How to capitalise on the pandemic and import cheaper gas

The coronavirus pandemic will affect everything and there is no reason to believe that the energy supply chain will be any different. For an energy-import dependent country like Pakistan, that matters a great deal more than a country that has sufficient domestic supplies of energy.

Before taking the sensational and perhaps drastic step of declaring an energy emergency, Pakistan needs to weigh its options, evaluate what the country’s best possible course of action could be, and adopt the most favourable and feasible energy scenario possible.

Saying this makes sense, of course. It is always good to weigh options and figure out the most favourable situation. Where the problem comes in is that to do this, you need to evaluate past data and mine through it to find the root cause rather than any hasty measures.

And before we begin panicking about the liquefied natural gas (LNG) supply chain facing collapse, or pointing fingers left right and center, it is important to make use of competent, knowledgeable people, to move forward under their advice to achieve our collective goals. And with the global LNG supply chain in a mess, and Pakistan’s domestic gas production at an all-time low, here is the state of the possible energy crisis we may be facing.

Where things stand

What will be most important in this process are the facts, and a good place to start is the Oil and Gas Regulatory Authority’s (OGRA) flagship 2018 “State of the Industry Report”. In this report, OGRA noted that “domestic gas production would continue to decline from about 3.3 billion cubic feet per day (bcfd) in the fiscal year ending June 30, 2018 to less than 1.6 bcfd by 2028 while the gas demand would keep going up to reach 8.3 bcfd by that year with shortfall increasing to 6.6 bcfd by fiscal year 2028.”

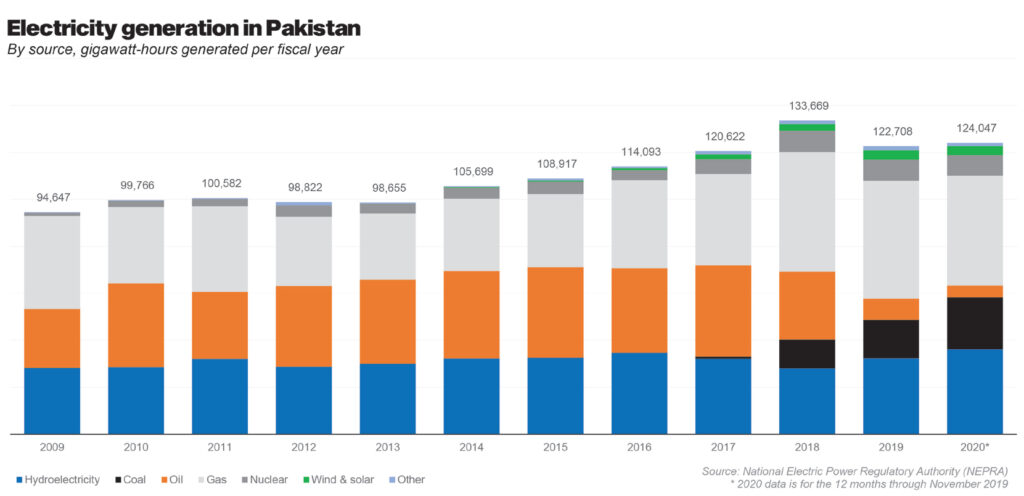

To put this in context, natural gas’ share in our primary energy mix is around 48% and the share of regasified LNG in the overall gas supply increased to 23% in fiscal 2018, the latest year for which complete data is available. That made up the shortfall due to proactive steps undertaken by the energy ministry.

The power sector was the main consumer of natural gas during the fiscal year 2018, consuming 37%, followed by the domestic sector with 20%, fertiliser with 17%, captive power with 10%, industrial sector with 9%, transport with 5%, and the commercial sector taking up the smallest slice with a 2% share.

Meanwhile, as domestic gas production falls, things turn in favour of LNG, which is the cheapest and simplest imported gas available. In fact, according to an article published in The News, LNG has saved the country $5 billion after it substituted the expensive furnace oil. Over 19 megatons of LNG was imported since 2015, resulting in import bill savings worth 2% of gross domestic product (GDP, or the total size of the economy). And while there had been detractors in the Senate Energy Subcommittee who had raised concerns over having no lower or upper limit in Pakistan’s long-term LNG supply agreements, that arrangement is now proving to be beneficial.

