Atif Mian’s advice for the State Bank: explained

Pakistani-American economist and Princeton University Professor Atif Mian took to Twitter on Monday, January 20, in effect, critiquing the way central banking functions in Pakistan.

His main gripe though, was with what some analysts and commentators in Pakistan have been celebrating: the recent record foreign investment of $2.25 billion in treasury bills during the current fiscal year. Those inflows are what have helped the State Bank of Pakistan (SBP) push reserves up to cross $11.6 billion. The total reserves in Pakistan are now at $18.1 billion.

Yet Atif says that, in fact, there is little benefit of such inflows in the case of Pakistan, and that such inflows will create potential risk. How did he reach his conclusion? Profit takes a look.

What is the role of a central bank?

According to Atif, “For central banks to be effective, they must first work on establishing two pre-conditions: (i) flexible exchange rate management, (ii) macro-prudential and capital control regulation.”

Mian based this understanding of what a central bank is on “Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence”, a paper by French economist Helene Ray.

According to this understanding, Mian says: the exchange rate needs to reflect market reality. If the productivity growth is lower than competing countries, the exchange rate has to depreciate.

So far, so good: Pakistan has learnt the hard way that a fixed exchange rate does little for growth, and most agree that the new market-based exchange rate, also advocated by the International Monetary Fund (IMF), is a step in the right direction of a responsible, and more realistic, economy.

But what is a little more interesting is the second part on regulatory measures at the SBP’s disposal. Traditionally, central banks have often focussed on the financial soundness of individual financial institutions, like commercial banks. This approach is known as micro-prudential policy. But after the global financial crisis of 2009, this approach was considered too narrow in its scope, and macroprudential policies were introduced, or more holistic regulatory approaches to the economy. These policies are designed to reduce systemic risk in a system.

Examples of organizations dedicated to macroprudential policy include the Financial Stability Oversight Committee in the United States (formed in 2010 and overseen by the US Treasury), and the European Systemic Risk Board (also formed in 2010, and overseen by the European Central Bank).

Meanwhile capital controls refers to a set of measures that a government can use to control flows from capital markets to and from a country’s capital account. Capital controls used to be popular measures until the 1970s, when more free market economists began to persuade governments to abandon capital controls. But recent financial crises have once again made countries, particularly emerging markets partial towards capital controls.

So why is Atif advocating such a strong regulatory approach? His next tweet expands upon his attitude towards free capital flows: that the “benefits of free global capital flows have proven to be elusive or illusive.”

According to Atif, unregulated capital inflow can build dangerous external liabilities that whiplash the economy, and severely constrain the central bank.

To make his point about ‘elusive capital flows’ more forcefully, Atif cites two well known crises: the Asian Financial Crisis of 1997, and the Mexico Peso Crisis of 1994.

In the years leading up to the crisis, many Asian countries had pegged their currencies to the dollar for favourable exchange rate, and had also focussed on an export led growth strategy. But the sudden influx of foreign financial inflows, plus favourable subsidies, ended up creating a massive investor bubble. And the bubble eventually burst: the countries had to unpeg their currencies one after the other, and the currencies’ value fell as much as 38pc, with stocks declining as much as 60pc. The World Bank and the IMF were then forced to intervene to stabilize the countries.

Similarly in Mexico, post the signing of the NAFTA (North American Free Trade Agreement), Mexico enjoyed high investor confidence, and attracted new capital. It also had an overvalued peso, that caused imports to rise and led to a trade deficit. Once Mexico was forced to devalue its currency, it led to massive capital flight. The country was only saved by a bailout organized by the United States and the IMF.

The section of the tweet where Atif talks about the central bank being ‘constrained’ is a little more relevant to home. As is the case with Pakistan, the central bank is keeping the interest rate high to attract hot money. Currently, inflation rates are also high, which would justify a high interest rate. But what happens once inflation starts to taper down? The central bank will have to consider whether to cut the policy rate, or keep it high to continue to attract foreign inflow. Hence, maintaining the interest rate becomes a ‘constraint’ on the central bank.

What’s wrong with Pakistan?

Atif Mian basically says that Pakistan has ignored the two pre-conditions for good central banking. He lists just three cases in the last 20 years that are a reflection of poor central bank governance:

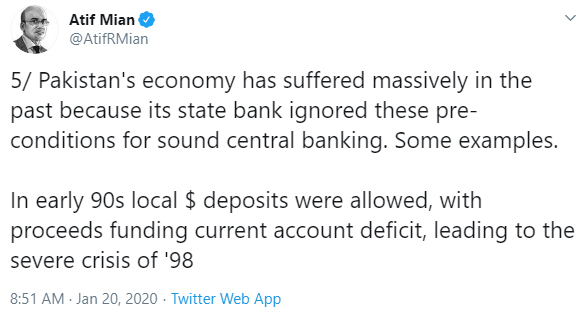

One, local dollar accounts were allowed in the 90s. The proceeds of the local dollar accounts were used to fund the then current account deficit, leading to the severe economic crisis of 1998, where the government literally froze all current accounts.

