It is 2019 and the Pakistani economy is a wreck. The stock market is in free fall with no signs yet of a recovery. The Pakistani rupee has hit its lowest against the dollar in the ongoing year, with the lowest recorded at Rs165.2 against the dollar in July 2019.

In theory, export businesses – that is to say those companies that earn all or a majority of their revenues in dollars – should be thriving in an economy like Pakistan. Why? Because it would increase their earnings in dollars, while their costs, which are local would not increase by much.

This is particularly true for software exporting companies. Software companies do not need to source raw material like, for example, textiles that need cotton as a raw material, the price of which would go up as the dollar goes up, to manufacture a product. Information technology and its related products are a labour-intensive business and majority of the costs are associated with the size of the workforce.

With a weak rupee, revenues would most certainly go up for them while costs will not because a weaker rupee does not make the labour costly all of a sudden. Wages are more a function of supply and demand rather than exchange rate and in an economic recession, oversupply of labour due to unemployment would pull wages down instead of pushing it up.

It is true that investor sentiment drives stock prices but what drives investor sentiment is fundamental company performance. Ideally, the stocks of these companies should be performing better than the stocks of other companies because higher revenues would drive the stocks up. It is, however, anomalous that the stock performance of these companies has been abysmal even though these businesses are flourishing on the back of strong dollar-based earnings.

So are the share prices of these companies truly reflective of their financial performance? At Profit, we examined the case of four publicly listed software companies.

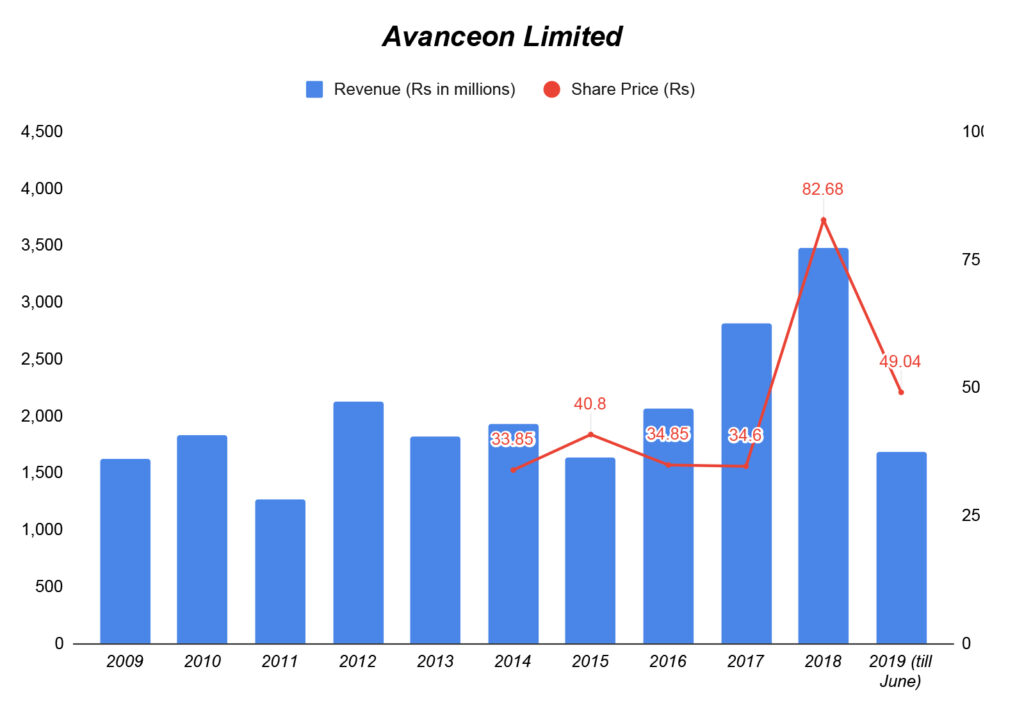

Avanceon Ltd

Avanceon’s core business is automating industrial processes that have a significant software component. Its clients operate in the oil and gas sector, food and beverages, water and waste-water sectors; and other infrastructure projects such as rail and metro systems. The company has a considerable local presence with clients such as Nestle Pakistan, the state-owned Oil and Gas Development Corporation (OGDC), but the majority of its clientele is located in the United Arab Emirates (UAE), the Kingdom of Saudi Arabia, and Qatar, which provides it the bulk of its dollar-based revenues, approximately 60-70% of total sales.

