JazzCash, Mobilink’s favourite child?

The mobile financial services market has become significant for Jazz, and its success is one of the major things the company is betting on

Pakistan’s largest telecommunication company, Jazz, is on an experimental spree to overhaul its business model. The Cellular Mobile Operator (CMO) is focusing on the 4G multiplay, meaning the operator doesn’t only want to remain a pipeline, but also evolve as a destination for its customers. Its focus is to encourage users to spend more time on the network by using its digital apps thus, generating incremental revenue.

The CEO of Jazz, Aamir Ibrahim, while on a panel discussion arranged by Tabadlab last year, stated, “Jazz was a telecom company. Today we are a tech company; in the future, we’ll be a data company.’

But, what Jazz can be before that is a bank, a digital bank.

The digital financial services (DFS) wing of the company that operates under the brand name of JazzCash has been a successful venture. Considering that this was not Jazz’s forte, the success on the financial services front becomes even more commendable.

However, the company seems to be in a rush when it comes to DFS. It has set its sight on massive growth targets built on ambitious lending plans backed by growth in mobile wallet users.

Yet, the journey is likely to be risky, with chances of regulatory, structural and internal deficiencies creating stumbling blocks along the way.

In this article, we will try to explore where the telco’s financial services product currently stands, what is the journey ahead, and the myriad challenges they are likely to face.

JazzCash

Contrary to popular belief, JazzCash is not a company but a brand under which Jazz offers its financial services. The service delivery is governed by a joint venture contract between Mobilink Bank and Jazz. The bank takes care of the operational aspects while Jazz looks after technology, marketing and other stuff.

As of December 31, 2021, JazzCash had around 39 million mobile wallet accounts holding around PKR 36 billion in deposits. This was a significant growth given that in 2020 it had approximately 28 million wallets while the digital deposit base was PKR 29.5 billion.

Furthermore, the closing portfolio for digital lending was around PKR 2 billion while total loan disbursements grossed up to PKR 10-12 billion in 2021. The relatively short tenure for digital loans (around 4 weeks) means that Jazz can lend a more significant amount with a comparatively lower deposit base.

Profitability, too, was great for digital lending as with a recovery rate of 95% and an exuberant annualised interest rate of between 160% to 180%, JazzCash lendings were clocking in an Earnings before Interest Tax, Depreciation and Amortisation (Ebitda) of approximately 50%

However, the overall JazzCash operations still incurred a loss in 2020 and 2021. Why did this happen?

Well, amid the pandemic, the State Bank of Pakistan (SBP) issued circular instructing banks to abolish Interbank Fund Transfer (IBFT) charges to account holders who could no longer go to bank branches or branchless banking agents because of the pandemic restrictions to make these transfers. Slashing these IBFT charges promoted digital payments but took away the primary source of revenue for branchless banking operations such as JazzCash.

Simultaneously, growth in the adoption of digital financial services encouraged Jazz to re-think its strategy and move from a payment service provider to a digital bank. As a result, the mobile financial services market has become significant for Jazz. Its success is one of the major things that the company is betting on, not just for future profitability but also for overall valuation.

VEON, Jazz’s parent company, as part of its acquisition of Warid from the Abu Dhabi Group (ADG) on July 1, 2016, entered into an agreement with the group. According to the terms of this agreement, ADG would have a right, upon the fourth anniversary of the acquisition, to sell their remaining 15% stake in the combined business (now Jazz, formerly Warid) to VEON at the then established fair value.

Therefore, a valuation was completed in December 2020 by the Bank of America, which VEON appointed while ADG appointed City Bank. As a part of the process, both banks estimated the value of JazzCash to be close to $245 million. However, the valuations were significantly affected by the negative margins from JazzCash operations.

Still, that meant the company was deriving almost 10% to 15% of its total value of operations in Pakistan from JazzCash, primarily a payment services provider.

Ambitions

As their conventional business model was disrupted by regulatory intervention, putting at significant risk operations of the company, Jazz now sought an alternative to turn things around. Thus, it decided to fast-track growth on the digital lending front.

It has plans to open up the mobile user base of 75 million customers for JazzCash lending and has set an aim for disbursing PKR 50-60 billion in the financial year 2023. The lending would consist of 30% consumption and 70% productive loans as Jazz is still using a microfinance licence that restricts certain lending types.

The consumption loans would comparatively be smaller, between PKR 1000 to 5000. While productive loans would be 10 times higher in limit. The telco plans to charge monthly interest on these loans between 5% to 10% depending on the time, nature and amount of lending. Also, as per sources, it is expected that JazzCash would be able to maintain an EBITDA margin of 50% on its digital lending.

However, what is not clear yet is how these loans are going to be financed. One way could be by utilising the surplus deposits of Mobilink Bank. There were PKR 21 billion of surplus deposits over advances for the bank by the end of last year. Additionally, the bank was carrying zero long-term borrowing on its balance sheet (Which probably explains why Mobilink Bank held back when the whole microfinance sector was on a lending spree).

