The fall of Pakistan’s textiles

The problems are well identified. But how did a once proud and strong industry come to its current state?

In 2002, archeologists excavating a neolithic burial site in Mehrgarh Balochistan discovered among the dust and bones of a six-thousand year old grave a few copper beads. Trapped within one of the beads were wispy white strands. Metallurgical analysis proved the suspicions of the archaeologists: the strands were cotton. They had been preserved by a unique occurrence of mineralisation of the copper that had trapped the strands of cotton in place.

The discovery was monumental, and an article published in the Journal of Archeological Science published later that year announced this was the earliest proven existence of spun cotton in any ancient civilization.

The area we know today as Pakistan has been growing, spinning, weaving, wearing, and exporting cotton for thousands of years. By some estimates the Indus Valley civilization introduced cotton and its uses to the ancient world more than three thousand years ago. The arc of history tells us that Pakistan is a textile country. It is a fact written into the genetic code of this nation. Cotton fields from Patoki to Rahim Yar Khan in Punjab and all the way down to Sanghar in Sindh have for thousands of years provided raw materials to the world’s oldest textile producer.

Which is why it was no surprise that, after Partition, textiles emerged as one of the leading industries in Pakistan. Over the decades, it has developed into Pakistan’s largest export oriented sector. In any given year 50-60% of Pakistan’s exports are textiles. Everything from thread, to yarn, as well as bed sheets and jeans are produced, packaged, are made in Pakistan and sold to the world.

But Pakistan’s textile industry is also in the middle of a severe crisis. “There was a time when our organisation had more than 400 members. Today we have fewer than 200 members,” says Kamran Arshad. Mr Arshad’s family has been in the textiles business since the 1980s. They have two spinning and one weaving units by the name of Ghazi Fabrics. For the past year, he has also been serving as chairman of the All Pakistan Textile Mills Association (APTMA) — one of Pakistan’s oldest and most well known lobbying groups.

“This is an industry that provides more than half of our exports, but we’re fighting a losing battle. Our regional competitors like Bangladesh, Vietnam, India, China and others all have cheaper electricity, they have cheaper gas, and lower tax rates compared to us,” he says. “If we had simply been given some consistency in policy from the federal government so many of our members would not have had to shut down their factories and units.”

