the heights of colonial corporate ambition. It was, for much of its history, the largest manufacturer in Britain. It was formed in 1926 as the result of the merger of four of Britain's leading chemical companies — the very same year that Syed Babar Ali was born. At the time, Syed Babar Ali’s father, Syed Maratib Ali, was an up and coming businessman who was a top contractor of the British Indian Army. For his grandson to one day buy what was once the Empire’s Corporate Jewel would mark a magnificent moment in the storied history of both the family and Pakistan’s corporate history.

That taste for legacy and the prestige of the ICI name still exists in Pakistan. Consider this: AkzoNobel’s entry into Pakistan had been because the Dutch company had acquired ICI Global in 2008 and the Pakistan business came as part of the package along with ICI’s presence in the rest of the world. Since AkzoNobel was a paint company and ICI had many other lines of business, Akzo decided to divide ICI and sell some parts of it.

In 2009 AkzoNobel sold the Pure Terephthalic Acid (PTA) business and the associated facility at Port Qasim, the only one of its kind, to South Korea’s Lotte Chemicals. Last year Lotte Pakistan was purchased by AsiaPak Investments, the company operated by Shaheryar Chishty, who also owns K-Electric, Daewoo Pakistan, and has interests in Thar Coal.

Read more: Who is buying Lotte Chemicals?

Similarly, ICI’s chemical business was sold in 2012 to the Yunus Brothers Group, owned by the Tabba family. The family’s biggest asset historically has been Lucky Cement. The Yunus Brothers Group bought a 75% share in the business for $152 million at a premium of nearly 30%, showing how coveted the business was. The Yunus Brothers Group decided to retain the name “ICI Pakistan” for the business they had bought.

But who will buy this last vestige of what was once ICI now? IGI Investments is not officially out of the running for AkzoNobel, but with the sale on the verge of collapse, a few contenders might emerge. There is the possibility of another paint manufacturer entering the fray to try and expand their footprint and acquire a well known brand. Then there are other investors who are also interested and starting to do their homework.

The ICI name and in particular its flagship paint brand Dulux still hold value in Pakistan. Of course a brand name and the power of legacy is not the only thing that makes buyers interested. Another significant feature that will be attractive for potential buyers is the prime real estate property owned by AkzoNobel on Lahore’s Ferozpur Road right outside Model Town. At the end of the day it will come down to the numbers. A buyer might consider the possibility that even if the paint business is a dead end, the property that comes as part of AkzoNobel might be able to turn the profit. But the question remains: could this be a case of flogging a dead horse?

The once mighty ICI

Perhaps nothing paints a better picture of the state of AkzoNobel Pakistan than a brief comparison with AkzoNobel India. At the time of partition, ICI was split between ICI India and ICI Pakistan. The Pakistani side of the border had the soda ash and chemical business while India inherited the paint business including the famous Dulux brand.

However, ICI Pakistan acquired Fuller Paints in 1960 and began manufacturing Dulux in Pakistan as well and ICI Pakistan was as much a paint company as it was a chemicals or soda ash company.

When AkzoNobel acquired ICI in 2008, they entered both the Indian and Pakistani market. In 2024 AkzoNobel International decided to restructure its corporate structure in 2024 in order to focus and make the business more efficient. In line with this, it decided to sell off its businesses in both India and Pakistan.

The Indian company sold quickly.

JSW Paints bought 74.76% of AkzoNobel India for a deal valued at €1.4 billion in June 2025. This is being called one of the largest transactions ever in the Indian paint industry. Up until December 2025, 60.76% of the stake had been bought from AkzoNobel N.V., AkzoNobel Coatings International B.V. and Imperial Chemicals Industries Limited. Based on the value of the transaction, the per share value of the agreement comes to around ₹2,762.05 per share. This gives an EBITDA multiple of around 25 times.

The high valuation that was given was based on the fact that AkzoNobel India showed revenues of ₹40.9 billion (Rs123 billion) with net profit of ₹4.3 billion (Rs13 billion) for the year 2025 before the sale was carried out. In terms of growth, the company was seeing more than 3% growth per year and profits were also increasing. With a net margin of more than 10% being maintained, the company was also giving out healthy dividends.

The acquisition will make JSW the fourth largest paint company in the region, competing with the likes of Asian Paints, Berger Paints and Kansai Nerolac.