As per sources, the company is also targeting PKR 50 billion in Jazz Cash Deposits by the end of 2023.

PKR in Millions

Source: DFS Rollout Plan in VEON’s 2020 strategy document

Source: DFS Rollout Plan in VEON’s 2020 strategy document

But expanding the digital lending portfolio would be an uphill task for Jazz given that in comparison to their ambitions, adoption of DFS is still on the lower side. The company is exploring partnerships to introduce a Buy-Now-Pay-Later model for its consumption loans. A source, on the condition of anonymity, told Profit that one big avenue for such disbursements would be gaming apps like Pubg where JazzCash aims to provide credit for In-App purchases.

Yet, the biggest lending chunk would be to the Micro Small & Medium Entities (MSMEs). Jazz’s strategy is built around providing working capital to this segment and generating the maximum loan cycles from borrowers of the segment.

“Mobilink Bank has a keen interest in the digital financial sector of Pakistan and we see a huge potential market in the growing MSMEs of the country,” said Sardar Abubakr, the chief finance and digital officer of Mobilink Bank, during a discussion with Profit earlier this year.

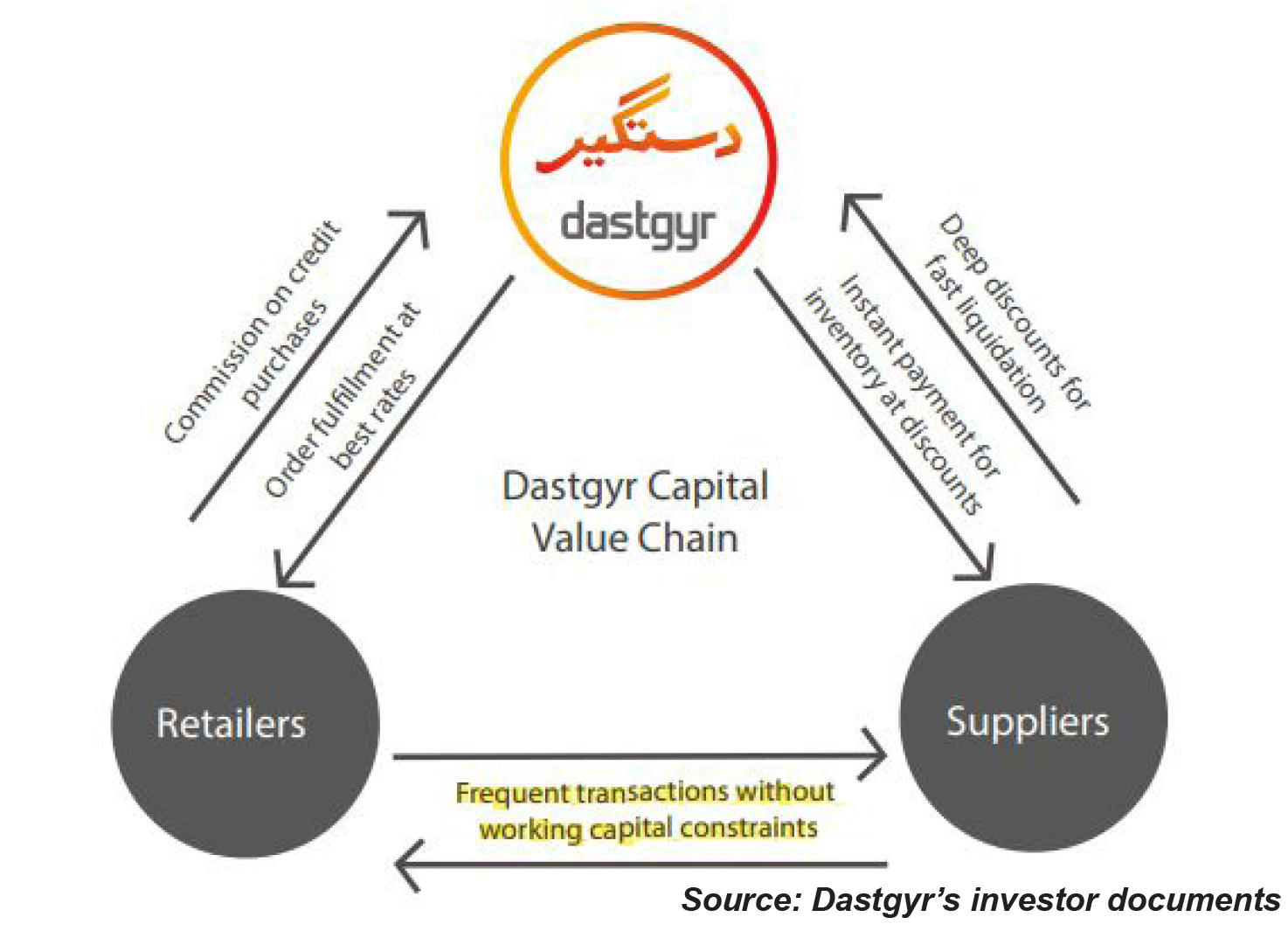

To explore strategic opportunities on this front, JazzCash relies on its group company, VEON ventures, to invest in startups and businesses that can help Jazz develop an ecosystem. One such example is Dastagyr, a B2B marketplace startup.