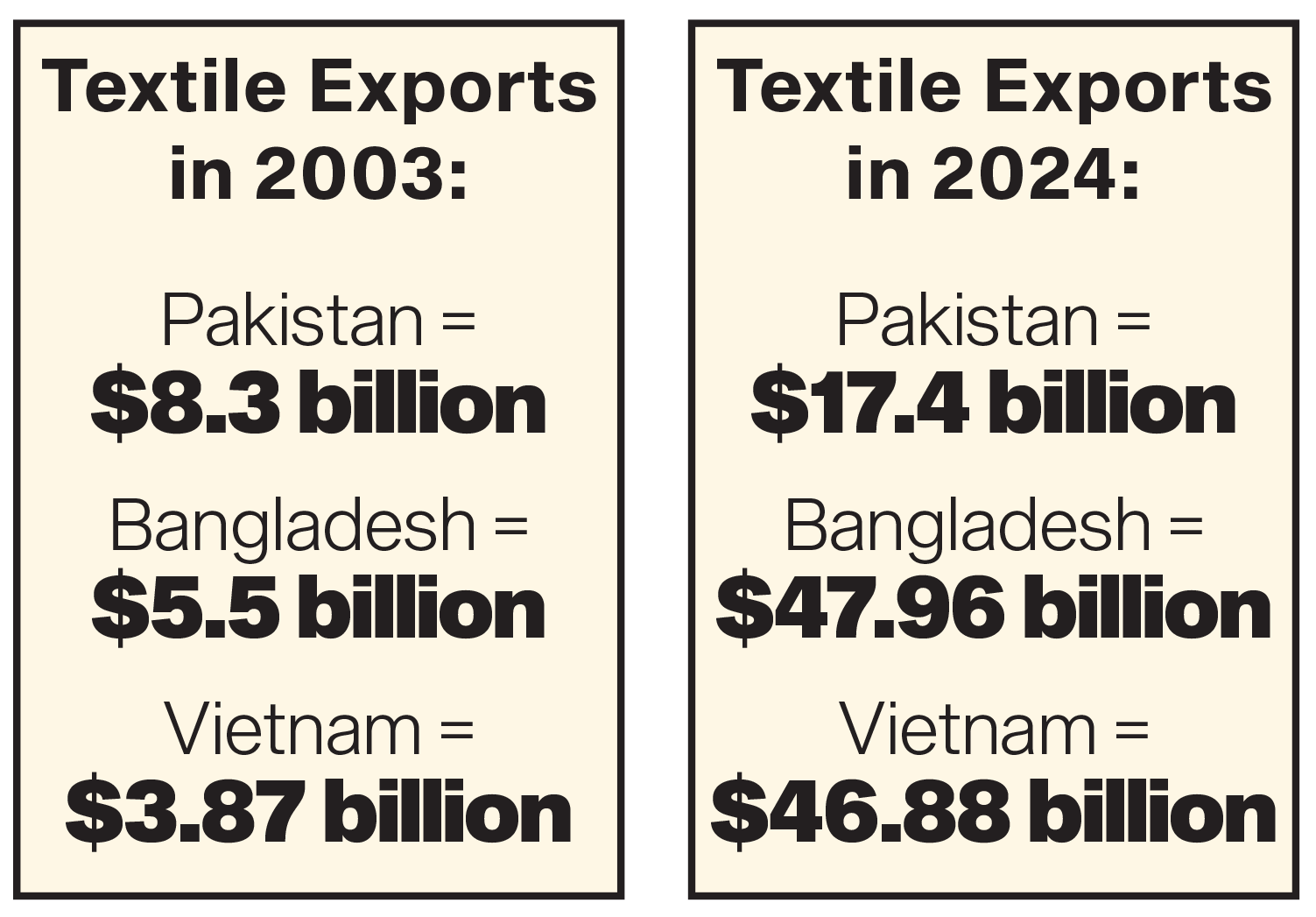

The reservations raised by Mr Arshad are quite familiar. Not only has the textile industry been saying these things for years, but other industries have similar concerns: inconsistency in government policies, fluctuating energy and tax rates have all left them uncompetitive on the global market. In the case of textiles, the impact in the past 20 years has been stark. Here is a sobering statistic: In 2003, when Pakistan’s textile exports were $8.3 billion, Vietnam’s textile exports were $3.87 billion, Bangladesh’s were at $5.5 billion. Now Vietnam is at $46.68 billion and Bangladesh is at $47.96 billion, while Pakistan has failed to cross the $20 billion mark in the past five years.

This downfall has been the result of a combination of factors. By their own measure, stakeholders in the textile industry estimate that they have been slow to move towards value addition and to adopt modern materials such as synthetic fibres. However, they claim further investment in the textile business has been made impossible by fluctuating government policies. Their issues are clear and well documented: shortage of raw materials in the form of domestically grown cotton, the highest energy costs among competitor countries, and taxation measures that have left them crippled with a deadly cash flow crunch.

But what is behind these issues and is there a way out of them? Profit spoke to industrialists, cotton farmers, and textile stakeholders from weavers and spinners to massive retail fashion brands. A combination of their opinions presents a much clearer picture. The historic success of textiles in Pakistan has had to do with a complete value chain that starts in the cotton field, moves towards ginning, is spun into thread, woven into cloth, and then coloured, dyed, knitted into bedsheets, shirts, pants and all manner of other cotton products that can then either be sold locally or exported. All along this value chain there are different problems but they combine to culminate in an industry that has been around for more than 10,000 years, but might be standing on its last legs.

The cotton tale

“There was a time when I could say with great pride that Kapas talks to me. I have conversations with my cotton fields,” says Khalid Khokhar. Middle-aged with grey hair, he talks about cotton with affection you would normally expect to be reserved for people. Mr Khokhar began farming in 1992 and is currently President of the Kissan Ittehad. The first crop he grew was cotton. He claims he could tell just by looking at his crop whether it needed more, pesticide, or fertilizer.

“Now unfortunately I cannot say the same thing. The kapas has turned away from me. It has stopped talking to me. It is upset that he has stopped growing white gold and is instead promoting white poison.”