The story in Pakistan is strikingly different. Not only did the Pakistani AkzoNobel not reach the heights of its Indian counterpart, the overall paint industry remains difficult to track. While companies like AkzoNobel do have a market share, a host of smaller and undocumented paint manufacturers control a big chunk of a market that operates in the shadows. Due to the high amount of competition, the gross margin for the industry averages at 21% and net margin stands at 3% compared to India’s 10%.

Peaking under the hood

But what made AkzoNobel in Pakistan lag so far behind its Indian counterpart? There was a time, at least in the beginning, where AkzoNobel was thriving in Pakistan. It was once considered the peak in the corporate world of Lahore with Management Trainee Officer (MTO) candidates enrolling to become part of the company. When the company used to visit the campuses, students would line up and sit through the grueling interviews just to have a shot at the coveted seat.

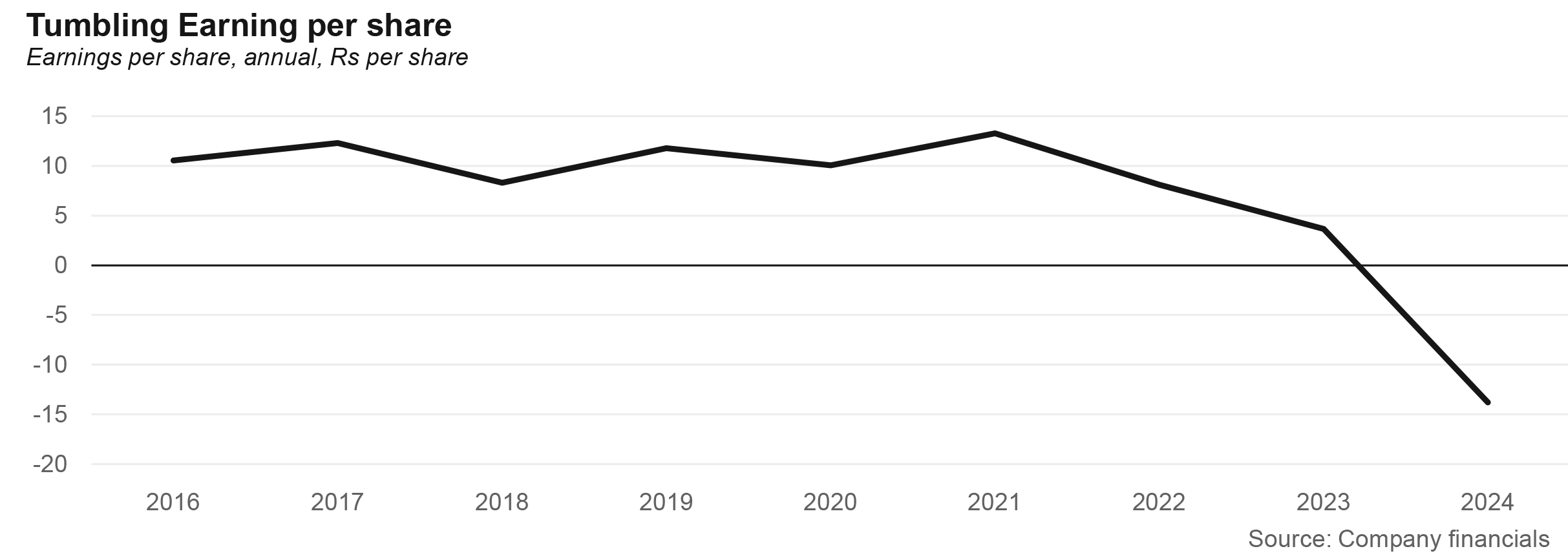

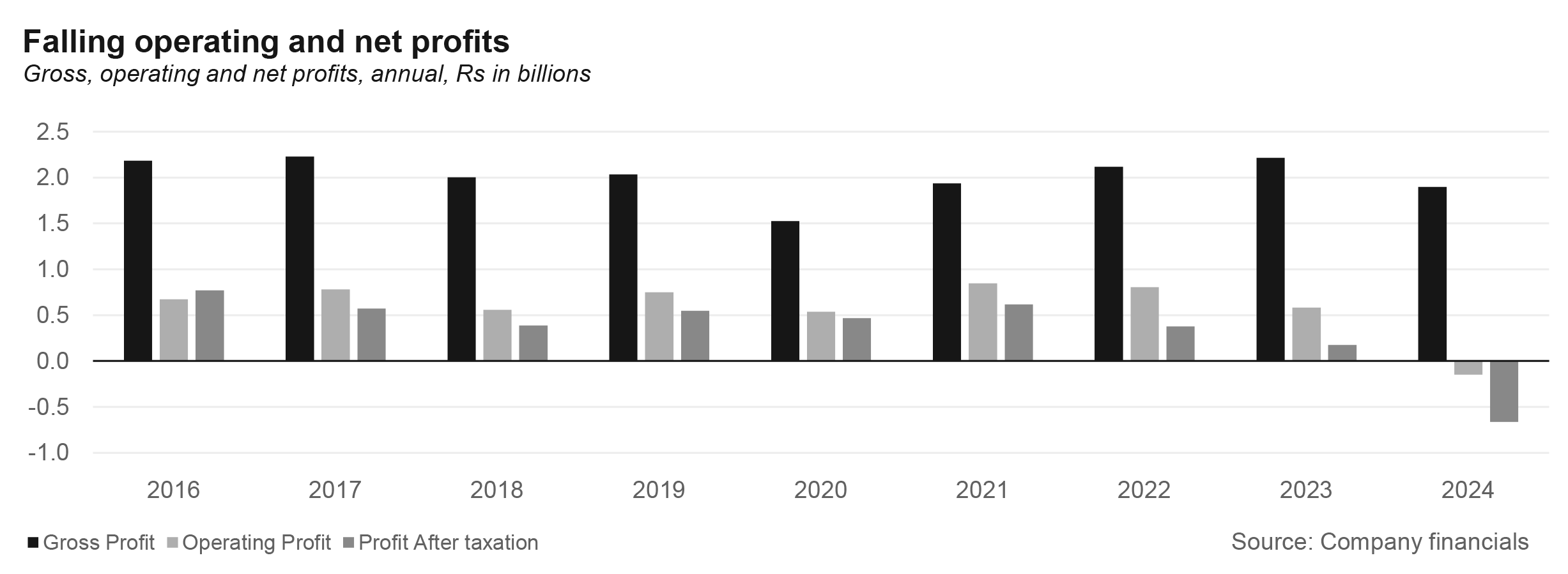

In 2016, AkzoNobel Pakistan was able to earn net revenues of Rs5.1 billion leading to gross profit of Rs2.1 billion and net profit of Rs77 crores. This translated to an earning per share of Rs10.57 as the company saw gross margins of 42%, and operating margins of 13%. These numbers are similar to the ones observed in India.