“After Telecom our biggest foray is in fintech. Retailers that are customers of Dastgyr are also Jazz’s customers. We can fulfil their working capital and payments needs while also benefit from the data provided by Dastgyr for better credit scoring.” Aamir Ibrahim, CEO of Jazz, stated in a podcast interview in June this year.

Though the opportunity to finance retailers might be obvious, what is more, interesting is Ibrahim’s comment on credit scoring; a factor that could be the deal breaker for Jazz’s lending ambitions.

The data Jazz’s head honcho was referring to is likely to be generated through D-Core. This is Dastagyr’s backend data app which exchanges information with other interfaces of the startup, such as the retailer app, taking in relevant inputs and feeding back actionable insights and recommendations.

It helps the company to determine the creditworthiness of retailers from buying patterns, including order frequency and average GMV to determine buying power as well as the ability to pay set credit terms with retailers based on insights.

Walking on a slippery slope?

Historically, what has kept Pakistan’s digital credit market from growing is the non-existence of sophisticated credit scoring models to improve the quality of credit. Even large commercial banks haven’t made a breakthrough on that front. (Read more about it in Profit’s article: What’s your credit history?)

Jazz, as well as other companies with digital banking ambitions, suffer from the absence of consolidated, reliable data on consumer spending behaviour and detailed payment history. The third-party credit bureaus are also not well equipped to serve them either. The reason is a lack of access to payment, utility, tax and other data points of the population.

"Mobilink Bank leverages Jazz’s largest data hub in the country to better equip itself for customer's credit risk assessment for digital lending. Also, we do have third-party service providers that help us build robust AI models for accurate credit scoring," said Taimoor Farid, Financial Controller & Head of Strategy, Mobilink Bank.

The data points they are leveraging are mainly obtained from three sources; Jazz GSM data, JazzCash account data and customer electronic credit information bureau (eCIB) details. The parameters to assess customer details include the transaction history of an e-wallet as well as average bill/recharge on Jazz sims.

Yet, in-house data is likely to be insufficient to build a robust credit scoring framework. As per Karandaaz’s report, Fintech Ecosystem in Pakistan, published in 2021, “Data-driven credit profiling for the underserved is an opportunity area for consumers and enterprises alike. By using alternative data sources (such as tax payments, mobile phone payments, subscriptions and so on), Fintech can develop credit scoring models for previously unbanked individuals and MSMEs. This enhances access to easy and affordable credit. Credit scoring models have a definitive impact on economic growth and are considered one of the key elements in accelerating inclusion of MSMEs globally.”

Furthermore, industry experts suggest that penalising defaulters with actions like blocking sims will also deter habitual defaulters. In any event, it is unlikely that PTA would allow such actions anytime soon.

However, sources aware of Jazz’s strategy did acknowledge the fact that the existing credit scoring models are not as robust as they are being presented. But the telco is willing to take the risk, backing its high margins to absorb any adverse shocks.

Yet, this is not the only problem. To expand rapidly, JazzCash would need to overcome regulatory constraints. It currently operates under a microfinance licence obtained by Mobilink Microfinance Bank (MMBL). This restricts its lending capabilities when it comes to consumption loans.

Therefore, Jazz has applied for the digital banking licence and is awaiting a response from SBP. The licence, however, has its limitations.

As per the framework introduced by SBP for digital banks, “Aggregate deposits are capped at 25% of the capital for the pilot stage. For the transition stage, aggregate deposit cap would be six times of the capital, progressively increasing to 12 times.”

With a capital base of PKR 2.7 billion and approximately PKR 36 billion of JazzCash deposits, the deposit base was close to 13 times the share capital as of 31st December 2021, which means the company is already in breach of the threshold and the figure is likely to skew further given Jazz’s rapid expansion plans.

As far as competition is concerned, Jazz is likely to get a run for its money from the dozens of fintech startups that have emerged over the past few years. JazzCash certainly has the financial might in the form of a cash-rich sponsor but the value proposition of the fintech startups such as Nayapay and Sadapay is a promise of elevated customer experience enabled by an extensive technology stack. (Read more about it in Profit’s article: How good is the bank in your hand?)

A senior official associated with the JazzCash project, responding to Proft’s question about the chances of the expansion not materialising, stated, “Failure is a word unknown to us.” The gentleman is likely to have forgotten the debacle Jazz super app “VEON” was.

Similarly, this project is also built on a combination of ambition and practicality and to avoid the fate of the VEON app, Jazz would need to be inclined more towards practicality than ambition.

The author works as an Editorial Consultant at Profit and can be reached at [email protected]

View all articles →166 Comments

No comments yet. Be the first to join the discussion!