Engro’s Rs60 billion question

How the conglomerate will deploy this capital over the next few years will define its future for the next generation – and possibly that of Pakistan

It was a back-to-back series of announcements that shocked Corporate Pakistan: Engro Corporation, one of the largest private sector conglomerates in Pakistan, announced in March 2016 that would be selling a majority stake in its most promising subsidiary, Engro Foods. It followed that shocker with another one three months later in June 2016: that it would also be selling a significant proportion of its holding in its oldest, and still core, business line, Engro Fertilizers. All told, the company made Rs54.7 billion in capital gains from these two strategic transactions that year.

It was at that point that the speculation game was on. What would Engro do with that pile of money? Combined with other, smaller transactions, the total amount of cash on Engro’s balance sheet hit Rs60 billion, an astronomical sum by Pakistani standards. Clearly, the company was gearing up for a major strategic shift in direction and was expected to announce a series of other transactions that would soon signal where it was heading?

Two and a half years later, and long after the transactions have closed, the nation’s corporate sector – and capital markets – are still waiting to understand what Engro will do next.

So what happened? Why did Engro sell those shares in the first place? And why has it still not redeployed that capital into other ventures? What is it waiting for?

And, perhaps most importantly, what exactly does it plan to do with that pile of cash? To understand the answers to these questions, it helps to first understand what Engro will not be doing with the money.

The strategic re-alignment

By 2016, when Engro made those decisions, the board had been mulling the direction of the company for several years. In truth, it was an inflection point in the company’s history that had already seen two significant phases in the post-1991 management buyout era.

The first phase of expansion was what company director Samad Dawood calls the diversification phase. It lasted from approximately 1997 through 2012, when the company slowly expanded into areas outside of its historical core operations of fertilizer manufacturing and into petrochemicals, commodities trading, power generation, and food production.

The second phase can only be described as a deep foray into energy. While Engro had been engaged in the power generation business since 2005, the company did not begin its significant commitment to energy until 2014, when it was finally able to begin work on a coal mining and power generation project in Thar. It then diversified its commitment within the energy sector by commissioning Pakistan’s first liquefied natural gas (LNG) import terminal.

It was at that point that conversations in Pakistan’s capital markets – and even within the company itself – began to focus on just how much Engro would invest in the energy sector. So when the announcements came about the divestiture of its stakes in Engro Foods and Engro Fertilizers, the logical next question was: is Engro now just an energy company?

The initial conversations around that time very much seemed to indicate yes. Indeed, in interviews with Profit in December 2016, the company’s chairman and largest shareholder, Hussain Dawood, stated outright that Engro’s motivation behind selling those stakes was to raise the equity they would need in order to expand their investments in the energy sector.

“The reason for the Engro Fertilizers transaction had little to do with a desire to exit the business or to scale down exposure to it and more to do with the positive desire to raise cash to expand both Engro and Dawood Hercules’ presence in the power generation sector,” Hussain Dawood had told Profit at the time.

Samad Dawood, his son and also a board member, was even more bullish at the time. “We are long on the Pakistan energy market. Our group took over a controlling stake in Hubco [the Hub Power Company] back in 2012. We brought in new management, a new board, invested into the plant to improve its performance while simultaneously entering into some strategic partnerships with the Chinese, Engro and GE. As a result of these efforts not only the operational metrics went up but the market also appreciated the work we did. And since our acquisition we have been able to create 45% annualised shareholder return over the last four years.”

[caption id="attachment_57915" align="aligncenter" width="1800"] Engro Corporation headquarters at the Harbour Front Building in Karachi[/caption]

Engro Corporation headquarters at the Harbour Front Building in Karachi[/caption]

Over the course of 2017, however, the company’s management started having doubts about the energy strategy, though this was not immediately obvious to outsiders, since Engro kept financing its share of the commitment to developing a coal mine and coal-fired power plants in Thar.

But if you were paying attention to the balance sheet, and noticing the subtle shifts in the CEO and chairman’s letters to the shareholders each quarter, you could tell that something had moved.

The consumer-focused strategy

Since its founding in 1965, Engro has been an industrial, business-to-business commercial enterprise. Its first foray into the consumer-facing business was with Engro Foods in 2006, and while that investment was ultimately highly profitable, it was nonetheless an anomaly relative to the rest of Engro’s businesses, nearly all of which were either industrial, or serving business clients, not retail consumers.