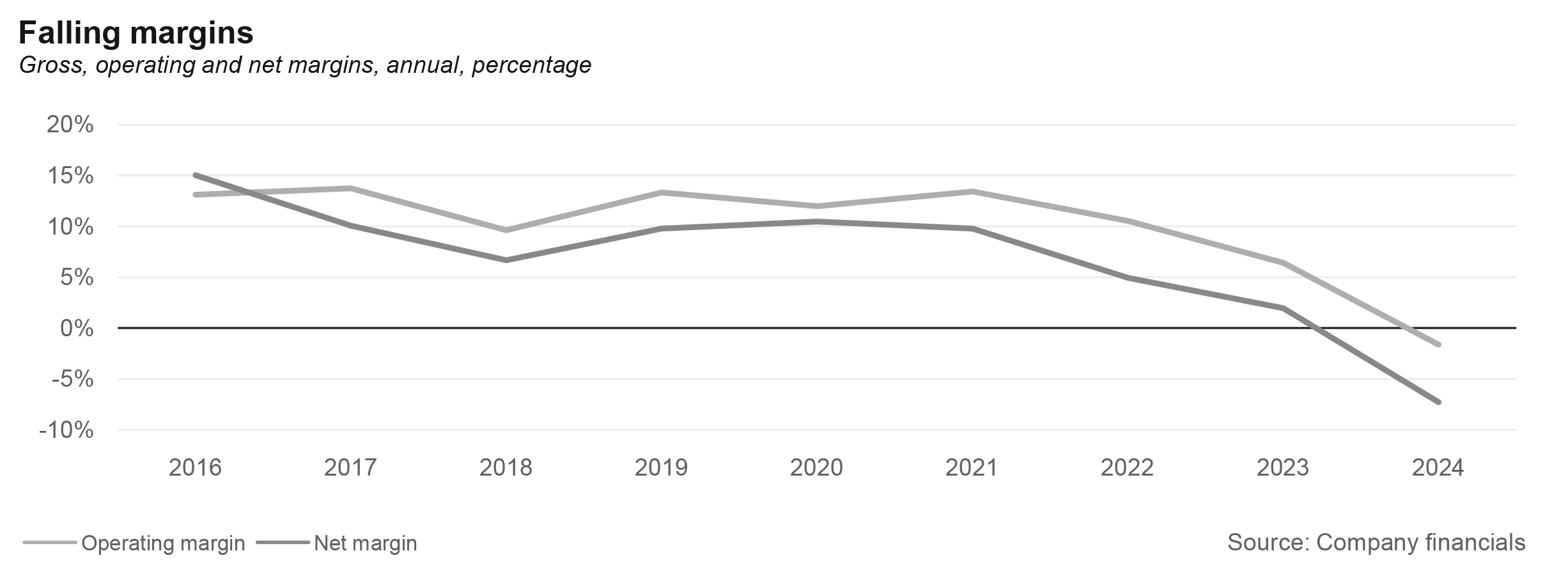

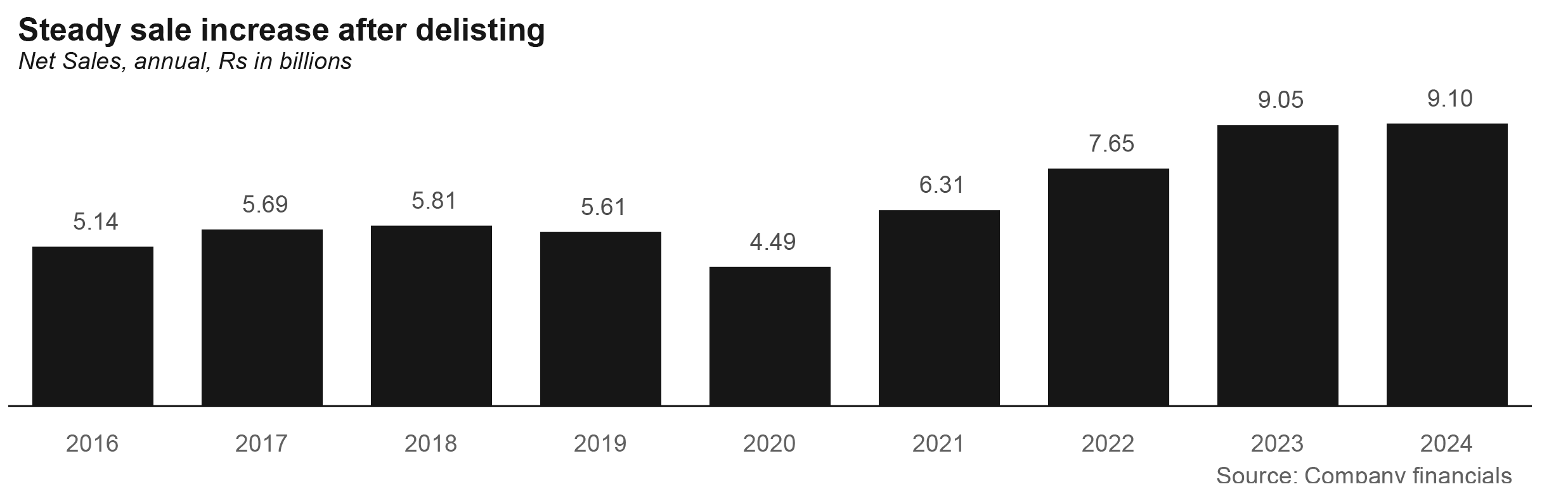

Then things got messy. So messy that all the paint in the world could not white wash the changing nature of Pakistan’s paint market. From 2016 to 2020, sales fluctuated between Rs4.5 billion to Rs5.8 billion. The concerning part for the company was that regardless of sales increasing, the gross profit margin consistently shrank from 42.5% in 2016 to 34% in 2020. This was mirrored by operating margins which decreased from 13% to 12% and net margin which went from 15% to 10.5% in 2020.

This was around the time when Pakistan was experiencing a construction boom. The worst of the after effects of the post-Musharraf economic crisis had passed and new life was breathed into the economy. Interest rates were low and so were fuel prices off the back of international stability. To cater to a lot of this demand, a number of smaller, informal paint manufacturers began to emerge in Pakistan.

This informal sector moved fast, it grew in bursts in smaller areas, and it competed hard on prices. For starters, these local players were not bound to international quality standards. They used their own mix of chemicals which do not follow the strict code of ingredients required for manufacturing. This also made them immune to any changes in the prices of the inputs being imported by the international companies and to any weakening of the rupee. Because the sector is so vastly unregulated, it did not matter that their paint often did not meet safety standards let alone quality standards.

