Walk into any money changer in Karachi or Lahore and you will undoubtedly witness the same things. A few tellers will be busy counting cash and sitting in front of windows with the rates for major currencies displayed somewhere – either on a digital ticker display or shabily written on a white board. And the one currency always displayed is the US dollar.

In principle that should be the extent of it. If you want to go buy dollars for example, all you need to do is walk into the closest money changer, give them cash in the Pakistani rupee, and ask for the greenback in return depending on that day’s exchange rate. However, often what you will find instead is the tellers offering rates for the greenback much higher than the official rates displayed on the boards.

The difference between the rate of the dollar on the interbank market and the open market in Pakistan is telling of many things. For starters, the hike in the price of the dollar the entire month of December tells us that despite the government and central bank’s full efforts, currency devaluation was happening as a result of economic and political uncertainty. That uncertainty in turn leads to people trying to buy dollars to secure their savings because the rupee does not feel reliable in trying times. This has been something that has happened in Pakistan before – uncertainty leads to people trying to buy dollars which in turn leads the dollars to go short from the market and the price of the dollar in the open market being significantly higher than the dollar rate in the interbank market.

To confirm these suspicions, your correspondent visited multiple money changers in Karachi. What quickly became apparent was that as far as small quantities were concerned, around less than $500, most of the money changers were selling them without hassle at the rates quoted on the board. Some were charging a premium of up to Rs 3 and were willing to negotiate. For larger amounts, however, it was a little trickier and more expensive. Matters were no different in Lahore and Islamabad, where people looking to buy the dollar have complained to Profit about money changers charging an exorbitant premium even on small amounts of the dollar. One such buyer informed me that the best rate they could find for a mere $450 purchase was Rs186 on a day when the dollar selling rate was not even Rs179.

The practice of money changers selling currency at a higher rate than it is actually worth is a common one. However, the practice increases around December because of the holiday season, and becomes particularly bad because there is a high demand for the greenback during this time of the year. This year, it was worse because Pakistan was going through negotiations to continue its programme with the International Monetary Fund, and with there being political as well as economic uncertainty, it seemed that the country was headed towards dollarization at least on the savings front. But as the speculation settles and the rupee seems to be making a minor comeback at the twilight of the new year’s eve, it is worth looking at how Pakistan faced dollarization in the last few months of the year.

Dollarization and availability

Dollarization is the term for when the U.S. dollar is used in addition to or instead of the domestic currency of another country. It is an example of currency substitution. Dollarization usually happens when a country’s own currency loses its usefulness as a medium of exchange, due to hyperinflation or instability. This happens most starkly in countries where the local currency has completely collapsed, like in Zimbabwe or in Venezuela, where devaluation has gotten to a point where it is just simpler to trade in the US dollar.

However, since the supply of these dollars is low, acquiring them can be difficult and expensive. In Pakistan, we are not close to a point where the US dollar will be used as legal tender. However, while we haven’t started using the USD as a medium of exchange, for savings more and more people are turning to the greenback to protect themselves from the depreciation of the rupee.

In Pakistan, because of its constant uptick in value, the US dollar is considered the currency of investment and savings. While this savings strategy can be debated, this does show a trend of finding solace in the dollar and treating it as a safe haven investment amidst uncertainty and inflation.

“I try to save as much as I can in dollars,” said one young professional in one of the lines at the money changers. These days, the lines are typically long and moving at a snail’s pace, because instead of customers simply going up and trading currency, they are haggling with the tellers over the markup they are charging. However, the desire to buy the US dollar as a saving tool has not been affected by this. “Keeping inflation into account, the riskiness of the stock market, the fact that I don’t want to pay interest and don’t want to pay tax on my savings, I’d rather just keep them in physical notes at home,” said the person in the line.

This means finding and buying is a tough task – and the rates thus keep rising even if off the books. And when people are investing, sometimes the amounts they want to buy are high. The government has introduced limits and barriers to buying the dollar freely, such as requiring biometric verification along with CNIC for anyone buying more than $500, and an overall limit of $10,000.

However, the general sentiment at money changers when asked about how to get around these measures is that “sab hojaye ga.” There are easy workarounds to the SBP rules recently put into place to curb the dollarization, especially in light of hawala hundi rebounding as travel eases.

The rupee is stable

Despite all of this in addition to international pressure, the rupee has been as stable as can be expected against depreciation as of late. This is often attributed to the current account deficit numbers clocking in lower than usual and the various means by which the SBP is trying to slow down the dollarization of Pakistan.

However, uncertainty regarding the IMF program has in the past caused the rupee to weaken. We don’t really see that happening right now. On October 26 2021, for example, the rupee shed Rs 2.80 against the dollar over confusion regarding the resumption of the IMF program.

