Ladies and gentlemen, meet PSO; the fintech company and Rs 1.7 billion VC fund

Is the state-owned enterprise doing the right thing by venturing into fintech and the world of venture capital?

In the world of retail, coffee giant Starbucks is considered a bank. Because the mammoth coffee chain operates a digital wallet, which held $1.5 billion in customer cash as of 2022. Starbucks app has as many as 31 million app users. The numbers are staggering! For context, more than 85% of the banks in the US hold less than $1 billion in assets.

What could this possibly achieve for Starbucks? A lot really. Because the $1.5 billion in customer cash solves all the cash flow issues for Starbucks. All the money remains in the Starbucks ecosystem that the coffee retailer can use as a loan without any interest. Customers preload money onto the app, order coffee and pay through the app, without any exchange of cash or card swipes. The funds that remain in the app can be used by Starbucks as working capital as well as to grow operations. This is ingenious and the success of the Starbucks wallet makes it one of the top apps in the world.

There are lessons that can be learnt from this and if you are Pakistan State Oil (PSO), you would definitely want to replicate this. Because the state-owned oil company struggles with serious cash flow issues mainly because of the persistent circular debt problem in the country. The choking of the cash flows means inefficiency of operations and an impact on overall financial performance of the company.

How could it be solved, you might think? The answer to this lies in digitising payments. What if the retail payments at PSO were made through a digital wallet instead of cash, just like in the case of Starbucks? Realistically, that should plug some of the cash flow issues of PSO. At the same time it should also help bridge the pesky cashless world the State Bank keeps telling us about which in turn should mean more customers for PSO. A win-win-win, right?

In its financial statements, PSO revealed they were launching the fintech venture under the name of Cerisma as a long-term corporate strategy. It is also a move that, the company believes, will endear them to shareholders.

But it seems like PSO is not only following the Starbucks model but also taking it a notch above. Because the oil marketing and distribution company is also gunning to secure an Electronic Money Institution (EMI) license under its fintech ambitions. The company has not yet confirmed to Profit if it plans to secure the license in any official communication but we understand that the wheels are already in motion.

It is not only fintech that PSO wants to do. The plans are grander with the company also planning to invest in startups via its venture capital arm, PSO VC Pvt Limited. Since 2021, the company has earmarked as much as Rs1.7 billion for this fund, all from its own pre-tax profits.

What could all of this mean for PSO and are these plans substantial? Before we try to explain this, let's delve into the recent financial woes of PSO.

The financial woes of Pakistan State Oil

PSO has a problem. It is massive, tied to governmental sluggishness, and in a constant liquidity crunch. Allow us to demonstrate in some key statistics.

PSO's national presence spans 3,528 retail outlets, holding a 51% market share, marking a 1.8% growth from the previous year. Notably, in motor gasoline, it maintains a robust market presence with a 44.2% share, selling 3.3 million tons against industry sales of 7.5 million tons. Despite a 29% decline in diesel consumption, PSO increased its market share to 54.4%, hitting 3.4 million tons, a growth of 2.8% from the prior year.

Despite this, PSO faces a critical challenge hindering its strategic plans. This risk stems from the accumulation of long-outstanding circular debt receivables, which reached an amount of Rs 524 billion as of June 30, 2023. These debts include an aggregate amount of Rs. 434 billion due from GENCO Holding Company Limited (GENCO), Hub Power Company Limited (HUBCO), and Sui Northern Gas Pipelines Company Limited (SNGPL) on account of Inter-corporate circular debt. These include past due trade debts of Rs72 billion, Rs18 billion and Rs298 billion from GENCO, HUBCO and SNGPL respectively, based on the agreed credit terms.

As of September 30, the issue of circular debt remained a significant concern with outstanding receivables reaching Rs 511 billion, with SNGPL accounting for 72% of total outstanding receivables amounting to Rs 366 billion of the total receivables.

To cope, PSO had to resort to increasing their short-term borrowings to meet their working capital requirements. Short-term borrowing increased by 2.6 times to Rs 453 billion in fiscal year 2023 as compared to Rs 175 billion in fiscal year 2022. As of September 30, 2023, this figure stood at Rs 392 billion.