These companies also established direct relationships with small distributors. While AkzoNobel might have had the suited and booted MBAs working on strategy, the owners of these smaller companies were spending time at these distribution points themselves. It is also difficult to overstate the role that the “token” system played in this. As Profit has covered in earlier stories, paint manufacturers began placing tokens worth a certain amount of money in paint boxes. Because of cheap labour in Pakistan, painters often buy material themselves and add it to the cost of a paint job. These painters could redeem the tokens inside for money and thus began buying the brands that would give them the biggest tokens. Essentially, these companies were offering painters a bribe to work with their paint. By some estimates, the informal sector has grown to have 64% of the market share, while AkzoNobel and other international brands have the remaining third of the market share.

The token system has been covered by Profit in the past as well.

Read more: Business vs Ethics: The colours of corruption

According to Farooq Amin Sufi of Master Paints, AkzoNobel suffered especially hard from the token system because they did not go all in. “Dulux used to be the only paint company other than Master Paints that did not use tokens, but then around a decade or so ago they also started putting tokens in their paint,” he explains. “The problem was they did not match their tokens to the local companies. Then there came a time when their volumes suffered immensely.”

He went on to explain that AkzoNobel started using tokens until the MNC’s international bosses put an end to the practice. “When they reviewed the accounts of AkzoNobel Pakistan they saw a massive expense under marketing for the tokens and told the Pakistan office to stop doing it. When the next quarterly result came there were serious losses, and when the international headquarters asked the local company said this was the nature of the Pakistani market — and they are right it is. We suffer losses because of it as well.”

Master Paints claims they are the only company that has never compromised on tokens. However, as a result they have branded their paint as the “no token” variety and have used this distinction heavily in their marketing campaigns and focused on making customers more aware. Because AkzoNobel first placed tokens, did not compete on token value with local companies, and then also removed them they still had that taint. All of these bad decisions compounded.

Companies like AkzoNobel and Master were not able to compete on price. Not only were their inputs more expensive, being in the documented sector meant they had to pay taxes while their new competitors could skate them away. Their response was to push themselves as a quality product, which required further investment and more imported pigments and other inputs. This naturally increased their costs and their margins narrowed.

Read more: Why Syed Babar Ali should not buy Akzo Nobel

This was perhaps one of the factors that led to AkzoNobel delisting from the PSX in 2020. Since then, details of the company’s performance remained under wraps. The company attempted to continue expanding, even inaugurating a major production facility in Faisalabad worth more than Rs7.5 billion in 2024. The new site would be used to produce decorative paints for automotives, specialty and protective coatings.

“Our investment in this greenfield site reaffirms our commitment to grow in Pakistan. It will fuel our ambition to diversify with sustainable innovations and enter new segments in the domestic market, while also providing new opportunities to delight customers beyond Pakistan,” stated Mubbasher Omar, CEO of AkzoNobel Pakistan Limited speaking to the media at the inauguration of the new plant.

But then came AkzoNobel International’s decision to restructure the corporate sector. Before AkzoNobel had the chance to make this new facility work it was up for sale. Unlike in India, however, this was coming at a time when the Pakistani company was in the doldrums. AkzoNobel’s financial statements since 2020, analysed by Profit, show the problem of shrinking margin had only grown.

While the company recorded more sales, reaching Rs6.3 billion in 2021, then Rs7.7 billion in 2022, Rs 9 billion in 2023, and Rs9.1 billion in 2024, this was mainly the effect of inflation.