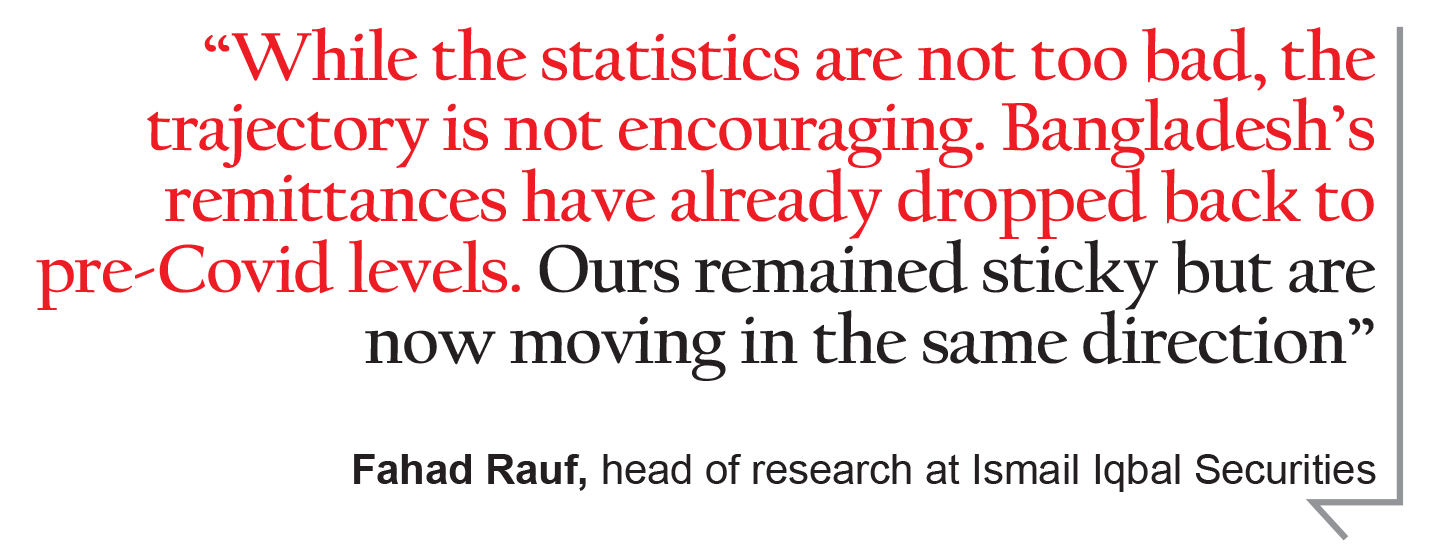

If we look at the remittances front, that too has not been very promising. Remittance by overseas Pakistanis registered a meager 1 per cent year-on-year (YoY) growth, clocking in at $2.4 billion in November FY22 compared with $2.3bn during November FY21. All of this despite the federal government swooning as they wax and wane poetic in praise of overseas Pakistanis and their contributions to the economy.

On a month-on-month (MoM) basis, remittances declined by 7pc, whereas a growth of 10pc was registered for the current fiscal year clocking in at $11.76bn. “Clear signs that opening of travel restrictions are affecting official remittance,” Topline Securities CEO Mohammad Sohail said. “While the statistics are not too bad, the trajectory is not encouraging. Bangladesh’s remittances have already dropped back to pre-Covid levels. Ours remained sticky but are now moving in the same direction,” said Fahad Rauf, head of research at Ismail Iqbal Securities.

Earlier in November, the World Bank released a report titled “Migration and Development Brief” wherein it claimed that remittances are likely to remain flat at the presently high levels in 2022 as the one-off effects of government incentives to attract them fade although the Afghanistan factor will continue to sustain flows. Afghanistan’s fragile economic and political situation emerged as an unexpected prompt of remittance inflows into Pakistan in 2021, the report reads.

“Second factor that comes into play is starting in August. And that is developments related to Afghanistan because they cause additional pressure, especially in the open market. reports that foreign currency cash is being taken in large amounts to Afghanistan. That adds pressure. It also adds some broader concerns and uncertainty on the part of the investor community about geopolitical developments in the country, when there is a desire to move into safe assets. In the local context that is either gold or dollar,” said Governor State Bank of Pakistan while speaking to Profit in an interview.

It is a healthy reminder that political problems like the Afghanistan issue have not just political repercussions for Pakistan, but also a direct impact on the rupee which drives inflation. It also has an impact on the investment climate in Pakistan especially if one is to take into account international sentiment towards the region.

However, the situation with regards to Afghanistan has improved as per sources which is due to the SBP curbs, FIA activeness in the border areas, and better geopolitical dynamics. Talking about the Real Effective Exchange Rate (REER), it has depreciated by 4.1% during the 4MFY22. This means exports have become cheaper in international markets, whereas imports seem more expensive to Pakistanis.

“Over the next few quarters, our base case FX outlook is less pessimistic than initially feared. We expect PKR to be 178/USD by June 2022 and 183/ USD by December 22”, says the Arif Habib Limited Pakistan Investment Strategy 2022 report.