While the core driving force of economic growth in most countries is ultimately consumer spending, Engro has never historically been in any of the layers of business closest to the consumer’s wallet. However, in 2017, the company made a decision to start heading a little closer to direct consumer spending.

The first public hints of the new strategy came in August 2017, when a Malaysian company – edotco Group – announced that it would be buying out 13,000 cellular telecommunications towers from Jazz, Pakistan’s largest mobile telecommunications operator, and that it would be forming a joint venture with Dawood Hercules Corporation in order to do so.

Strictly speaking, the Dawood Hercules Corporation, while the single largest shareholder of Engro Corporation, is an independent company with its own management and a board that has overlapping, but not completely the same, board memberships. But because Hussain Dawood is the chairman of both companies, and because he controls a lot more of DH Corporation than Engro, it is sometimes seen as a precursor to what the market can expect to see in Engro.

For instance, Dawood Hercules bought a share in the Hub Power Company in 2012 before the major push into the energy business by Engro. And Dawood Hercules sold its fertilizer business two years before Engro sold a significant stake in its fertilizer manufacturing subsidiary.

So the edotco transaction could be seen as an early indication of a shift in priority: stay focused on a business-to-business enterprise, but move just a little closer to consumer spending. While the transaction was ultimately unsuccessful (it was denied regulatory clearance), it was a clear signal of intent.

Since then, rumours have been swirling throughout corporate Pakistan about what Engro might buy next. Just about anything that is up for sale, or even considering going up for sale, is being pitched, or is being rumoured to have been pitched, to Engro. Pakistan is not a rich country, so when a publicly listed company has Rs60 billion idling on its balance sheet, word gets around fast, and the opportunists line up very quickly at the door.

What’s causing the delay?

Two years is a long time in the corporate world. And in a country like Pakistan, where macroeconomic indicators can shift rapidly, it is a very long time. Since the Engro Foods transaction was announced, for instance, the Pakistani rupee has depreciated by 33.2%. Besides the expected impact that depreciation will have on inflation, that also means that any equipment that needed to imported from abroad, or any foreign shareholder who needs to be paid to buy a company, now has a cost basis that is more than 33% higher than it was two years ago.

The delay, in other words, has serious consequences. And it is starting to get the critics to question the judgment of the company’s management and its board of directors.

“It is not that hard to deploy Rs60 billion in capital in Pakistan. The Dawoods make it difficult because they are being too careful and conservative [with their investment strategy],” said one finance professional who is familiar with the deliberations at Engro, and chose to remain anonymous because they were not authorized to speak to the press on the matter.

For their part, the Engro board – and the Dawood family in particular – are aware of the criticisms and are not bothered by them.

“The decisions we make now will impact the direction of the company for the next 25 to 30 years. We want to be very deliberate about where we deploy that capital so that it can have the maximum impact,” said Samad Dawood, in an interview with Profit.

In other words, what’s a few months of deliberation when you’re setting the direction of one of the most important companies in the Pakistani economy for an entire generation?

And it is not as though the company has been sitting idly by, watching opportunity pass it by. Both the management and the board of directors are actively evaluating several options, in several key sectors.

So where will they take this storied Pakistani company? Based on information gleaned from the company’s own public statements, as well as sources who are familiar with the company’s deliberations, we have gleaned a picture of what some of the top contenders for Engro’s capital might be.

Petrochemicals: expanding into complex processes

The one near-certainty about where Engro will be deploying some of its capital is in the petrochemical sector, where the company’s subsidiary – Engro Polymer and Chemicals – has publicly stated its interest in setting up a petrochemical cracking facility in Pakistan.

At a symposium held in Islamabad on October 24, 2017, Engro Polymer CEO Imran Anwar said: “Let's build our own naphtha cracker as Pakistan needs it.” And in its investor presentation for the third quarter of 2018, Engro Corporation identified ethylene crackers as an opportunity for investment.

[caption id="attachment_57917" align="aligncenter" width="1255"] Petrochemical Plant[/caption]

Petrochemical Plant[/caption]

The company has clearly decided that cracking – an industrial process that involves breaking down larger, more complex hydrocarbon molecules into smaller, more useful hydrocarbons – is something it would like to invest in. It appears to simply be deciding on which type of cracking would be most feasible for the Pakistani economy. Once it makes that decision, it can be expected that a significant portion of the company’s capital will be deployed in Engro Polymer’s expansion into a new line of business.