On the domestic gas front, production continues to decline, at least in part due to the fact that the government controls pricing, even as the industry relies on equipment and costs that are often globally set, meaning there can be a strong disincentive to invest in domestic natural gas production.

It is important to remember that gas pricing for producers in Pakistan has not been a stable business. Back in the 1950s and 1960s, prices were determined on a cost-plus basis. Since 1985, wellhead gas pricing has been revised intermittently and is linked to a reference of crude or fuel oil price taken from a basket of imported Arabian crude oil during the last six months. Through the 2012 Petroleum Exploration and Production Policy, the government has also placed an upper cap on prices received by producers in operation in the form of an S-curve, specifying both a floor and ceiling.

Under the policy, the government set wellhead gas price in Zone-III at $6 per million British thermal units (mmbtu), $6.30 in Zone-II, and $6.60 in Zone-I. The Petroleum Policy also provides a comprehensive pricing mechanism for offshore zones: Zone 0, for example, has been set at $7 per mmbtu for shallow, $8 for deep, and $9 for ultra-deep exploration with other incentives.

However, prices are different for each of the 55 gas fields, since they are set by the petroleum policy applicable at the time when they were discovered. So, for example, Mari provided the government with the lowest price for its field located in the 1950’s at around $1.40 per mmbtu compared to the 2012 pricing policy, which has set it to about $5.70 per mmbtu. Its gas purchase agreement also allows a minimum return on equity of 30% net of taxes on shareholder’s funds.

In July 2018, OGRA increased wellhead prices in a 30% adjustment. Pakistan’s current wellhead gas prices are at $3.50 per mmbtu on average, which is 10% higher than those in India and almost double the prices in Bangladesh. Locally produced gas prices in India are $3.23 per mmBtu, which were as low as $1.50 in 2017. Bangladesh’s wellhead prices have varied between $1.60 and $2.80 per mmbtu, but saw an upwards spike when they also recently increased gas prices by 34%.

Well-head prices for producers, of course, rely in large part on what the government allows gas distribution companies to charge the end consumers. On that front, the government weighs a combination of factors, including incentives to industrial consumers of natural gas, as well as political considerations in ensuring that household consumers have access to cheap fuel.

Bangladesh’s gas prices are the lowest in the world. Of special significance is the 37.6% rise in industrial tariff from $2.66 to $3.66 per mmbtu. Its industrial tariff is $3.66 per mmbtu as compared to $4.01 in the United States; the latter is perhaps one of the cheapest gas producers in the world due to its shale resources.

Pakistan’s industrial gas tariff at $7 per mmbtu is comparable to or slightly lower than that of many countries in Europe and Asia. A special tariff for export-oriented, tax-exempt industries (textile, leather etc) has been kept at Rs786 ($5.24) per mmbtu.

Domestic sector gas tariff in India and Bangladesh is $10 and $4.25 respectively, while in Pakistan, $10 per mmbtu is the highest slab.

OGRA had decided to increase gas price in January 2020 for domestic household gas consumers by 191%, for the fertilizer sector 135%, 31% for consumers falling under the category of roti tandoor, commercial, industrial, zero-rated export industry, captive power plants, compressed natural gas (CNG), cement and power plants.

However, after complaints from literally all of these consumers facing huge losses, the government put the scheduled increase on hold for six months. The alternative, if the prices had gone up of course, would have been LNG. It is estimated that at an oil price of $50-55 per barrel, contracted LNG arrives at a cost lower than domestic price benchmarks.

With all this going on, there is also an opportunity in the supply chain situation as well. Goldman Sachs, the global investment bank, stated in a research report in March 2020, that the bearish cycle might end in 2021 due to lower production in Europe and in the United States. This, along with higher LNG purchases, would help tighten up the market, with some analysts forecasting prices in the winter of 2020-21 to be at $5.80 per mmbtu, and at an even lower $5.50 per mmbtu in summer 2021.

There is also some misrepresentation of the prices other countries in the region are paying for LNG imports from Qatar. The numbers quoted by people who suggest this are not true: Pakistan continues to buy LNG at competitive rates, and while India may have secured a few shipments are favourable prices, Pakistan’s longer term contracts are likely to result in favourable rates over the next few months, particularly as the benchmark Brent crude price has fallen from a rolling three-month average of $63.76 in January, to $50.97 in March, and is now down to $33.89 per barrel.