For the half-year ended June 30, 2019, the latest for which financial data is available, Avanceon recorded revenue of Rs1.68 billion. Compared to the same period last year, revenue grew by 16.3%. Company’s gross profit margin was 27.1%, down 383 basis points from last year, whereas operating margin was 35.2%, up 771 basis points from the same period last year. (One basis point is one hundredth of a percentage point.)

The growth is going to be even more because a bulk of Avanceon’s revenue is realised in the 3rd and 4th quarter of the year and historically, the 4th quarter has added revenue in excess of Rs1 billion for the company while the first two quarters are usually half or a little over that. For instance, out of its total revenue of Rs3.48 billion in 2018, the company added Rs1.47 billion in the fourth quarter of the year, giving a jump to its revenues of 42% in the last quarter. Moreover, the company claims that they have $56 million worth of projects in the backlog.

Surprisingly though, Avanceon stock eroded by 39% in value for the six months of 2019 (from Rs80.61 on January 1, 2019 to Rs49.04 on June 28, 2019 at closing price), while the rupee depreciated by 34% during the same period. And for a little less than the 9 months of 2019, from January 1 to September 20, Avanceon’s stock price fell from Rs80.61 to Rs31.66 at closing price.

Between January 1, 2018 and December 31, 2018, Avanceon’s stock appreciated by 135% to Rs82.68 on December 31, 2018 from Rs35.18 on January 1, 2018. For the year 2018, its revenues increased by 23.7% from 2017. Avanceon’s financial year starts on January 1 and ends on December 31 each year. For the financial year 2018, the company realised revenues of Rs3.48 billion, against a revenue of Rs2.81 billion in 2017.

For the year 2018, the rupee lost 15.5% of its value and the company witnessed cost increases of 34.3% from the previous year, shrinking its gross profit margin by 558 basis points to 29.1% for 2018 compared to 34.7% in 2017. The company said that in 2018, it witnessed a fixed cost increase of 36% due to Rs95 million in provisions for bad debts and earning in excess of billing and written-off of old balances. Other increases in costs include a 13% net increase in salaries and other administrative expenses and cost of selling due to inflation.

Meanwhile, Avanceon’s operating profit margin was at 26.3%, an increase of 258 basis points from the previous year.

Bakhtiar Wain, the CEO of Avanceon Ltd, attributes the lacklustre performance of the Avanceon stock to the bearish investor sentiment: “Everything is outstandingly good at the company but the market has been in a freefall,” Bakhtiar Wain tells Profit. “Our business and results couldn’t have been better. This is essentially a blip that will go away which will go away automatically when the sentiment changes,” he says.

For a business like Avanceon, a bust in any of the sectors that it operates in abroad would not augur well for the company. A recession in Avanceon’s business would come if there is a recession in any of the sectors they operate in internationally, for instance in the oil and gas sector in the Middle East. But Bakhtiar says Avanceon is hedged from such dips in the business because of their diversification into other sectors.