It is somewhat understandable as to why Engro is probably closest to making a decision on this petrochemical business. It is close to the company’s roots, involves a large capital outlay that few other players in the country can match in terms of both capital and technical expertise, and has an industrial client base that Engro is quite comfortable selling to and already has established relationships with.

Logistics: infrastructure for the supply chain

One business area that Engro has been interested in since at least 2011 has been logistics. Pakistan has atrociously bad supply chains, in large part because both the physical and commercial infrastructure required for efficient supply chains simply does not exist in the country. (Physical infrastructure refers to roads, railways, and air transportation facilities. Commercial infrastructure refers to large scale companies dedicated to providing the ability to move and store goods.)

Engro has been studying this area for a long time, and the board is convinced that logistics as a sector of the Pakistani economy is worth investing in. The discussion within the company, however, centers around which vehicle would be best suited to capture significant economic value from improving the currently atrocious inefficiency of Pakistan’s logistical infrastructure.

On that front, the company faces essentially two paths: it can seek to build something from scratch, or it can buy out an existing company and then invest in expanding it to scale. In his conversation with Profit, Samad Dawood confirmed that the company is evaluating both options, but implied that a decision has not yet been reached on the matter.

[caption id="attachment_57918" align="aligncenter" width="1024"] Logistics[/caption]

Logistics[/caption]

Sources familiar with the company’s thinking say that any organic foray into the logistics space would involve the company investing in creating a subsidiary that would first handle Engro’s own internal logistics need as its business core, following which it would seek to expand into serving other businesses as well. Given the fact that Engro has thousands of distributors selling to over 11 million farmers in the country, it certainly has a large enough internal need to form the basis of a significant logistics company in its own right.

Healthcare: hospitals for the middle class

In statements to the press as well as investors, Engro Corporation has confirmed an interest in the healthcare sector in Pakistan, though the precise form of what that investment will look like has not yet been stated publicly by the company.

However, sources familiar with the company’s deliberations on the matter say that Engro is considering a partnership with Ashmore, the London-based emerging-markets-focused investment management firm, and King’s College London Hospital to set up a chain of hospitals throughout Pakistan. The hospitals would seek to cater to middle and upper-middle class consumers who want access to quality healthcare and are willing to pay a brand premium for a European hospital company’s facilities within the country.

It is unclear how far the discussions have progressed with respect to this proposal, nor is it clear what is sticking point between the three parties with respect to pulling the trigger on proceeding with the project.

When asked by Profit to comment on the matter, Samad Dawood neither confirmed nor denied that Engro was engaged in such a discussion, but simply stated that the company is indeed evaluating opportunities in healthcare.

[caption id="attachment_57919" align="aligncenter" width="1600"] King's College London Hospital at Dubai[/caption]

King's College London Hospital at Dubai[/caption]

Should Engro succeed in bringing King’s College London Hospital to Pakistan, it would not be the first foray into the region for the famed London institution. King’s College Hospital UAE currently operates two medical centers in Dubai, one surgical and medical center in Abu Dhabi, and is in the process of constructing a 100-bed hospital in Dubai. Nonetheless, it would be the very first foreign healthcare brand to enter the Pakistani market, outside of the pharmaceutical sector.

Real estate: the ‘safe’ bet

In September 2018, Reuters published an interview with Engro CEO Ghias Khan that suggested the company might be interested in investing in real estate, or at least was considering opportunities in the space. “ Undeterred by Chinese investment jitters and the recently wobbly economy, Khan said Engro was weighing acquisitions and starting new businesses in agriculture, healthcare, real estate, communications and other consumer-linked sectors to profit from rising incomes in the Muslim majority country of 208 million people, 60 percent of whom are aged under 30,” the Reuters story stated.

It quoted Khan as saying: “If you look at sectors that did well when they were where Pakistan is today ... like real estate, automobiles, healthcare, logistics – everything is somehow related or linked to population growth or the middle class.”