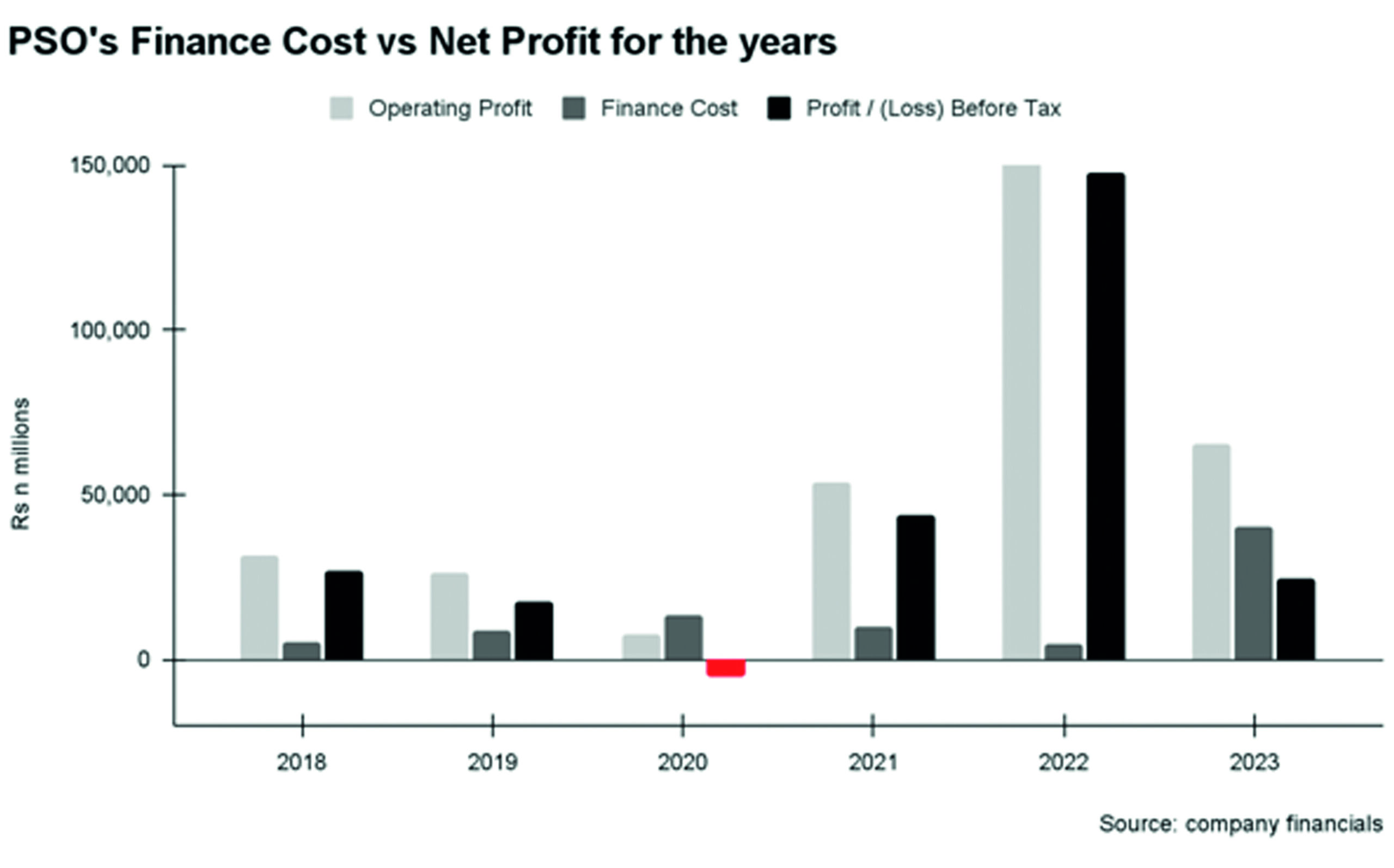

Consequently, there has been a substantial increase in finance costs, which have risen by 114% compared to the same period last year. Moreover, a steep rise in interest rates in the fiscal year 2023, on account of an increase in the policy rate by 825 basis points by the State Bank of Pakistan, resulted in a substantial increase in the company's finance cost and severely impacted its profitability.

Finance cost in the fiscal year 2023 stood at Rs 43 billion as opposed to around Rs 6 billion in fiscal year 2022. This has impacted profitability adversely as nearly 60% of the operating profit has been consumed by finance costs, leading to a net profit of only Rs 5.7 billion.