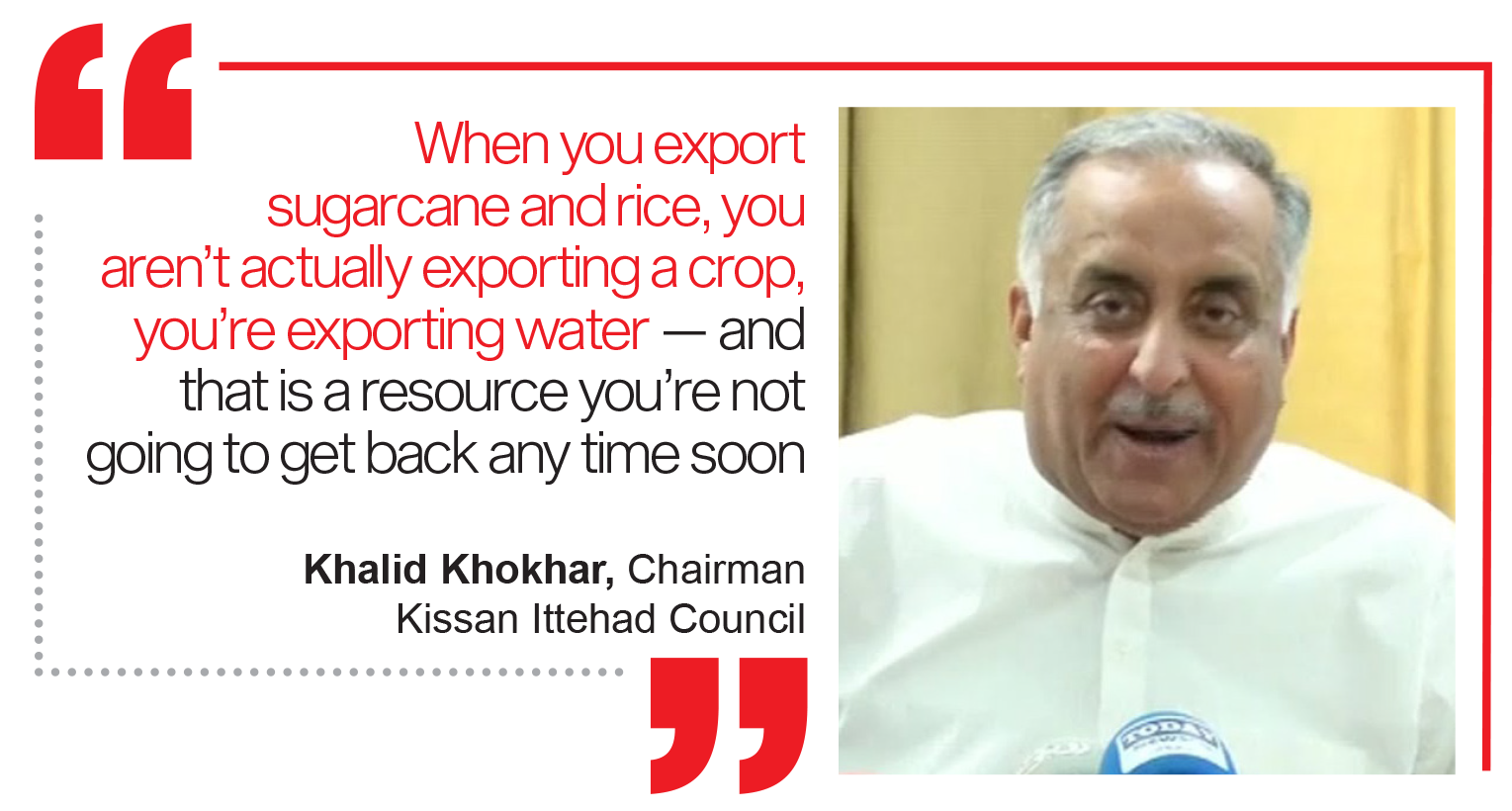

He is referring to the replacement of the cotton crop in large areas of Punjab and Sindh by sugarcane and rice. It is an issue that is deeply critical to Pakistan’s agriculture. Cotton was for the longest time a very safe cash crop, but a lack of investment in seeds and research has meant Pakistan’s cotton is not disease resistant. The loss of the crop year after year has led farmers to plant sugarcane and rice instead. Both of these are water intensive crops, unlike cotton. As Mr Khokhar explains, when you export sugarcane and rice, you are not actually exporting a crop, you are exporting water — and that is a resource you are not going to get back any time soon.

“In 1992, in my hometown in Zilla Khanewal, ground water could be found at 20-24 feet. Today you cannot find ground water at 65-70 feet sometimes. In this entire area sugarcane and rice has taken over. And when you plant sugarcane, it is like you’re planting a tubewell. It sucks water and potash out of the ground which leaves the land completely barren in time,” he says.

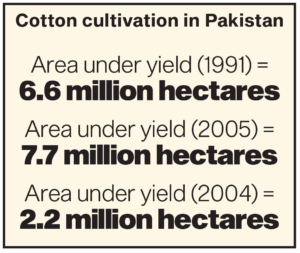

Cotton is the core component that has been holding Pakistan’s textile industry together all these years. Over the past two decades, the cotton crop in Pakistan has fallen out of demand, has become internationally uncompetitive, and output has fallen by a whopping 65% from 14 million bales being produced in 2005 to 5 million bales being produced last year. This is despite the fact that Pakistan has actually decreased the weight of its bales.

