Dear control-freak seth, welcome to the stock exchange

By introducing the dual-class shareholding structures, the Pakistan Stock Exchange – and the SECP – are hoping to attract the listing of companies whose owners want to retain tight control but do not mind sharing profits

After decades of being considered, it is finally here. Dual class shares are being allowed for publicly listed companies on the Pakistan Stock Exchange, and Mughal Steel has decided to jump into the fray by announcing the existing of what they are calling “Class C” shares, which will not be tradeable, not eligible for dividends or bonuses, but will have 50 times the voting power of ordinary shares listed on the exchange.

Needless to say, this move is expected to be highly controversial, and many people – especially the handful of advocates for the rights of minority shareholders – are likely to be deeply upset by this development.

So why is the Securities and Exchange Commission of Pakistan (SECP) even allowing such a thing to exist, whose explicit purpose is to reduce the power of minority shareholders and give insiders even more control over the companies they run?

Because there is more to dual class shares than meets the eye, and while it certainly has its downsides, it has benefits which the regulator is likely keen to see realized.

In this story, we will examine what dual class shareholding is and what its benefits and downsides might be, how it is done in other parts of the world, and then finally how it applies to the case of Mughal Steel.

What is dual class shareholding?

Consider the position of the Pakistani seth. After spending years of toiling and building up their business, in the naysaying culture of Pakistan that does not exactly encourage entrepreneurship, they want to make sure that they control every aspect. The seed that they nurtured and cared for has grown into a flourishing tree and they want to make sure they get to enjoy the fruits that they bear. In the case of companies that have managed to stay documented, they have even gone to the trouble of following all the rules while being treated like a criminal by the government at every turn.

But what happens when they want to get additional funds and capital to keep growing their business further. Either they have to head to the bank and ask for a loan – which Pakistani banks do not like giving to them unless they already have collateral worth much more than what they want to borrow – or they can go to the capital markets to raise the necessary funds. Once the banks have been maxed out (which does not take very long), the only option they have left is to head to the stock exchange and issue shares of their business.

For many, the issue is not even about sharing profits. Investors who have invested in the business should get to share in the profits that are being earned and Pakistani business owners are no different from business owners all over the world in understanding that concept. The one thing that sticks in the seth’s craw is the fact that they have to give over some of the control over to these shareholders.

Shareholders get two things when they invest their money into a company. Firstly, they have a claim to a share of the company’s profits, particularly when they are paid out in the form of dividends. The second right, not one many retail investors often think about, is that they get to vote on important matters brought up before a vote of shareholders (including how much to pay out in dividends, and who to hire as CEO, being two of the most important). It is this voting on important decisions that can sometimes result in acrimony between the founding family and their minority shareholders.

With a dual class shareholding, there is no change to the claim investors have to the profits of the company, especially not to dividends and bonus shares. There are usually substantial changes to the voting rights, however. More specifically, a separate class of shares is created which carries more votes per share compared to ordinary shares.

In the case of Pakistan, there are other considerations, particularly some regulations that have tried to increase the number of shares available for trading for each company listed on the stock exchange.

In order to get listed on the Pakistan Stock Exchange, the minimum initial public offering is expected to offer up 10% of the shares of a company to the public. The exchange then requires companies to increase their floated shares to at least 25% over time. Section 5.4 of the PSX Rulebook states that in case the offering is up to Rs2.5 billion, the listing company should initially offer 10% of the share capital and then increase it to 25% in a span of three years.

That 25% number is particularly important because under Pakistani corporate law, a 75% majority is required to appoint the CEO, which, as Asad Umar used to say when he was the CEO of Engro, is the single most important decision the shareholders can make. If a company floats 25% of its shares to minority shareholders, it needs absolute unanimity among the founders or family shareholders in order to ensure that they retain control over the decision to have their own CEO. For this reason, the 25% plus one threshold is called “negative control”, meaning that it gives minority shareholders a veto on an unacceptable CEO if all of them band together.