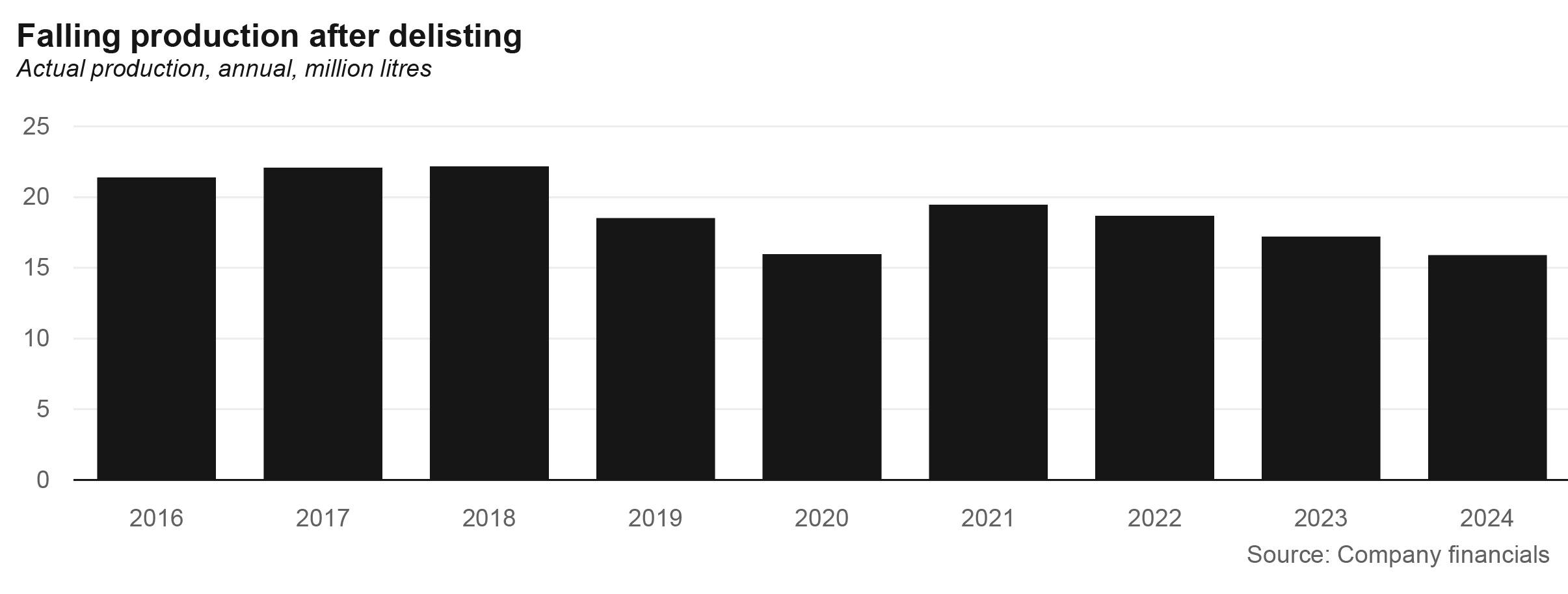

Gross margin fell from 34% in 2020 to 20.9% in 2024. The operating margin shrank from 12% to -16% and net margins fell from 10.5% to -7.3%. While the exact volume data of sales is not given, the annual production of the company can be used which showed that the company produced 21 million litres of paint in 2016 which reached 18.5 million litres by the end of 2019. The production for 2020 can be considered an outlier due to the pandemic taking place where actual production was only 16 million litres. After the recovery was seen in 2021 with production reaching 19.5 million litres being produced, Akzo has seen production fall to 16 million litres of paint being manufactured in 2024 as people (and more importantly the painters) increasingly preferred cheaper local alternatives.

The gross profit earned by the company was only Rs1.9 billion and the company actually made an operating and net loss of Rs15 crore and Rs66 crores respectively. The situation was so bad that the loss per share made by the company was Rs-13.77 per share for 2024.

The effects were not limited to the company’s financial statements. Once the darling of MBAs and young grads from Lahore, their offices today paint a gloomy picture. Their MTO programme is unable to compete with other MNCs and they pay their trainees around Rs90,000 a month. Cost cutting is the name of the day. It is a vicious cycle that many companies go through. A crisis forces the management to cut costs and they immediately go for the jugular: the workforce. Talented workers leave, their positions are either not filled or multiple roles are given to a single person, and less competent workers replace them. The organisation’s collective brainpower and ability to solve problems goes down dramatically.

And all this while with every passing year production was becoming costlier and less profitable over time. With the added pressures of no profit repatriation to the foreign owners and import controls being placed by the government, the best solution for AkzoNobel N.V. was to sell its subsidiary.

Why buy AkzoNobel?

As a paint manufacturer, AkzoNobel Pakistan is in the dumps. With gross margins this low it was impossible to stay in the race let alone thrive. But for anyone potentially looking to buy the company there will be two things that might justify the price: legacy and assets.

AkzoNobel, ICI, and Dulux are all well recognised brand names in Pakistan. For those that do not remember the heights of ICI, it is difficult to imagine what it must feel like to the business leaders of today who came up in their careers idolising this grand old company. Not only is there a premium to be paid for the ICI legacy, anyone looking to enter the paint business would do well to have established brand names on their side.