Once the darling of farmers and agriculturalists, the area dedicated to cotton farming has also been shrinking significantly since the late 2000s while competitor countries like Egypt have increased the area they are dedicating to growing cotton.

In 1991, cotton was grown on around 6.6 million acres of land all over Pakistan. It grew to a peak area-under-cultivation level of 7.9 million acres in 2005 but stood at a mere 2 million hectares in 2020 showing a serious backwards trend. Changing climatic conditions have made the cotton seed in Pakistan less resistant and more likely to fail — which means growing it has become a bad business decision for a number of agriculturalists.

This decline has had two main factors. For decades, farmers grew cotton because they knew the textile industry would buy the raw materials and they would get a good price. However, there was a shocking lack of research on cotton. No new seed varieties were introduced, at most there were strains that were disease resistant but not disease free. The cotton crop had its issues, but low yields were made up for by higher areas under cultivation because the demand was high. Then came the crisis of 2008. That was the year energy shortages in Pakistan crippled both industrial and domestic consumers with massive power cuts.

The textile industry is energy intensive, and the shortages meant the business was in a massive slump. In a single year, more than 90 mills shut down. The ones that did not wrap up kept their machinery off. Cotton was suddenly not a sure shot crop. In the years to come, farmers shifted away from cotton and the industry began importing cotton, particularly from the Americas, to make up for the shortage.

This combination of factors has led to a decimation of the crop, and serious implications for the textile industry. “The one advantage Pakistan has in its cotton chain is cheap labour, but you need to have a streamlined chain. For us to utilize this advantage, we need to encourage local cotton growth even if it takes supporting farmers for a few years, and we need to give cheap energy to spinners and weavers,” says Kamran Arshad.

And that brings us to the next and possibly biggest problem — energy.

Spinning a web

It is important to understand the process by which textiles are made. Briefly, cotton is grown on farms, picked by farmers either by hand or machine, and then sold to cotton ginning mills. Nearly the entirety of Pakistan’s cotton ginning industry is located in South Punjab. Ginning involves removing the cotton seed from the cotton. It is a labour-intensive, low margin business, so even the owners of cotton gins are not particularly rich people.

That ginned cotton is then bought by textile spinning companies, who use spindles to turn that ginned cotton into cotton yarn. The yarn is then woven into cloth, the cloth is then dyed and printed, and after that comes the stitching phase.

This is, again, a labour intensive part of the process, but it is a bit further up the value chain, so the margins are a little bit better. And here is where a big strategic decision needs to be made by the person who owns a textile factory. See, textile spinning, weaving, and dyeing are big mechanical processes where large machines run by semi-skilled labourers and engineers do most of the work.

After that, your ability to go further up the value chain involves how many people you can have in a factory literally just sitting at a sewing machine and sewing up the items you are trying to manufacture. And the margins you will earn at this stage are determined by one decision: do you want to earn higher margins by having people sew smaller, more complex stitches, or do you accept lower margins, but potentially higher volumes by doing simpler stitches that you can probably churn out faster?

A bedsheet, for example, involves a small number of straight lines that can be stitched very quickly. A pair of jeans, however, involves pockets, zippers, and curved stitches that can be significantly more complex. Your factory would earn a lot more for the jeans, but it will also take longer. The bedsheet could probably be done in seconds by a skilled labourer.