The giving away of power and control is a big reason many companies choose to stay private. The two others are a desire not to share information about the company, and a desire not to share the profits. The exchange can do nothing about the latter two: after all, that is the very point of being listed. But they are betting that many Pakistani companies do not mind sharing information and profits, as long as they get to keep complete control, and that the founding family can never be ousted from controlling their company.

That is why the dual class shareholding is likely being allowed by the exchange, with the blessing of the regulator.

Dual class shares around the world

This may be a new concept in Pakistan, but how does the rest of the world handle it? Broadly speaking, the world’s markets are divided into three camps:

- Allowed completely: United States, Sweden, and the Netherlands

- Allowed with restrictions: Singapore, Hong Kong, Canada, India, and China

- Banned completely: United Kingdom, Australia, most of Europe and Latin America

Needless to say, there is far from a consensus on how to approach this matter, and different countries have arrived at very different conclusions on what is the most appropriate set of rules. Based on what the SECP and PSX appear to be allowing, Pakistan’s approach appears to be somewhat similar to the United States than the other two approaches.

Since the United States accounts for more than 45% of the total market capitalization of all stock markets in the world, and is generally considered the most sophisticated of the world’s capital markets, it may be pertinent to ask: how are things done in that market?

In the US, dual class structures are becoming more common, especially among technology and media companies. They allow founders and insiders to maintain control with a minority economic stake. About 7% of the Russell 3000 – an index of the 3,000 largest publicly listed companies in the United States – have some form of dual class shareholding structure.

Even in that market, however, they are not without controversy, with critics arguing they reduce accountability to shareholders. Proponents say they allow long-term focus and protect from short-term market pressures.

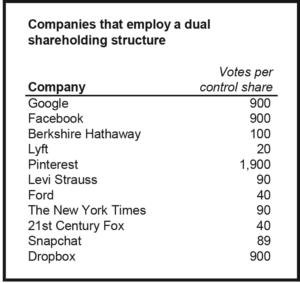

Many of the most famous companies in the world employ a dual class shareholding structure, including Google, Facebook, Berkshire Hathaway, Levi Strauss, The New York Times Company, and Ford Motor Company. Equally famously, however, many companies do not, such as Tesla, Amazon, and Microsoft. In the case of Microsoft, Bill Gates has publicly stated that he was opposed to the idea of a dual class shareholding that would have given him more power over the company.

The Mughal Steel transaction

Mughal Steel is creating a separate class of shares that would give its founding family significantly more control over the company. They are creating a set of Class C shares that will have 50 votes per share, and issuing 50 million total shares, which would give these shares 2.5 billion votes. The company only has about 336 million ordinary shares, so these Class C shares would exercise 88% of the votes in any shareholder vote, and hence have complete control over all matters in the company.

It appears that this new class of shares being created is not being exempted from the requirement of being offered to all shareholders, which means that the sponsors of Mughal Steel have had to come up with a way to ensure that outsiders will not want to buy these shares: Class C shares will not receive any profits or dividends from the company.

Since the shares are not eligible to receive dividends, they are being issued at a substantial discount to the current market price per share of the stock, which closed at Rs70.51 per share at the close of trading on the Pakistan Stock Exchange on Friday. The Class C shares are being offered for Rs30 per share to the controlling family (technically to everyone, but likely only the sponsors will be bidding for them).

At that price, the sponsors will pay Rs1.5 billion to acquire 88% of the control of a company valued by the market at Rs23.7 billion as of the close of trading on Friday.

What is somewhat perplexing is that the Mughal Steel sponsors do not appear to need much by way of additional control. Between their direct family holdings and those they own through other companies in which they have controlling stakes, the sponsors control about 75.4% of the company already.

But perhaps 75% of the votes – and full control over the board and CEO hiring decisions – is not enough for the sponsors. After the issuance of the Class C shares, minority shareholders will have 24.6% of the shares but just 3% of the votes at annual general meetings and any extraordinary shareholder meetings.