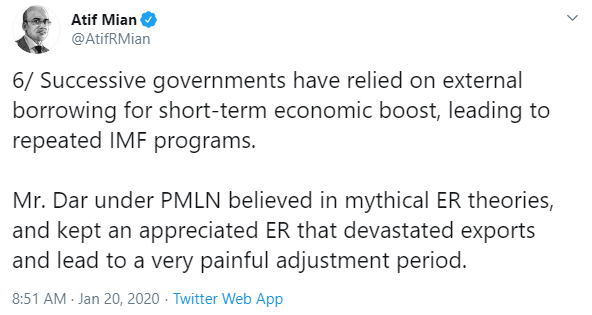

Pakistan’s over use of repeated IMF programs. Since 1958, Pakistan has gone to the IMF a shocking 22 times. Even more dramatically, between 1988 and 200, there were nine different IMF loan agreements, and all were dropped prematurely. According to Atif, this pattern occured because successive governments have relied on external borrowing for short-term economic boost.

Then, the well known overvalued rupee of the mid 2010’s. Atif Mian actually goes on to name Ishaq Dar, saying that the man believed in ‘mythical’ exchange rate theories. The appreciation of the exchange rate impacted exports heavily, and led to a ‘ very painful adjustment period.’

For Atif, these actions have had serious consequences.

“With little confidence that Pakistan will be insulated from external whiplashes, long-term investment does not happen. For example, Pakistan's debt has the lowest maturity among its peers.” he tweeted.

What does this mean? Well, most of the investment is only happening in the short term. The inflows are only coming in T-bills, which have a maximum maturity of 3 months, 6 months and 12 months.

But there isn't a lot of investment in long term debt securities. Look at the break down of all of the foriegn investment coming into Pakistan: of the $2.25 billion worth of foreign investment, only a paltry $24 million was in Pakistan Investment Bonds, or PIBs.

And there are concerns about the short term bills as well: after 3 or 6 months, one will have to hope that the lender rolls over the debt. If they don’t, the government faces a massive risk of having to make large payments.

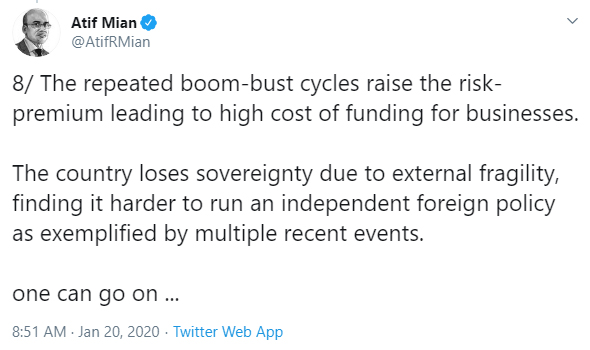

Atif also tweeted: “The repeated boom-bust cycles raise the risk-premium leading to high cost of funding for businesses.”

Essentially, the reason Pakistan had to dramatically raise the interest rate for 4pc to 13.25 pc in a very short time period is because of the risk of Pakistan’s cycles, as shown above.

One of the problems of being such a high risk country, and an unattractive place to invest, is that “The country loses sovereignty due to external fragility, finding it harder to run an independent foreign policy as exemplified by multiple recent events.”

While veiled, it's obvious what Atif Mian is referring to. A country that has to borrow $6 billion from Saudi Arabia, then also has to toe the line when it comes to Saudi’s policies, such as when Imran Khan had to decline attending the Malaysia Summit.

The solution

So what does Atif Mian propose? He suggests a four-step approach for the State Bank to follow:

“(i) Flexible ER management to deliver accumulation of real net reserves, essentially modest current account surplus, for a while. This would also send a strong signal of support to the export sector.

(ii) Discourage short term debt and portfolio flows. Promote long-term capital formation via FDI, but with proper valuation protocols and technology transfer.

(iii) Strong safeguards against money-laundering and capital flight.