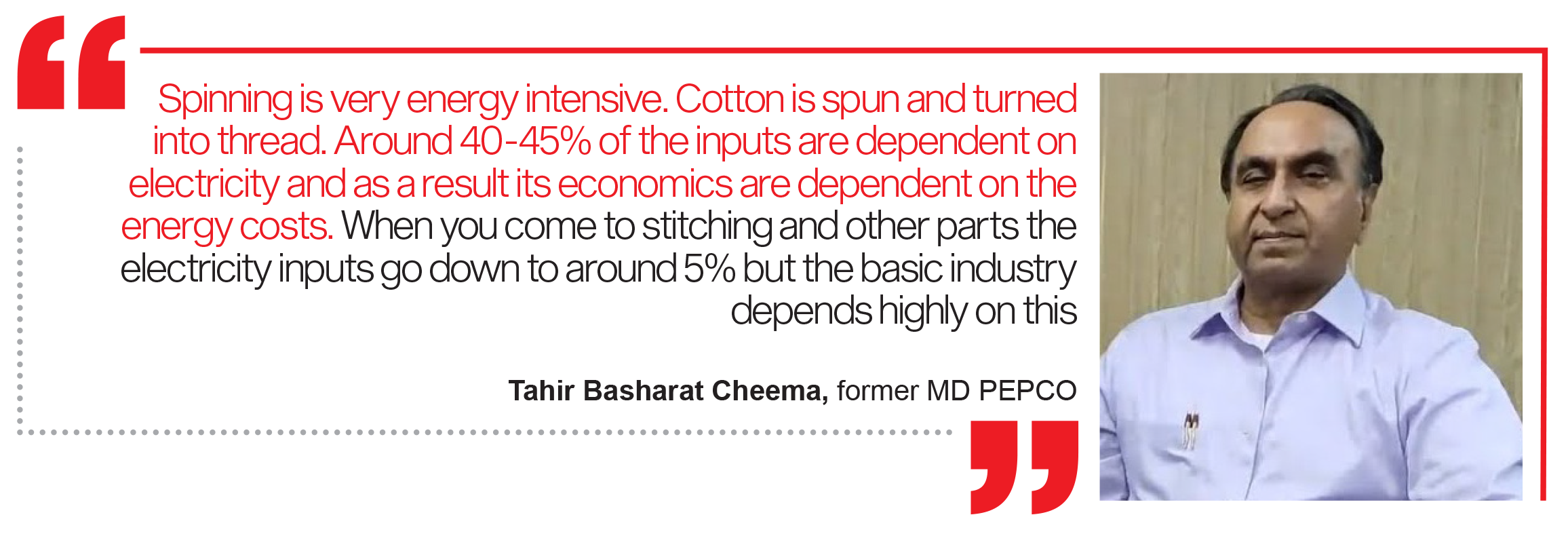

The second part of this chain, spinning and weaving, is where a lot of the cost is added. Since it is done primarily through machines, it is very energy intensive. Energy has been a consistent bane for the industry. “Spinning is very energy intensive. Cotton is spun and turned into thread. Around 40-45% of the inputs are dependent on electricity and as a result its economics are dependent on the energy costs. When you come to stitching and other parts the electricity inputs go down to around 5% but the basic industry depends highly on this. And if it works the rest of the industry will work as well,” explains Tahir Basharat Cheem, an energy advisor to the industry and former managing director of PEPCO.

“The export industry competes with other countries, not other cities or factories. We need to look at comparative economies to see what our advantage is and what our disadvantage is. We compete with India, Bangladesh, Sri Lanka, Thailand, Vietnam, and China. If electricity rates there are low, then naturally the industry here will be at a disadvantage. We cannot export at those rates. We need to digest those. At these rates we are not competitive at all. At most the prices are 6-9 cents per unit of electricity. In Pakistan we are getting electric at around 12.5 cents per unit. And the entire chain needs to move along to get the downstream benefits.”

The history of how this happened is long and unfortunate, and has to do with how Pakistan’s energy management system has been run since the 1980s. From the 1950s onwards, Pakistan had most of its electricity generated through hydroelectric energy stored in Mangla and Tarbela dams. But as demands grew in the 1980s and water shortages became regular, in the 1980s, the government began setting up oil-fired power plants, but the vast majority of Pakistan’s electricity came from water until at least the early 1990s.

At that point, with international financing difficult to procure owing to Pakistan’s poor relations with the United States, the government instituted a policy that allowed for more private sector players to set up independent power plants (IPPs) that were reliant mainly on oil. Over the next decade, this increased Pakistan’s reliance on imported oil as a fuel for its electricity generation.

In the early 2000s, the Musharraf Administration decided to convert at least some of that thermal power generation capacity from imported oil to domestic natural gas, under the assumption that Pakistan had abundant domestic reserves. This, as has been pointed out in this publication on many previous occasions, was a very faulty assumption.

As of 2005, the height of the Musharraf-era economic boom, Pakistan derived more than 84% of its electricity generation from entirely domestic fuel sources, according to Profit’s analysis of data from the National Electric Power Regulatory Authority (NEPRA). That meant that even as the Iraq War of 2003 drove up global oil prices, Pakistani consumers of electricity remained largely unaffected.

Unfortunately, there was a limit to just how much natural gas was available in Pakistan and around the end of the Musharraf years, Pakistan went from being a gas-surplus country to having a shortage. That shortage, in turn, meant that the thermal power plants that could run on either natural gas or furnace oil ended up having to run on oil almost all of the time as the government scrambled – and failed – to keep the lights on.

The sharp rise in reliance on oil coincided with a dramatic rise in oil prices themselves (late 2007 and again in early 2009). Oh, and the rupee’s value collapsed at the same time, which created a perfect storm for the incoming Pakistan Peoples Party (PPP) led government, which tried to keep consumers insulated by increasing government subsidies, but the government did not have the money to do so.