Despite an increase in market share for oil products to 51%, reduced sales demand for white oil products due to an overall reduction in the industry’s sales volumes also contributed to this increase in the finance cost for the year which reached Rs 40 billion.

Summing up, these long-outstanding receivables are increasing the financial burden and adversely impacting the company's profitability, hindering retained earnings and overall equity.

To mitigate these challenges, PSO is collaborating with the government, actively pursuing solutions to the circular debt issue. Once the circular debt receivables are settled, PSO will be in a better position to realize its strategic plans for expansion, integration, and diversification. And it is also being creative to solve these problems in case the government stays in deep slumber.

Making sense of the PSO fintech

This isn't the first Hurrah, of course.

In 2019, the Pakistan State Oil launched its wallet by the name of DIGICASH. Users can manage the wallet via the PSO Fuellink app and get a virtual as well as a physical DIGICASH card to make purchases at retail fuel stations. These cards can be topped up through a bank, branchless banking agents and at some retail outlets of PSO. This wallet is currently closed loop which means that only PSO customers can use it for purchases from PSO.

What does that achieve? While the customer gets the convenience of not carrying cash, PSO is able to get cash in these wallets that stays with PSO. These top ups could be big and customers could keep them unused for a while. The unused customer cash could be used by PSO as working capital or investment purposes. The impact of wallets has already been in billions of rupees.

In 2019 alone, PSO added 80,000 DIGICASH customers and by the end of 2021, this number had increased to 190,000 DIGICASH users, with Rs5.7 billion in top ups in the wallet. Essentially, this is the concept of deposits at banks. Users deposit their money with the bank, the bank issues them a card and the users use that card to make purchases wherever the card is accepted. But unlike a bank card, a PSO card can not be used anywhere else other than PSO. And unlike banks, PSO can not lend that money out to anyone. Instead, it could use that money to plug any cash flows.

Think of it this way: for the financial year 2023, PSO had sales worth Rs3,605 billion. Even if half of these sales are done through the DIGICASH wallet on which the money is preloaded, PSO has access to that money, which is roughly Rs1,800 billion, before the actual sale which can be used to timely pay stakeholders in the supply chain and ensure smooth operations of its core business. This is the strategy that Starbucks also applied. The potential here for PSO is big because its sales are massive. Remember also that access to such money removes or diminishes the need of going to a bank for financing which can charge high interest rates and ask for securities and collateral. As mentioned above, financing costs are a big pain for PSO.

The big question, however, is why would people use the wallet instead of making purchases on cash, which is (apparently) easier and more prevalent? The answer to this question is loyalty programs. Loyalty programs are incentives provided by businesses in the form of rewards, discounts or any other special inducements to attract customers or retain them. One of the biggest hooks for Starbucks customers to get to use the wallet is a points-based rewards system. On each purchase, customers get points that are equivalent to a certain amount of dollars. When accumulated enough, these points can be used to make purchases at Starbucks.

A similar points-based rewards system is in place for PSO when using the DIGICASH card. Every time you use your DIGICASH card to make a payment for fuel at PSO, you get points worth a certain amount. When accumulated enough, these points could be used for a refuel free of cost as a reward for using DIGICASH.

[caption id="attachment_159494" align="alignleft" width="1695"] PSO's recent campaign to promote usage of DIGICASH cards includes a mega prize giveaway of 1,000 liters of free fuel via a lucky draw. Only DIGICASH users are eligible for this prize upon refuel[/caption]

PSO's recent campaign to promote usage of DIGICASH cards includes a mega prize giveaway of 1,000 liters of free fuel via a lucky draw. Only DIGICASH users are eligible for this prize upon refuel[/caption]

Besides giving PSO a free loan everytime you top up your DIGICASH card, you are also giving PSO access to money that is now moving quickly in the PSO supply chain. According to a source expert in fintech and familiar with operations of PSO, electronic transactions are settled quicker, giving PSO quick access to money.

But what if PSO could also attract deposits like a bank, and use that money to invest in government securities and use those earnings to plug liquidity issues? What if PSO cards could also be used at all the PoS machines in the country and for fuel purchases only? Not only does this help them plug liquidity issues in their core operations but also opens up new revenue lines. This is perhaps why PSO has set up its own fintech company by the name of Cerisma Private Limited which is gunning to get an EMI license. PSO is also rumored to be in the race to secure a digital bank license.