That price of oil has an effect on LNG import prices, which are benchmarked to oil prices. The eight cargoes Pakistan is importing from Gunvor, QGas and ENI will soon be at an average price of $3.2 per mmbtu (benchmarked to 12.97% of Brent oil prices of around $30 per barrel) which could decrease to $3.04 per mmbtu if Pakistan was also to buy 4 additional cargoes at future spot price of LNG of $3.3 per mmbtu (benchmarked to 10% of Brent crude prices of $30 a barrel); thereby saving the country approximately $200 million per year in LNG terminal charges.

Coronavirus impact

While spot prices have gained slightly, they are still trading at their lowest for this time of the year. They fell to a record low last month as the coronavirus outbreak dented industrial gas demand from China, the world’s second-largest LNG buyer. While more businesses have reopened in China in recent weeks, analysts do not expect activity to return to normal levels for some time yet with how the Covid-19 pandemic is turning out.

According to Giles Farrer, research director at Wood Mackenzie, a leading energy consulting firm, the forward curves for prices suggest that there might be some shut-ins of LNG, although this may not necessarily be from the United States. “US LNG projects selling on a Henry Hub-plus basis will also be perceived as less competitive than oil-indexed LNG,” he claims. “As a result, there will be fewer LNG projects taking FID in 2020 and 2021.”

Put in layman’s terms: US natural gas prices are the only major market in the world that are not linked to global oil prices, and will thus not see as steep a decline in prices compared to LNG from other parts of the world, which will see a decline in prices due to the sharp drop off in oil prices.

LNG export terminal projects in Mozambique, Mauritania, Senegal, and Australasia will also come under pressure, translating into lower global supply between 2024 and 2027. By contrast, Qatar, with low fiscal breakevens and an ambition to grow LNG market share over the long term, is expected to continue to push forwards with its North Field expansion plans.

The news about LNG shipping in April is that LNG suppliers are currently flooding the market with excess spot cargoes, generating fresh price problems, as demand dwindles globally due to the coronavirus outbreak. And with major buyers such as India, Italy, and Spain, among the worst hit, things are looking a little bleak.

Total LNG deliveries to Europe are expected to reach nearly 11 million tonnes, a 14% hike from the previous record set in December, according to IHS Markit, which said the supply push comes as gas demand is collapsing at double digit rates. “Asian buyers are reselling volumes purchased from the US and portfolio sellers are offloading their excess cargoes as well,” says Michael Stoppard, IHS Markit chief strategist for global gas in a media interview.

Given the uncertainty, LNG buyers in North Asia had opted for a ‘downward quantity tolerance’ (DQT) when negotiating their annual delivery programmes. Some buyers are now exercising the clause that allows them to cut volumes by up to 10%. “We’re seeing more sell tenders these days due to a combination of factors like coronavirus and DQT, but this also means that when demand rebounds, buyers will return to the market to seek spot cargoes,” a Singapore-based LNG trader said.

One gas trader in Spain said everyone was using all the flexibility available in contracts during this time. “If a contract is not in the money and has downward flexibility, everyone is doing it in whatever they can: cancelling a cargo, cancelling volume within a system,” they said. “Right now, if we could cancel, depending on the contract, we would cancel everything.” Last week, Qatargas approached buyers in Asia and Europe to offer cargoes for delivery or loading in April, sources said.

Traders said it had likely been forced to seek buyers for its excess cargoes after being issued with a force majeure notice by Petronet LNG. Qatar is India’s biggest LNG supplier. Cheniere Energy, the largest US LNG exporter, also offered a cargo for loading in early April from Sabine Pass, which traders claimed was unusual. In Australia, Malaysia’s Petronas offered a cargo for loading in May from the Gladstone plant in which it has an equity stake, likely due to a cancellation from a buyer, an industry source said.

Where does Pakistan stand?

So why is Pakistan lagging in taking advantage of the global gas glut when gas was selling in the future at $2.50 per mmbtu and now at $3.4 per mmbtu. Other price-conscious buyers are already taking advantage of record low prices and soaking up some of the excess supply.