The most obvious candidate to buy AkzoNobel would be a local paint manufacturer. In India as well, AkzoNobel was bought by JSW, a local paint manufacturer that has become one of the largest players in the region after the acquisition. Local paint companies in Pakistan have managed to do well, however it seems the idea of purchasing AkzoNobel is not well thought of within the paint industry. According to one senior executive of the paint industry, the asking price is far too high. “Our company at least cannot manage such a big purchase. Also frankly , it is not worth the headache,” they said.

Similarly Farooq Amin Sufi of Master Paints says it is a proposition that they had received before but it was too expensive. “Back in the day some ex employees of AkzoNobel did approach our family and asked if we were interested in buying them. The offer was made many times actually,” he says. “Recently when it came on the market it was open for everyone but we thought it was overvalued. They have also been facing a lot of problems which is why we were not particularly interested.”

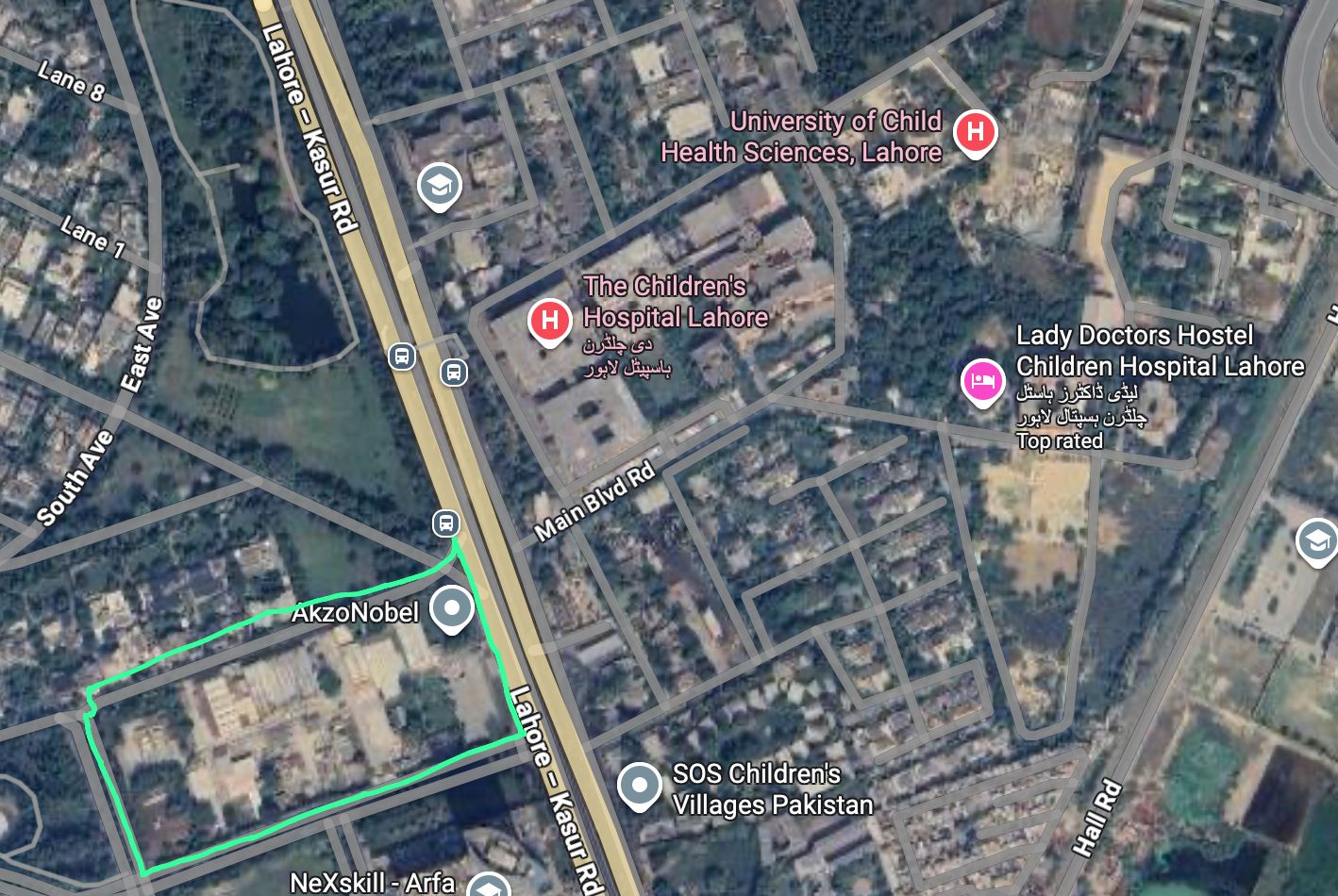

Why, then, would anyone want to buy AkzoNobel? Perhaps the most attractive factor is land. AkzoNobel has a large facility spread over 88 kanals (11 acres) at 346 Ferozpur Road Lahore. The facility sits on one of the most lucrative intersections in Lahore. Its front faces out onto main Ferozpur Road right at a terminal of the Metro Bus Station. It sits on a corner with its other side sitting in the middle of Model Town, one of the most expensive areas in the city. On top of that its main gate is a 30 second drive away from the Gulab Devi Hospital U-turn which leads directly to Walton, Cantt, DHA, and recently CBD’s route 49. In 2019, when AkzoNobel was preparing to delist from the PSX, that property was reevaluated and its forced sale land value was estimated close to Rs2.6 billion. This does not include the cost of the building. Since 2020, the property’s value is bound to have gone up, particularly because of continuous development work in the area and in particular on this patch of Ferozpur Road.

AkzoNobel Pakistan’s main asset is an 88-Kanal facility in one of the most prime real estate locations in Lahore.

According to one source, buyers are not just interested in the paint business but also in the potential of this property. While they might want to give running the paint business a fair shot, even if it does not work out, the prime property can be managed or converted into a commercial real estate project.

As far as IGI Investments acquiring AkzoNobel is concerned, the matter is unlikely to come to fruition. That is despite the fact that the owners of the group were quite keen on buying AkzoNobel. In fact, even after the low offer made after the due diligence exercise, a revised upward bid was also made in consequence of the talks stalling, however, even the revised deal is too low for AkzoNobel to be accepted. Within the Packages Group, one source felt that the resistance from the management group was enough that they conducted the due diligence in a very strict manner and stuck closer to the lower edges of the valuation.