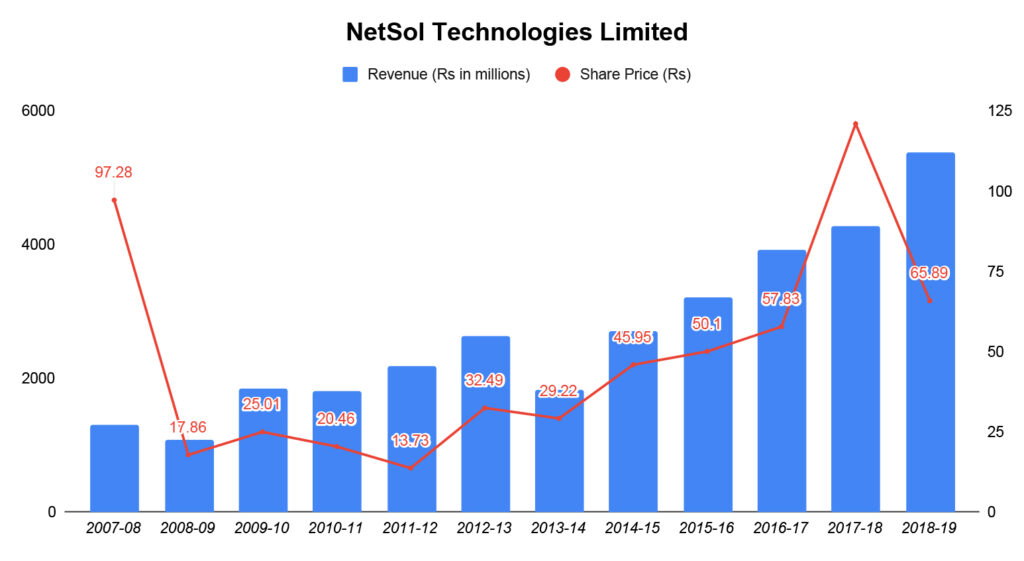

NetSol Technologies Ltd

There is a great hype surrounding NetSol and a great deal of that comes from the very public profile of its founder Salim Ghauri. After returning to Pakistan from Australia after a 17-year stint as an IT consultant, Ghauri laid the foundation of NetSol in 1996 using seed funding from his brother Shahab Ghauri. For the 23 years it has been in existence, NetSol has remained an exporter of IT services to the asset finance and lease management, banking, insurance and information technology sectors. It is listed on the Pakistan Stock Exchange (PSX) and trades under the symbol ‘NETSOL’ and was the first and only Pakistani company to be listed on the NASDAQ in the United States.

NetSol’s business has a dominant share in the international automobile lease industry where it serves a diverse client base across the world through its core flagship and project the NetSol Financial Suite (NFS) – which is essentially an asset financing software application that helps lenders manage their lending. Almost all of its customers are international and that includes automakers Mercedes-Benz, Toyota, Volkswagen, BMW, Nissan and Hyundai among others. The government of Sindh was its only Pakistani client according to its financial report for 2018.

For the full year ended June 30, 2019, the latest period for which financial information is available, NetSol posted revenue of Rs5.4 billion, a growth of 25.6% compared to last year. For the same period, the rupee depreciated by 34%. The company’s gross profit margins for fiscal year 2019 were 38.9% against 45.2% last year, while operating profit margins for fiscal 2019 were 25.2%, compared to 27.1% the previous year. Meanwhile, over that fiscal year, NetSol stock fell by 48.1%, to Rs65.89 on June 28, 2019 from Rs126.84 on July 2, 2018.

Salim Ghauri, the CEO of NetSol, told Profit that the Pakistani stock market is not able to appreciate the work NetSol is doing and the domain it has built in the last 25 years.

“Until the market starts appreciating [our work], we will see these kind of values but I am very confident that the market will soon see how we are evolving into a very high-value tech organisation and once the market starts seeing the additional work delivered by NetSol, we will see better values,” he says. “The market is overall down and that has affected us also but I believe that this is in the short run,” he adds.

During fiscal year 2018, NetSol stock appreciated by 116%, to Rs121.07 on June 29, 2018 from Rs56 on July 3, 2017. For the same period, the company reported a revenue of Rs4.3 billion, up by around 10% from the previous year. Its gross profit margin was 45.2% while the operating profit margin was 27.1%, an increase of 1,709 basis points from the previous fiscal year when it was a relatively smaller 9.98%.