What happened after this is a sordid tale that has led us to our current woes. The relevant part to our story is that Pakistan’s energy mix today is majority dominated by imports. For an energy intensive industry like spinning and weaving, that makes it very expensive. On top of this, the government also has tariffs and cesses on energy that make it more expensive compared to energy in other countries. Not only this, the government has also shown stubbornness when it comes to renewables. For example, the government only offers solar net metering to commercial customers for 1MW, even though the industry wants to expand their solar capacities.

“We have some serious legacy costs here. The government was told the private sector needed to be brought into the electricity generation. This was the birth of the IPPs. However, there was no regulatory control on them nor any legal controls. They get very high rates. Because we were always considering them in US cents and dollars, our currency devaluation also was a big blow. It has gone from Rs105 to over Rs300 in recent years. If the currency falls this much, that cent which was Rs6 has become Rs18-20. Perhaps not a lot of attention was given to this at the time. Similarly, we were not able to use indigenous fuel sources at the time. So not only are we import reliant, the cost is also increasing because of currency devaluation. Similarly even with RLNG the prices were pegged to the price of oil. Customer categories have also been a big issue. We have not been able to deal with these legacy costs,” says Mr Cheema.

Energy is by far the biggest problem Pakistan’s textile industry faces. It has meant costs have increased, and with fast changing government policies, the industry claims it is impossible to keep up. “As long as our policy makers do not give prolonged policy framework industrialisation will not happen. As long as they keep focusing on T Bills the environment for growth just won’t develop. We don’t know what our rate of taxation, energy, gas or anything else will be. When we have this uncertainty, the boom times will be less and bust periods will keep getting longer,” says Kamran Arshad, Chairman of APTMA.

The heat has been felt by everyone including large players that have been in the industry for a very long time. Adil Bashir is the third generation of his family that has been involved in the textile industry. He currently runs Suraj Textile Mills, but he is also troubled by the massive electricity costs. “Spinning yarn and fabric is the most energy intensive. We have to measure conversion costs. My biggest cost around 30-35% is utilities. Today we are almost touching 60%. If my input cost of utilities whether it is WAPDA or gas has gone up and almost doubled how does the govt expect us to survive. Mills are closing, especially the upstream and in the world there is a glut,” he says. “That is why we have fallen behind.”

Taxes, taxes, taxes!

In addition to skyrocketing energy prices, Pakistan’s textile industry faces an oppressive tax regime that exacerbates its challenges. Exporters in the textile sector are subjected to a range of taxes that make it increasingly difficult to remain competitive. The dual taxation system—where exporters are taxed both under the normal income tax regime and a fixed tax on export proceeds—has created a heavy financial burden for textile manufacturers. The effective tax rate for exporters can reach as high as 135% of profits, undermining the profitability of textile exports and making it more attractive for businesses to focus on domestic markets instead.