The official use of proceeds is to finance the working capital of the company, which effectively means there is no specific use in mind other than the cash being made available for the day-to-day operations of the company. There appear to be no growth or expansion plans being funded by these funds, based on the draft offering document released by the company.

The company does have approximately Rs28 billion in short-term debt, though the bulk of that debt appears to go into financing the company carrying about four months of inventory on its balance sheet.

The Mughal story

Mughal Steel itself is a company that has a long history, having been founded in 1950 as a steel trading company (unincorporated for most of its early existence) called Mughal Traders. It is currently the largest manufacturer of long rolled iron and steel products in Pakistan.

Through the years, that sole proprietorship kept on growing and becoming more and more formalized, providing some evidence for the hypothesis that the Pakistani informal economy will automatically formalize when the barriers to growth start getting removed.

In 1994, a steel production unit called Al-Bashir Steel Industries (Pvt) Ltd was established on the outskirts of Lahore. The company installed a melting unit along with medium section re-rolling mills to produce residential and structural sections like I-beams, H-beams, C-sections, L-sections etc.

In 1998, Mughal Steel – by then a partnership – was established. In 1999, Mughal Steel imported and established two induction furnaces. In the same year an Argon Oxygen Decarboriser (“AOD”) was installed along with ladle refining furnace reaching a complete melting, refining alloying cycle. AOD was the first of its kind in Pakistan, capable of producing stainless steel of high quality.

In 2003, a stainless steel sheet rolling mill was added to the previously established Mughal Steel. The new production unit resulted in increased product line and efficiency. To compliment several production units and ensure quality standard Mughal Labs (“ML”) was established. ML is equipped with chemical and mechanical analytics machines as well as an optical emission spectrometer.

In 2006, foreseeing the rising demand of electricity, Mughal Steel set up a 9.3 MW captive power plant. In 2007, Mughal Ferros was established. The project was aimed at utilizing existing deposit of manganese and chromites in Pakistan for the formation of alloys such as ferro manganese and ferro chrome. It is used for reducing metals from their oxides as well as for deoxidizing steel and other ferrous alloys.

In 2008, Mughal Steel took over the plant and machinery of Al-Bashir Steel and installed two additional mini sectional mills.

By 2010, the company formally converted from a partnership to a private limited company. In the same year, the company installed a bar re-rolling mill with capacity of 150,000 metric tons per year.

By 2015, the company – which had started off as an unincorporated sole proprietorship 65 years prior – converted to a public limited company in preparation for its initial public offering on the Karachi Stock Exchange, raising just shy of Rs700 million.