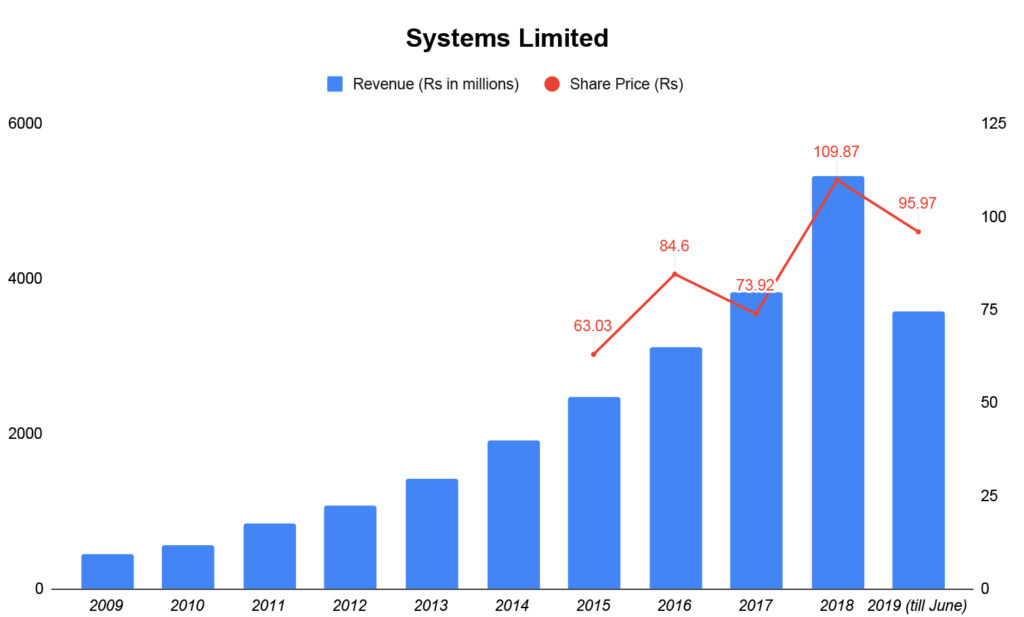

Systems Ltd

Systems Ltd is a public limited company incorporated in Pakistan under the Companies Act, 2017, and listed on the PSX under its trading symbol ‘SYS’.

The Company is in the business of software development, trading of software and business process outsourcing services. The Group comprises of Systems Ltd (Holding Company) and its subsidiaries – TechVista Systems FZ LLC and E-Processing Systems (Private) Ltd. The company’s revenue is primarily from software development and IT services work subcontracted by its subsidiary TVS operating in the Middle East region and its associated company Visionet Systems operating in the North America region. Over 73% of its revenue is export based. Systems Ltd’s financial year ends December 31.

For the year 2018, Systems Ltd’s stock appreciated by 46.5% to Rs109.87 on December 31, 2018 from Rs75 on January 1, 2018. While the dollar appreciated 15.5% against the rupee in 2018, the company revenues swelled by 38.9% to Rs5.3 billion from Rs3.8 billion in 2017. Systems’ gross profit margin was 28.7%, down 126 basis points from 2017 when it was 30.0%. Operating profit margin, on the other hand, was 20.17%, up 491 basis points from the previous year.

For the year 2019 through September 20, Systems’ stock lost value by 24%, down to Rs82.30 on September 20, 2019 from Rs108.70 on January 1, 2019.

The company has thus far posted half-yearly report for the period ended June 30, 2019. So for a fair comparison, we would look at the company’s stock performance for the 6-month period of 2019. For the period in consideration, the company’s stock shed 11.7% of its value to Rs95.97 on June 28, 2019 from Rs108.70 on January 1, 2019.

For the 6-month period that the currency depreciated by 34%, the company posted a 53.61% increase in revenues to Rs3.6 billion, from the same period in 2018 when the company posted revenues of Rs2.3 billion. Meanwhile costs increased by 47.6% in the first half of 2019 compared to the same period last year, whereas the gross profit margin increased to 30.8%, up 283 basis points from 28.0% in 2018 for the same period. The company had an operating profit margin of 25.5%, an increase of 530 basis points from 2018 when it was 20.2%.