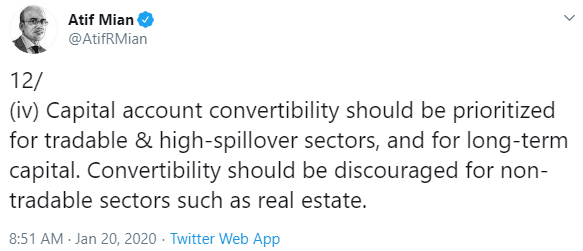

(iv) Capital account convertibility should be prioritized for tradable & high-spillover sectors, and for long-term capital. Convertibility should be discouraged for non-tradable sectors such as real estate.”

The gist of these is essentially this: stop focusing on short term foregn investment in T-bills. ‘Hot money’ inflows might be increasing reserves, but not actually ‘real net reserves’, Atif writes. What’s to stop the money leaving once the interest rates come down? When then will the SBP find the new capital?

Notice also the caveats that Atif writes regarding FDI: the long term FDI has to be based on the fundamentals of an economy (not just speculation), and also technology transfer. Projects like CPEC, are of course long term investments - but constructing roads is not the same thing as creating skills in the Pakistani labour workforce, or transferring new knowledge. And there is little to suggest that CPEC will be able to provide that.

Finally, ease of converting rupees into dollars and vice versa, should be reserved for things like the stock exchange, and not non valuable assets like property or gold.

Atif takes a pretty pessimistic view of the current situation. “We have not seen a coherent framework that takes these principles into account. In fact, on the worrying side, the government has gone out of the way to encourage short-term foreign investment in government T-bills. There is little benefit of such inflows in the case of Pakistan, and much potential risk...if these short-term liabilities continue to build, they can constrain monetary policy and generate external vulnerability.”

At this point one can argue that the State Bank had to take drastic measures in order to make sure we had reserves. As one commentator on Twitter said, portfolio investment is still the easiest way to secure financing.

But if one follows Atif’s thinking: such an influx of foriegn investment does not add anything productive to our economy. So far the only thing ‘good’ the SBP is following is a market-based exchange rate. But it hasn't constituted any structural reforms to actually create market conditions to foster long term investment. Until the SBP is able to do that, the current economic condition remains nothing but a bubble.

A little bit of backtracking?

Were the above tweets a little too dire? Someone (at the State Bank, or in government) clearly thought so, and made it clear to Atif Mian. Or perhaps Atif Mian himself thought his tweets deserved some additional context, based on Pakistani twitter’s reaction.

That’s because in a surprise move, just two days later, Atif wrote some clarifying tweets, which somewhat toned down the previous language.

First he reiterated that “a major positive change has been the move to a market-based exchange rate regime. SBP under new leadership held the fort through the painful adjustment period.” According to Atif, the SBP deserves ‘praise’ (a direct call to analysts to stop bashing the SBP, perhaps?)

He also said that “steps taken towards digitization and greater transparency of the financial sector are welcome changes.” (Profit takes the view that anytime someone mentions the word digitization but doesn’t explain it, it's a filler sentence and can be ignored.)

Amazingly, Atif also back tracked on his critique of the SBP encouraging flow of hot money, instead categorically stating: “It would be wrong to give the impression that the government "caused" the hot money flows - it didn't.”

He then went on to add: “I was critical of the government move to cut taxes to encourage foreign flows into government debt. However, these cuts were on longer-dated bonds, and flows into TBills had started before the change.”

Not so fast, Atif - while it is true that global investors have been pouring in money since at least July (the tax cut was in January), it is also true that the SBP has been perfectly comfortable with encouraging foreign inflows.

For example, in an earlier statement issued in December 2019, the SBP tried to allay fears, and said that international investors investing in debt instruments was a manifestation of their growing confidence in the positive outlook for the country. That statement was an attempt to clarify ‘misconceptions’ about the investments in Pakistan’s debt markets.

“Such investors have been able to move capital in and out of our financial markets without problems for the Pakistan economy,” the statement read - a much rosier picture than the one Atif is referring to.

Still, Atif tries to move the SBP out of the firing line, and instead tries to make the twitter thread a ‘history lesson’.

“The next stage is macro-prudential challenge” - he reiterates once again, adding “Tax incentives and ease of convertibility should be targeted towards FDI, and away from portfolio flows at this stage of financial and economic development for Pakistan. This is the broader lesson from history in my view.”

One wonders what caused Atif to back track so much, and frame himself as a neutral professor, as if he were talking about a paper on macroprudential policy, rather than what he actually is - an extremely prominent Pakistani-American economist, who was briefly on our Economic Advisory Council, and therefore, someone whose words carry immense weight. Guess someone at the SBP noticed after all.

The author is a member of the staff and can be reached at [email protected]

View all articles →4 Comments

No comments yet. Be the first to join the discussion!