Where the company stands today

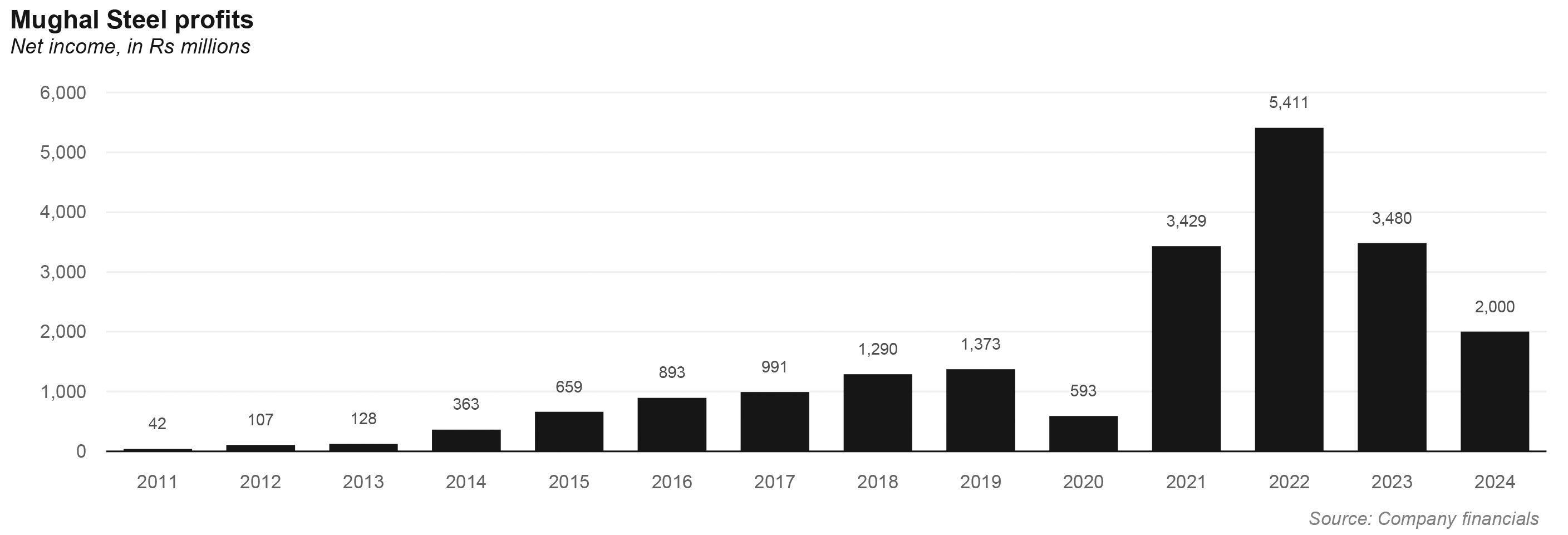

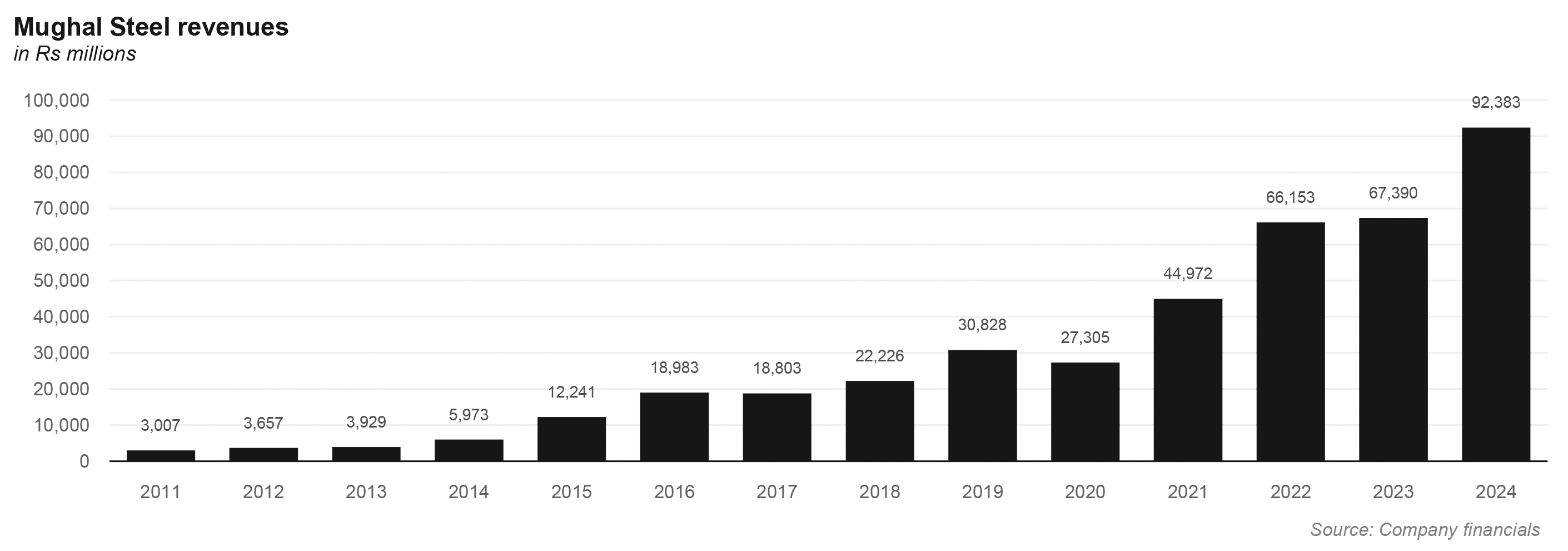

Mughal Steel has been one of the most dynamic companies in Pakistan’s steel sector and one of its fastest growing. In the 13 years that the company has been an incorporated business, it has grown its revenue from Rs3 billion in financial year 2011 to Rs92.4 billion in the financial year ending June 30, 2024, an average annualized growth rate of 30.1% per year. And despite several difficult years, it has never made a loss during any of those years.