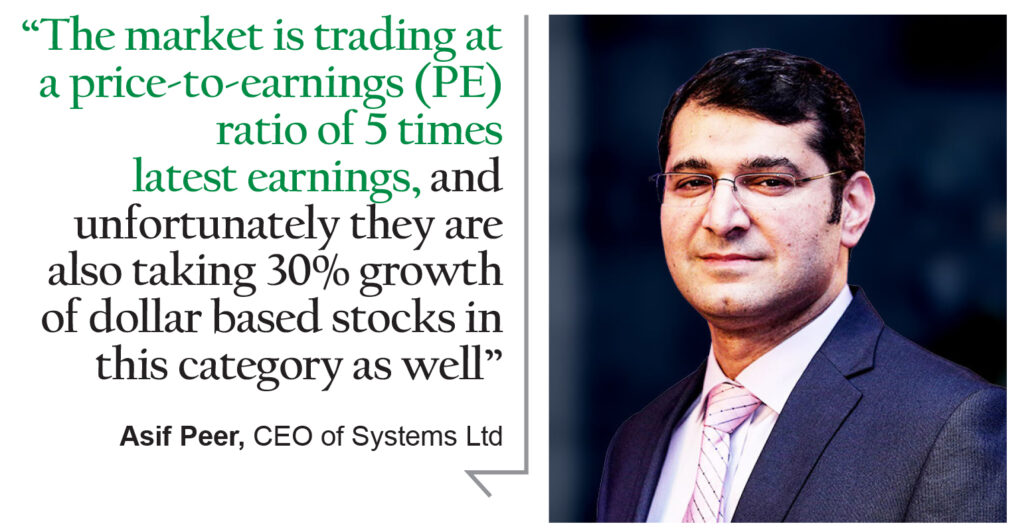

When asked why the share price of Systems Ltd is down even though the business is flourishing, Asif Peer, the CEO of Systems Ltd, told Profit that the market is trading at a price-to-earnings (PE) ratio of 5 times latest earnings, and unfortunately they are also taking 30% growth of dollar based stocks in this category as well.

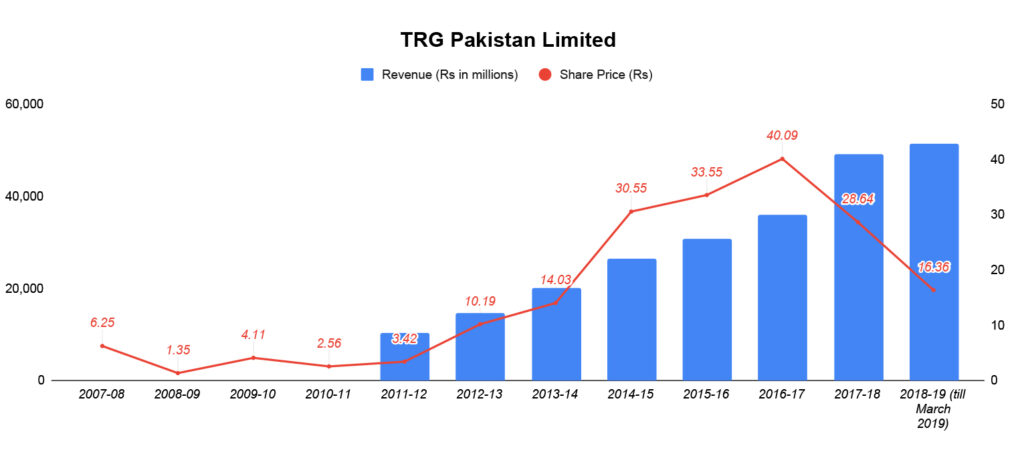

The Resource Group (TRG)

The Resource Group (TRG) is the brainchild of Zia Chishti – a US-based Pakistani businessman – who still serves as the CEO of the company. Zia’s entrepreneurial achievements are remarkable by all standards. The man single-handedly built two billion-dollar companies – with Align Technologies (the makers of the first ever brand of dental aligners called Invisalign) being the first one.

TRG Pakistan Ltd was incorporated in Pakistan as a public limited company and is listed at the Pakistan Stock Exchange (PSX) under its trading symbol TRG. Most in Pakistan know TRG as a call center company, but it is actually a holding company that acquires, invests in and manages operations relating to business process outsourcing, online customer acquisition, marketing of Medicare related products, and contact centre optimisation services through its subsidiary, The Resource Group International Ltd (TRGIL).

The bulk of the revenue for the company comes from its IBEX business, a subsidiary, which is essentially the call center business which has call centers in the USA, the UK, Canada, Jamaica, Nicaragua, Senegal and Pakistan. The second cash cow for TRG is its Afiniti subsidiary which uses artificial intelligence (AI) to pair employees of the company with its customers to improve profitability.

TRG’s financial year starts July 1 each year and ends on June 30 of the subsequent year.