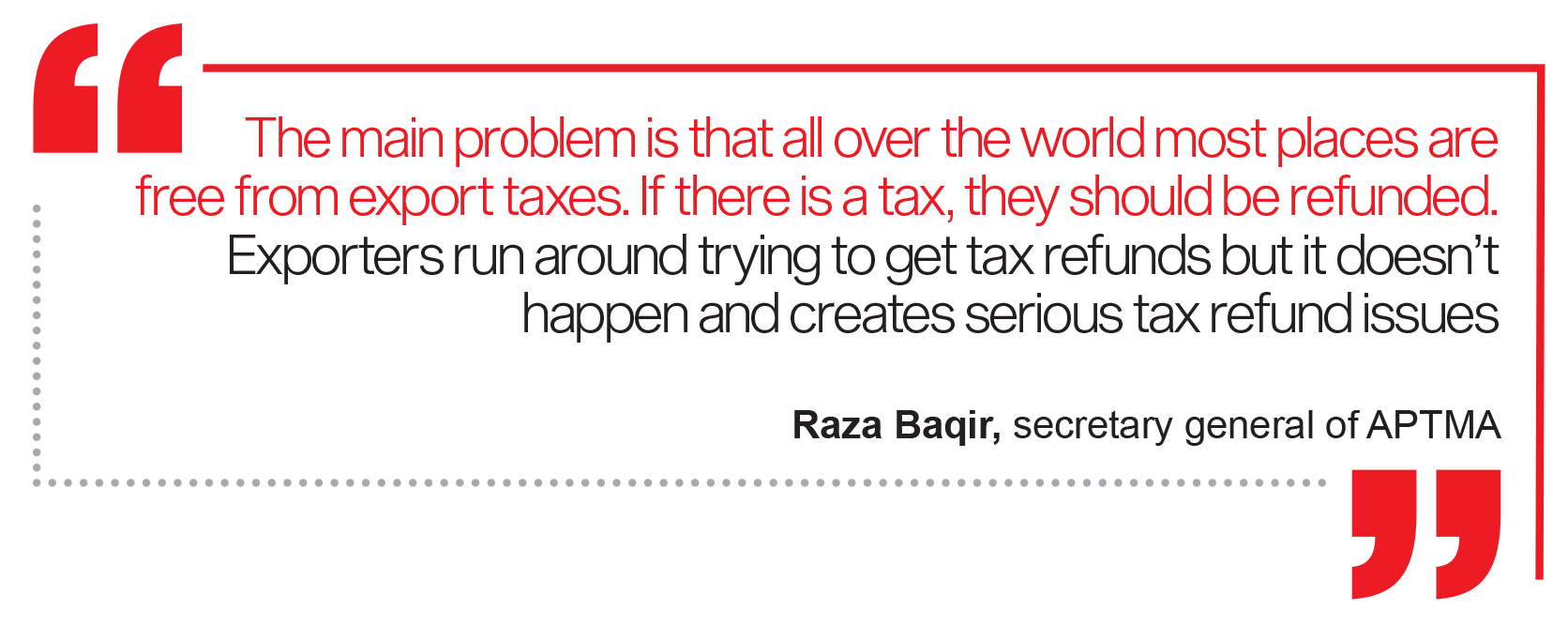

“Pakistan’s biggest issue is tax collection compared to our GDP. Our ratio does not go over 10%. There are ways to expand the take base. We have unfortunately taken the easier way of squeezing those already in the tax base,” explains Raza Baqir, a former member of FBR and Secretary General of APTMA.

“The main problem is that all over the world most places are free from export taxes. If there is a tax, they should be refunded. Exporters run around trying to get tax refunds but it doesn’t happen and creates serious tax refund issues.”

The imposition of new taxes, such as the recent re-imposition of electricity duties by the Punjab government, has only added to the industry’s woes. These taxes increase operational costs for manufacturers, further eroding their ability to compete in the global market. Many other countries have adopted tax policies that incentivize export growth, offering tax breaks, rebates, and other support measures to bolster the competitiveness of their textile sectors. Pakistan, on the other hand, seems to have adopted a more punitive approach, which disincentivizes expansion and investment in the textile sector.

“No one believes in giving rise to industry. No one in the government. That is the most frustrating part of dealing with the government. Our members are losing interest. No other industry is as affected by core issues such as interest rate. Taxation, and energy as us. We are directly impacted by this deadly trifecta,” says Kamra Arshad.

The lack of consistency in tax policies only adds to the instability. Exporters face the constant threat of new taxes or changes to existing tax structures, making it difficult to plan for the future. This uncertainty, combined with high taxes, has made Pakistan’s textile industry less competitive compared to other nations, which have more stable and supportive tax environments for exporters.