This is a company that has been able to steadily grow its market share and, unlike most of its competitors in the steel industry, has exposure not just to industrial users of steel, but also supplies steel directly to consumers looking for steel girders for home construction.

And the company continues to expand its industrial footprint. Mughal Energy Ltd (MEL), a subsidiary of Mughal Steel, plans to setup a 55MW coal-fired power plant with the proposed investment of $137 million in Lahore, it announced in June of this year. The energy from that power plant would be used to supply all of the production units for the company, which currently operates the second largest steel manufacturing plant in the country.

And earlier this year, the company had also announced an investment plan that would involve the company investing in Balancing, Modernization and Replacement (BMR) of existing bar re-rolling mill and procurement of 6 gas-fired generators (3.1MW each) at a total estimated cost of Rs1.75b. The company management plans to enhance its re-bar capacity from the existing 150,000 tonnes to approximately 350,000 tonnes. The company expects that the efficiency of the bar re-rolling process will improve resulting in reduced manufacturing costs and improved margins.

All of these moves have come as demand challenges have continued to weigh on the industry and may even be driving a consolidation in the industry, though Mughal appears to be the one company bucking broader industry trends. According to IMS Research, the industry’s profitability during the second quarter of calendar year 2024 was driven largely by a robust quarter from Mughal Steel.

Part of what drove the higher revenue and profitability was the surge in global copper prices, which tends to have a downstream impact on other metal products such as iron and steel. As the steel sector navigates these ongoing challenges, the focus remains on companies like Mughal, which are leveraging diversification and strategic growth in non-ferrous segments to bolster their financial performance amid a tough operating environment.

Zooming out, the steel industry faces its own set of macroeconomic challenges. Steelmaking in Pakistan relies heavily on imported raw materials, with iron ore and scrap metal comprising 60-70% of production costs. Between 2018 and 2024, scrap metal prices doubled, only to fall back to earlier levels. Yet, the rupee’s sharp depreciation has eroded the cost advantage this drop should have provided. Steelmakers are now grappling with a dollar that trades at Rs 280—up from Rs 100 just a few years ago.

Why the regulatory wants to allow this transaction

One suspects the reason the SECP is allowing this to happen is simple: they know that Pakistanis tend to be control freaks and are loathe to give up control. As a regulator, the SECP has competing responsibilities. Yes, having companies with strong corporate governance and accountability is important. But so is increasing the liquidity and investment opportunities open to the general public through the capital markets.

As matter stand today, the total market capitalization of all companies listed on the Pakistan Stock Exchange is under 14% of the total gross domestic product (GDP) of the country. This is significantly lower than even our regional peers. More worryingly, the market is not representative of the economy as a whole and many of Pakistan’s largest and most profitable businesses are not publicly listed.

While there are a great many reasons why each individual company might choose not to list publicly, the fact remains that fear of losing family control over what tend to be family-owned businesses is a major concern. The bargain the SECP is making is essentially hoping that more family businesses will be willing to share the economic value of their businesses if they do not have to give up meaningful control over their companies.

The Mughal Steel dual class shareholding, then is a trial balloon to see if some of the owners of Pakistan’s privately held companies take notice. In the next five years, if more of them decide to list their companies on the exchanges, this bet will have paid off.

Whether it will be worth the price – in the form of reduce accountability and potential for abuse of minority shareholder rights – remains to be seen.

Zain is a business journalist at Profit, and can be reached at [email protected]

View all articles →Comments

No comments yet. Be the first to join the discussion!