How is the rupee stable?

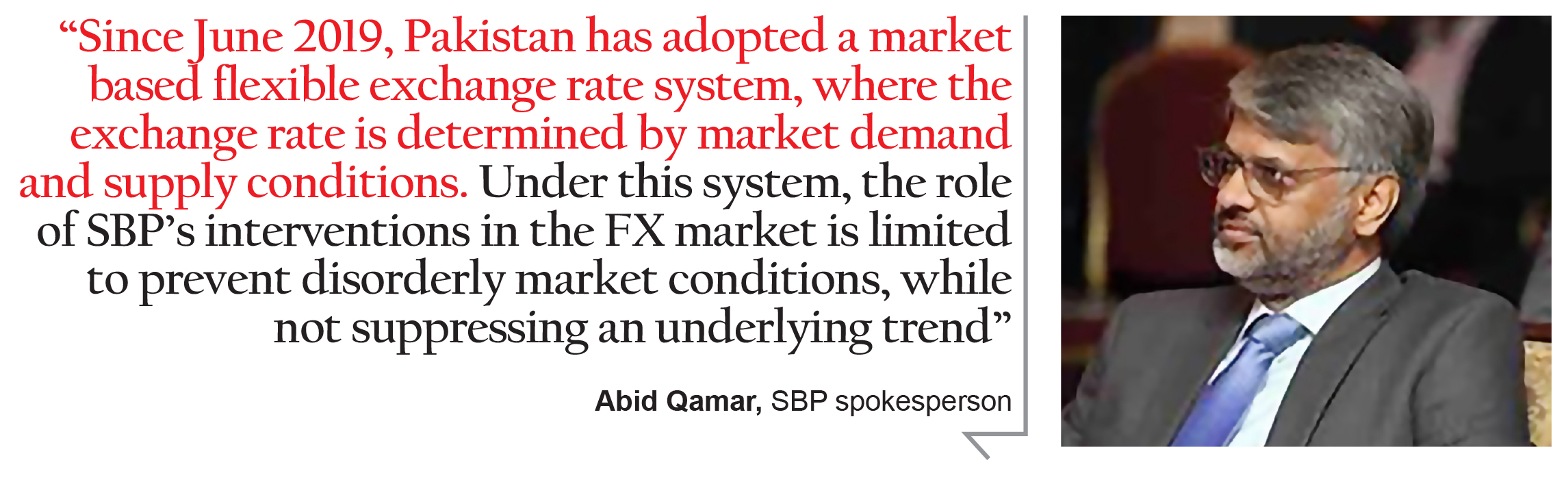

In a major scoop uncovered in September of 2021, Shehbaz Rana of the Express Tribune claimed that the SBP pumped $1.2 billion into the interbank market in three months to defend the weakening rupee. “The SBP does not comment on speculations about market interventions,” said Abid Qamar, Spokesperson at the SBP when Profit asked for a comment in September. That means that official confirmation is not a possibility. Yet there was no official denial of the story either.

“Since June 2019, Pakistan has adopted a market based flexible exchange rate system, where the exchange rate is determined by market demand and supply conditions. Under this system, the role of SBP’s interventions in the FX market is limited to prevent disorderly market conditions, while not suppressing an underlying trend. When the exchange rate does not reflect realistic market conditions it can contribute to unsustainable current account deficits and repeated balance of payments problems,” Qamar added.

How the rupee is controlled – allegedly

Previously when the SBP would intervene in the market, it would do so quietly by making calls to bank treasuries asking them to buy, sell, or hold the rupee at a specified rate. This is different from injecting rupees within the interbank market. That, however, is not the case anymore. As per a source in a leading bank, the process is far more complex. Let’s say Bank A wants to buy an X amount of dollars. When the transaction is put up, the SBP calls the bank and asks them to hold off on the transaction and arranges supplies of dollars at the specified rate. Instead, they offer the bank to buy from a broker to prevent the interbank rate from going up. Bank B pays the broker through money they receive from the SBP. All this effort is designed to keep the intervention silent and maintain the rupee at a level the central bank has determined for it.

“The central bank is actively, aggressively and systematically intervening in the interbank FX market to regulate rupee depreciation as best as it can”, said a senior banker while speaking to Profit. This is interesting because when the SBP makes an intervention by injecting money into the interbank it has to be a temporary transaction. This means that interventions will be temporary and they will maintain a net zero position at the end of each quarter. so whatever they sell to the market, they will purchase back at a later date.

In the case of the SBP arranging the dollar liquidity for the purchasing bank through market mechanisms, it may not have to treat this as a temporary injection. If true, however, we can now understand why currency traders have been seeing more action in light of fears of more depreciation.

A standout amongst other site about turning and energy tasks under goodbye material factories. We are give so numerous data about land and substantially more.

I’d remembered from the small number of scary movies that