As mentioned earlier, PSO has a mammoth presence with over 3,500 fuel stations. All these stations could have four different types of retail operations: first is the sale of fuel and lubricants; secondly a convenience store; third and fourth are a tyre shop and a service station. Now wouldn’t it be a good deal if you could use your fuel card that your company gave you or a PSO DIGICASH card to pay for all the aforementioned retailers at PSO stations?

This is the broader strategy in place, apparently. Your corporate fuel card or your DIGICASH card could be branded as Visa or MasterCard once PSO gets the EMI license and you could use that for all four of the retail transactions, provided they have PoS machines to accept these cards. Now fuel purchases are a significant expense, perhaps second only to groceries, and a frequent one. If you could use your PSO card to do groceries and other purchases such as buying clothes besides fuel, the PSO card has the potential to become your default debit card.

And PSO has a head start. Unlike other EMIs, PSO already has corporate users of its fuel card and DIGICASH users before it even is an EMI. PSO also has a very strong retail network where these cards could be used. According to an expert in fintech, new EMIs would need at least 2-3 years to build the kind of presence that PSO has now for its EMI.

The EMI operations would also not only help PSO save money from MDR but make it a new revenue line altogether. If you currently have, say, an HBL debit card, and you use it to purchase fuel at PSO, there is a fee that the fuel station owner pays to HBL for the card payment. Part of that fee is borne by PSO. Once PSO has its own cards as an EMI, it saves that fee paid to HBL, and also starts earning that fee (negotiated differently with different types of retailers) for itself when you use the PSO card to purchase, say grocery at Carrefour.

“The PoS transactions at PSO have a huge volume and the company already issues its wallet card. They could have in mind that while a piece from MDR goes to issuers, they could capture a piece of that being an EMI,” said a source in the fintech industry, who is familiar with PSO’s fintech plans.

PSO identifies MDR as a significant issue in its company reports. Late last year, PSO told its dealers that it will no longer be able to foot its share of the MDR bill. According to its arrangement with the dealers, whatever MDR on card payments was negotiated with a bank, the dealer would pay a certain percentage and the oil marketing company, in this case PSO, would pay the rest. But after PSO said that it would no longer pay its share of the MDR, dealers could either continue accepting card payments at their own expense or discontinue accepting cards completely.

The MDR that could be charged by the banks was between 1.5-2%. Later into the year, in a letter to the State Bank Governor, the OMCs asked the central bank to cap the MDR at 0.3% for the oil industry. This would mean that the merchants, fuel stations in this case, would have to pay less from the per liter price for accepting card payments. The rationale provided by OMCs was that since the fuel industry margins are regulated, a percentage charge of 1.5-2% on card payments was a significant hit on their bottom line.

In big cities like Lahore and Karachi, card penetration is high which means volume of sales on cards is high. As more sales are processed on cards against cash, the MDR starts becoming a bigger problem since now most of the sales are subject to the MDR percentage charged by banks, while margins are fixed because they are regulated.

As a consequence of this, PSO dealers either stopped accepting card payments or started passing it onto consumers, hampering PSOs sales on cards, wherever they were high in volume.

According to the company financials, it was able to successfully negotiate a favorable MDR applicable on bank card transactions. “This achievement led to significant annual savings of over Rs300 million, which will continue to benefit the company in the long run.”

Under the EMI license regime, fintech companies are allowed to invest up to 75% of their e-money balance in treasury bills and government securities. This could be of huge benefit to PSO. Since PSO users are big in number and if they switch to PSO cards, this would essentially mean big deposits for EMI. Now unlike a bank, PSO can not use that money to lend to anyone. But it could use the majority of that money to invest in treasury bills and government securities, just like conventional banks. And whatever income PSO earns from that, it could use it as working capital in its core operations, for expansion or for any other investment.

PSOs plans with regards to fintech fall together. Not only does this help the company solve cash issues in its operations, it could also add to PSO’s earnings. But whether PSO would be able to execute this plan efficiently is the big question. Because when contacted, Profit was told that the company does not have anyone who could say for certain what the plans were. This lack of discipline could also compromise PSOs other endeavor, that of launching a venture capital fund.

The PSO Venture Capital. But does it make sense?

