The bifurcation of payments

Electronic payments are gaining market share, but cash is not ceding ground either

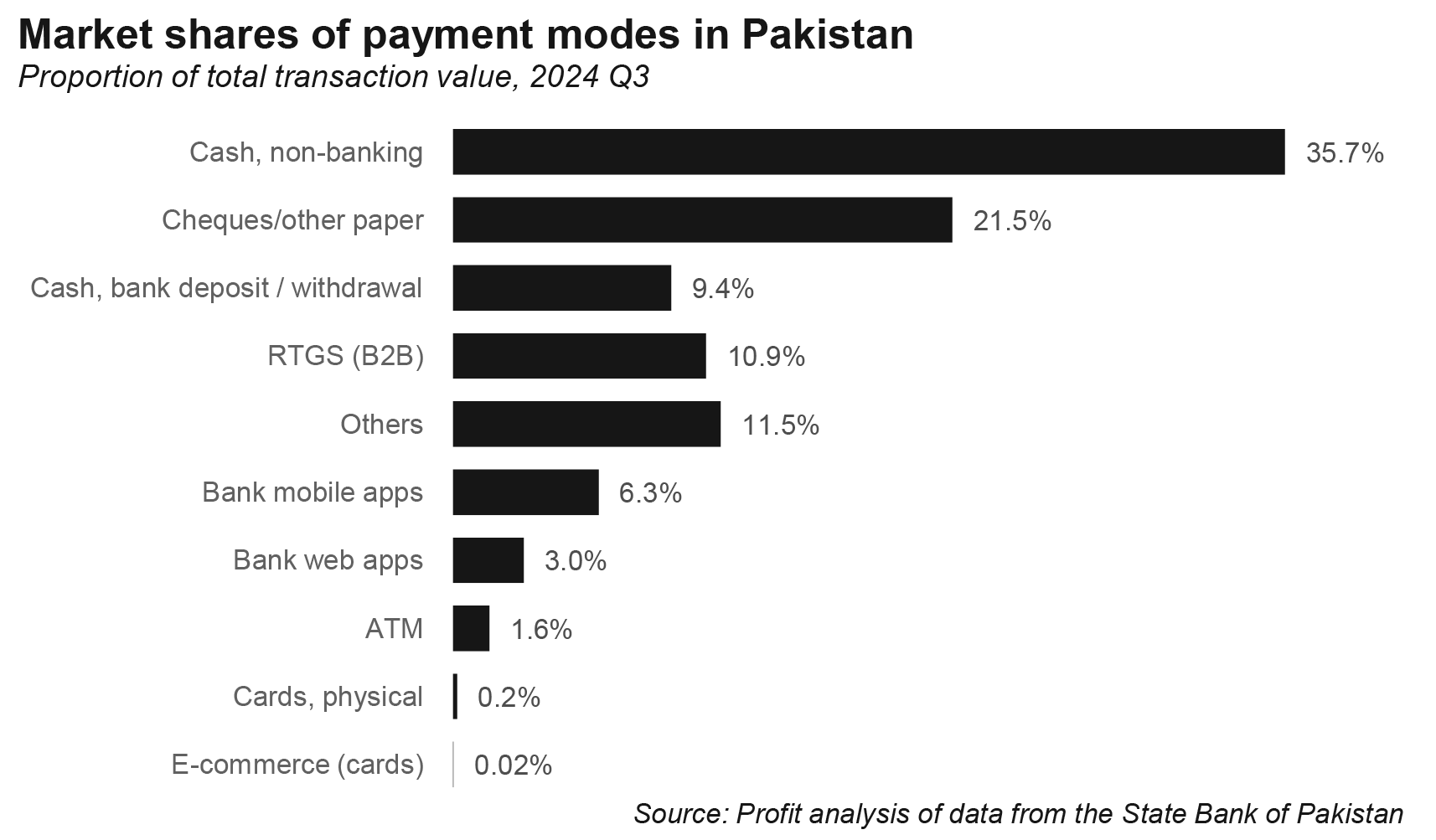

By now, the rise of electronic payments in Pakistan is quite clear and has been covered extensively by many publications, including this magazine. What is less clear is that what should be the implication of the rise of digital payments – that the proportion of payments in Pakistan made in physical cash is going down – has not happened yet, or at least not nearly as much as the rise in digital payments might imply.

During the third quarter of 2024, digital payments – bank apps, websites, and card-based e-commerce payments – have increased to approximately 9.3% of the value of all transactions that take place in Pakistan, up from just 0.3% in the same quarter in 2016, which is a nearly 31x increase in market share for digital payments, according to data from the State Bank of Pakistan.

You would think that cash would have fallen by a corresponding percentage, but you would be wrong. According to Profit’s estimates based on data from the State Bank, the proportion of transactions in Pakistan that took place purely in physical cash (which means excluding cash deposits and withdrawals from bank branches and ATMs), were approximately 35.7% of the value of all transactions that took place during the third quarter of 2024. Eight years ago, in 2016, that number was 38.4%, so cash is down slightly from where it was almost a decade ago.

But not by nearly as much as that rise in digital payments number might have led you to think.

Subscribe to Continue Reading

The rest of this article is available exclusively to subscribers.

Managing Editor, Profit Magazine. He can be reached at [email protected]

View all articles →2 Comments

No comments yet. Be the first to join the discussion!