The first nine months of FY19 was a period of highly significant growth for TRG as their consolidated revenues reached Rs51.3 billion, representing a 43.5% increase over the same period last year. The company said that the increase has been broad-based and took place across all of their major operating subsidiaries and was also aided by a weaker rupee against the US dollar. The IBEX business alone was Rs42.7 billion. For the same period, the currency depreciated by 15.7%.

The company’s gross profit margin increased to 36.3% from 28.5% during the first nine months of 2018. The operating profit margin also increased by 983 basis points from -9.81% in 2018 to 0.02% in 2019. TRG stock lost 20.3% of its value, going to Rs23.06 on March 29, 2019 from Rs28.95 on July 2, 2018. However, from the start of this year TRG stock has lost 43.1% of its value, falling from Rs23.41 on January 1 to Rs13.31 on September 20.

Why? Because it was being dragged by the weight of the company’s bad financial performance, making billions in losses.

For the financial year 2018, TRG raked in revenues of Rs49.1 billion. It had a healthy gross profit margin of 29.2%, up 2,043 basis points from the previous year when it was just 8.8%. However, the company made losses from operations of Rs3.5 billion, which was an improvement from 2017 when company made losses from operations of Rs8.0 billion before taxes and finance costs. And that is before taxes and finance costs. The profit margin for 2018 was -7.2%, an improvement of 15.0% from the previous year (2017) when the operating profit margin was -22.2%.

TRG attributes its losses to investments for expansion of its Afiniti subsidiary. The Afiniti cost base during fiscal 2018 increased to Rs9.6 billion, up from Rs5.8 billion during fiscal 2017. To fund its expansion, Afiniti closed a debt funding round in financial year 2018 for a total of $60 million, which included the refinancing of prior debt. The Afiniti subsidiary is also a significant source of revenue for the business. For the financial year 2018, Afiniti business added Rs7.5 billion in revenues.

How to approach these companies as an investor

It is evident that the companies are flourishing financially, even TRG, which even though it is currently making huge losses, it is on track to profitability with its operating profit margins in the positive after a plunge in the negative for a few years.

While it is certain that the overall economy has affected investor sentiment that has pulled the share prices of these companies down, when the dust settles, the share prices are going to adjust to their actual value based on the financial performance of these companies. But for now, however, even the best of these businesses are not correctly reflected in the stock market.

Maha Jafer Butt, director of research at Capital Stake, tells Profit that the overall sentiment in the equity market is low and concerns about the overall economy have kept investor confidence and participation low in the market.

“With the interest rates so high, institutional investors are more inclined towards investment in T-bills (treasury bills), which are low risk compared to equities,” she says, adding that when sentiments improve, it is expected that the overall market will pick up and share prices shall recover.

I don’t know how can anyone just write an article related to finance and stock market with apparently little to no knowledge about share pricing. The funniest thing is the comparison between revenues and share prices and the graphs presented in this article. It tells nothing!

Companies are known to hide sales and inflate costs. Wheres the income and EPS numbers for these companies in all those years? Graph comparison between EPS and share price would have told a better story and more understanding to investors that whether these stocks are declining due to market, or due to companies own performance or a mixture of the two!

I think your criticism is disproportionate to the magnitude of the error. The author has provided the profitability numbers for all four companies. The revenue to share price graph is however not the best way to look at things.

And what about payouts?? Apart from revenue, distribution of dividend is also important.

So, please share their dividend history.

Agreed. Dividend payout/Dividend policy for the year or the past trend is highly SP driving factor.

Everyone knows that revenues are just a made up number the way accounts are prepared in Pakistan. Hardly anyone shows the real Sales. The companies above are not blue chip corporations with high quality auditors. So comparison of revenue to share price is utterly pointless.

There are 3 recognized ways of calculating intrinsic price of a stock. Cash flow discounting, P/E multiple and dividend discount model. So share price can only be seen by first comparing it with EPS and Dividends throughout all those years. It’s surprising to see such a long article wondering why the stock price is so low for the 4 companies without even mentioning the above info and what should be the target value as per the author. Looks like paid promotion!

What’s the best stock at the moment in terms of dividend over long run ?

Comments are closed.