Part of PSO’s strategy is also to launch a venture capital fund, from its own profits. “PSO Venture Capital (PVC) has been created as a strategic investment division of PSO, aiming to unlock new streams of revenue and enhance the overall value of the parent company,” a representative from PSO said in a statement to Profit.

“By strategically investing in a wide range of businesses, high-growth companies, start-ups, and cutting-edge technologies, PVC is poised to drive substantial asset growth within the predefined risk boundaries.”

One could wonder though that if PSO has liquidity issues, why would it allocate money from its own profits? The company said in a statement to Profit that for the venture capital fund, it would be contributing up to 1% of its profit before tax in PVC for the purpose.

Adnan Sami Sheikh, assistant president at Pak Kuwait Investment Company (PKIC), says that the scale of the company is big enough that taking out 1% for investment purposes is not going to be an issue for PSO.

“PSO has sales worth trillions of rupees. Even at a pre-tax profits level, a 1% contribution wouldn’t affect PSOs' liquidity much,” Adnan said.

This makes some sense. For the year 2022, PSO’s pre tax profits were close to Rs150 billion. Consequently, the company contributed Rs1.47 billion to its venture capital fund. For the financial year 2023, PSOs profits were Rs 24.3 billion. For that year, the company contributed Rs243 million to the VC. Collectively, that’s over Rs1.7 billion in its VC fund. That’s a hefty amount that wouldn’t affect PSO much as Adnan says but shouldn’t PSO be trying to save every penny?

According to a senior investment analyst familiar with PSO’s operations, who chose to comment anonymously, PSO getting into venture capital as a diversification strategy makes sense because global oil prices have a high volatility which could result in losses. Any diversification for PSO would be helpful for its sustainability.

For PSO, he explained, positive cash flows could be seen in the coming days because of the increase in gas prices by the government in November. “The increase in gas prices would result in a positive GDS of Rs57 billion. Fixed charges have also been increased from Rs10 per month to Rs400 for protected consumers and from Rs460 to Rs1,000 for unprotected consumers which would have an impact of approximately Rs80 billion.”

“This would help the government pay for the tariff differential caused by RLNG sales to consumers instead of industries. PSO being an RLNG importer would receive this money which would help it achieve positive cash flows,” he explained.

Regardless of PSO being able to take out money to invest without affecting cash flows or not, the big hazard here is that the company plans to invest in ventures that are extremely high risk but come with very high gains as well. VC investments are a game of patience. A fund has to keep on investing, anticipating that out of multiple investments it made, one or two could give them gains so big that they would offset any losses on the other investments. But these gains come after a few years. So PSO upsetting its cash flows to invest in very risky ventures could turn out to be a double edged sword. This kind of a risky endeavor can be undertaken by Saudi ARAMCO and the likes that have a very stable financial position and invest in startups for the sake of innovation, without worrying about cash flows or gains. In fact Saudi ARAMCO has a $500 million fund called Wa’ed Ventures to invest in startups.

“If PSO is planning to replicate ARAMCO, know that people at ARAMCO are seasoned professionals and do everything with precision. I don’t expect the same from PSO,” said a prominent Pakistani venture capitalist.

This is one more hazard of PSO’s VC ambitions. That venture capital investments require a certain type of expertise and discipline. Being a government owned and controlled entity, that discipline is likely not there. Because although there has been a lapse of two years since PSO started contributing money to the VC fund, no investments have been made by the company yet. In fact the company has not been able to secure a license from the Securities and Exchange Commission of Pakistan (SECP) to undertake this endeavor, and doesn’t even have a team yet to look after these investments.

On the other hand, folks at the SECP were amused and struggled to comprehend that a government-owned entity like PSO was launching its own venture capital fund. They haven’t yet been able to confirm the status of PSOs VC license.

According to an expert, PSO would likely be better off if it partners with a local fund to make such investments and does not do it on its own. That is to say that whatever allocations PSO has for its VC fund, it should give that money to a local VC fund and let them decide where to invest. This would not only cover the discipline but also the expertise issue. Or being a government entity itself, PSO should contribute its money to the $10 million fund that the Government of Pakistan also plans to launch.

This article was updated on December 26, 2023

The author is a staff member and can be reached at [email protected]

View all articles →75 Comments

No comments yet. Be the first to join the discussion!