Profit reached out to the management of the Packages Group and IGI Holdings to seek insights into the matter but they stated they did not want to comment.

Profit reached out to the representatives at AkzoNobel N.V. multiple times in regards to the credibility of the deal falling through. Joost Ruempol, head of reputation management at AkzoNobel N.V. stated that “We do not comment on market rumors.” Similarly, officials at AkzoNobel Pakistan were also contacted to verify or reject these reports, however, no reply was received till the filing of the story.

There are also reports that the deal that was being negotiated was stipulated on the fact that AkzoNobel could not pursue any other active bidders while IGI was contemplating the deal. This was done so an active bidding war did not start while the due diligence was being carried out. The deadline for the deal was initially given in December 2025 which was extended to February 2026. With that date elapsing, AkzoNobel is now free to find new bidders.

One might imagine there to be a vague possibility that Lucky Core Industries and Asia Pak Investments, the two companies that currently own the other two parts of what was once ICI Pakistan, might be interested in this last link. However, Muhammad Ali Tabba of the Lucky Group firmly denied that this idea was even being considered.

Similarly, Profit also reached out to AsiaPak Investments. The private equity firm headed by Shaheryar Chishti has acquired significant positions and control in some of the largest companies operating in Pakistan. The firm also has experience buying a controlling interest of foreign multinationals like Lotte Chemical and Daewoo Bus Service where ownership was handed over by foreign investors to local ones. Their representative said they could not comment on the matter.

The field for purchasing AkzoNobel remains open. While the company has its fair share of problems, its sale will mark a bittersweet moment in Pakistan’s corporate history. On the one hand, it means that what was once ICI, a grand old imperial company, is now entirely in the hands of Pakistanis. But not only has it taken time to get here, it has involved exits and divisions.

There are two words in Urdu that can be used to describe the act of division. The first is taqseem. Of Arabic origin, it is a politer word that indicates a fair distribution of some sort. The other word is of Hindi origin: Batwara. It denotes something far more visceral. It is a violent sundering of something whole, a selfish decimation.

It is perhaps why Pakistani histories of the partition refer to the events as Taqseem-e-Hind, and the language used by the Indian National Congress at the time of partition referred to Jinnah’s plan as Hindustan ka Batwara. It is also why the word batwara continues to be used in a negative connotation in discussions of inheritance.

As Profit has pointed out earlier, the sale of AkzoNobel will determine the fate of what was once ICI. And it will raise the all-important question: was this taqseem or the dreaded batwara?

4 Comments

No comments yet. Be the first to join the discussion!