The window may be short, as short-term demand for LNG has improved over the past month, so now is the time to move if there ever was. India’s Torrent Power sought a cargo for early May, Gujarat State Petroleum Corporation (GSPC) sought 11 cargoes for delivery over April to March, next year and Gail may also issue a swap tender offering cargoes from Cove Point in the United States and seeking cargoes for delivery into India.

Chinese utility Guangdong Energy group was also seeking five cargoes for delivery over April to December whereas Turkey’s EgeGaz also sought two cargoes for delivery in April and June.

Still, supplies are ample as cargoes were offered in the spot market. Angola LNG offered a cargo for delivery in April to as far as India while Oman LNG offered three cargoes for delivery over March, June and July.

Currently, Pakistan has the ability to buy four cargoes on spot prices every month as spare terminal capacity is available and should do so. But then where is this inaction coming from?

The order for the additional four cargoes needed to be placed with measures ensuring LNG utilisation despite lack of demand due to the economic downturn. This could realistically have been achieved through the enforcement of utilisation of LNG in the power sector, especially considering the sector used under 140 million cubic feet per day (mmcfd) in the first week of March, despite the demand being 240 mmcfd.

Sui Northern Gas Pipelines (SNGP) should also be busy securing additional customers, providing LNG to export industries and CNG, while the energy ministry should be reviewing indigenous gas production (average price proposed by OGRA at Rs707 to 785 per mmbtu), and deferring cargoes of long term contracts if beneficial. They should also have their hands full reviewing tenders or reopening signed sales agreements, if deemed prudent.

All of this would help achieve desirable results, especially if these actions had been undertaken with the utmost professionalism and good faith. The problem is, that the oversupply period will not last long, and will be back to normal as soon as the world GDP improves. The pandemic impact on the economy of China is already reducing and the Russia-Saudi Arabia oil turmoil has ended. Meanwhile Pakistan has opted to defer two cargoes but probably should do two more soon.

What can be done?

There are, however, some options to further reduce gas volumes and benefit from the lower cost of oil. For now, PetroChina has already invoked force majeure in its long term contracts and refused shipments. The combination of falling economic activities, a Northern hemisphere warm winter, and now the coronavirus effect, are all making the LNG supply situation and the pricing of LNG under long term agreements more critical. However, the Pakistani government seems uninterested in invoking force majeure

The tsunami of new LNG production now hitting the market mainly from the US, Australia and Russia is unprecedented. LNG sellers and buyers need to sit down together to analyse the LNG import agreements having an indexed price, and work out a solution. If the parties to the long-term LNG sales and purchase agreement (SPA) are unable to find a solution, then they should seek independent professional help. The European gas industry went through a similar problem a decade ago and might be an example to learn from.

Depending upon the governing law and upon the specific terms used, there are potentially good arguments for both the Covid-19 event being effective as a reason to excuse or suspend performance [based on force majeure] and, also, for it not being a strong claim.

However, both buyers and sellers need to tread very carefully. If a buyer is allowed to claim hardship under an SPA and is also able to demonstrate to a court that they are suffering hardship as a result of the pandemic, then a judge acting under English law has in court has the power to annul the SPA.

Pakistan has seen a lower demand due to the economic downturn. In addition to this, the country can legitimately claim that it has shut down its ports because of fear that keeping them open would help spread the virus.

In addition, terminal capacity should be allocated on “use it or lose it” basis and not monopolised by traders as is happening presently.

The two terminal operators – Engro Elengy and Pakistan GasPort – are allocating capacity to only Shell and Trafigura. This is anti-competitive and will not develop imports by the private sector. The government of Pakistan is now considering taking over the PGPL terminal, assigning a new operator, or settling the penalty and other contractual matters. If it does take over GasPort, then the Sui Southern Gas Company (SSGC) and GasPort terminals could be operated as merchant terminals, freely available to anyone who wants to use them.

Ultimately, however, the big fix that is needed is in the gas prices charged to consumers. There needs to be a single gas price charged to all consumers and then any households that cannot afford gas should be subsidised through cash transfer programs like the Benazir Income Support Program (BISP).

Sheikh Imranul Haque is a former energy executive with decades of experience in the industry, including stints as CEO of Engro Elengy and and Managing Director of Pakistan State Oil

Comments

No comments yet. Be the first to join the discussion!