Retail woes

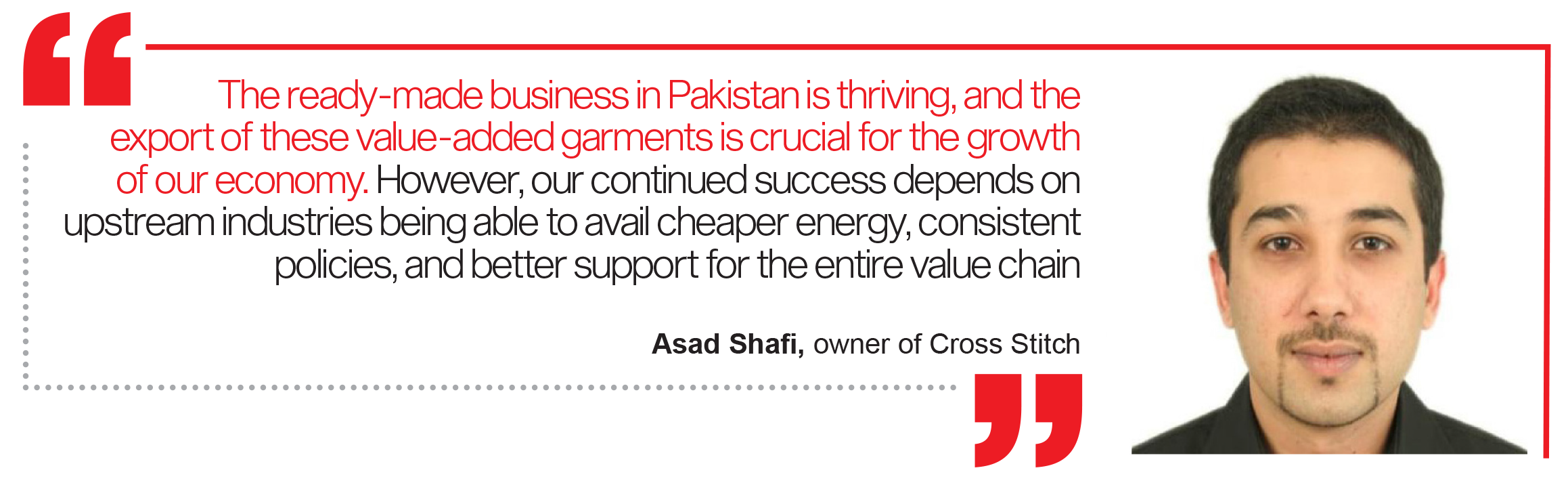

The issue of taxation goes beyond just the export industry. Asad Shafi, a third-generation textile businessman, is the proud owner of Cross Stitch, a leading fashion retail brand in Pakistan. His company, which specializes in ready-made garments, has successfully captured the domestic market while also exporting its products to international markets. Shafi sees immense potential for Pakistan's textile industry to thrive in the ready-made garments (RMG) sector, with value-added products like apparel having a substantial market abroad. However, Shafi is quick to point out that the current challenges facing the domestic textile industry must be addressed before the potential for growth can be fully realized.

“The ready-made business in Pakistan is thriving, and the export of these value-added garments is crucial for the growth of our economy,” says Shafi. “However, our continued success depends on upstream industries being able to avail cheaper energy, consistent policies, and better support for the entire value chain.” The government’s lack of stability in policies, particularly regarding energy prices, is a major concern for businesses like Cross Stitch, which relies on a well-functioning, competitive supply chain to thrive both locally and internationally.

Yet, the problems do not end at the energy costs or the upstream sector. Shafi is particularly concerned about the taxation system, which, in his view, severely hampers the growth of the industry, especially for registered businesses. “In Pakistan, small-scale retailers often operate cash-based businesses and evade taxes. This puts companies like Cross Stitch, which are fully registered, at a disadvantage. We are paying high taxes while these smaller players avoid the burden. This creates an uneven playing field that harms legitimate businesses and discourages investment,” he explains. Shafi believes that Pakistan’s fashion retail sector could grow exponentially if the government provides a more consistent and supportive taxation system that levels the playing field.

The discrepancy between small, informal retailers and large, formal ones like Cross Stitch is evident in the business landscape. Small players often operate on margins that are not subject to the same regulations, allowing them to thrive in ways that larger companies simply cannot. The lack of enforcement of tax laws for informal businesses creates an additional layer of complexity for large textile retailers. Shafi argues that the government must prioritize formalizing the sector and ensuring that every player contributes fairly to the economy. “This disparity in tax compliance is not only frustrating for businesses like ours, but it also impedes the overall growth of the industry,” he states.

Despite these challenges, Shafi remains optimistic about the future of Pakistan’s textile sector. He highlights the growing demand for Pakistani garments abroad, which could be the key to unlocking the sector’s full potential. “If we can overcome the issues in the upstream sector, streamline our supply chains, and create a stable taxation environment, Pakistan can become a powerhouse in the global ready-made garment market,” he says. Cross Stitch, with its focus on high-quality production and design, is already making its mark internationally, but Shafi believes that more support from the government is necessary to enable others to follow suit.

The growth of Pakistan's textile sector is not just about increasing exports; it’s also about empowering domestic retailers to compete on an equal footing. To do so, the country needs to address the deep-rooted issues of taxation, energy costs, and policy instability. Asad Shafi’s insights underscore a crucial point: the textile industry can thrive, but only if the right measures are put in place to support all segments of the value chain, from cotton farming to ready-made garment manufacturing.

The textile industry in Pakistan is at a crossroads. On one hand, it has the potential to reclaim its historical dominance as a global textile producer and exporter, particularly in value-added products like ready-made garments. On the other hand, the industry is grappling with numerous challenges that are stifling its growth. The lack of consistency in government policies, energy shortages, and the taxation disparities between formal and informal businesses all contribute to the current crisis. However, as highlighted by industry leaders like Asad Shafi and Kamran Arshad, there is still some hope if the government and other stakeholders can come together to fix each stage of the problems in what was once a robust chain.

This story is the first in a two-part feature focusing on Pakistan’s textile industry. With unprecedented access and interviews across the entire textile supply chain from cotton field to foreign markets, the first part has focused on what the core issues of Pakistan’s biggest export-oriented sector have been. To understand what can be done about this, read the second part in next week’s issue.

Abdullah Niazi is senior editor at Profit. He can be reached at [email protected]

View all articles →2 Comments

No comments yet. Be the first to join the discussion!