And there were indeed some rumours earlier this year about Engro possibly considering an acquisition of Emaar’s assets in Karachi’s Defence House Authority neighbourhood, specifically the Crescent Bay project. However, while real estate is certainly a consumer-facing area of investment, it is one that is likely one of the least attractive from an institutional investor’s perspective, not least because of the extreme distortions in land prices in Pakistan that result in monthly mortgage payments frequently being twice as high as monthly rents for the same property.

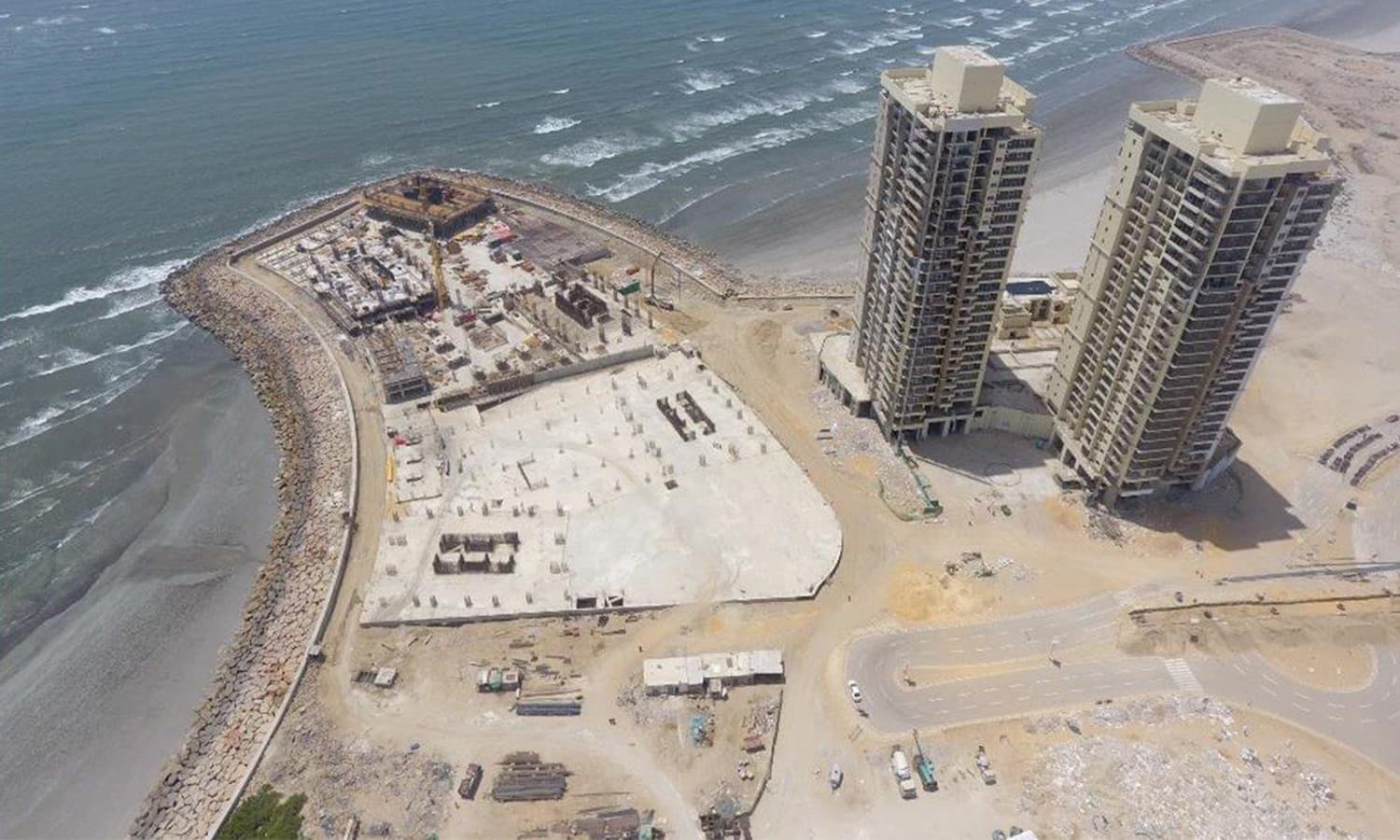

[caption id="attachment_57920" align="aligncenter" width="1500"] Crescent Bay Karachi construction site[/caption]

Crescent Bay Karachi construction site[/caption]

It is unclear what Engro would even do with real estate. Everything the company’s management and board of directors have stated suggests that they are looking for long-term investments in building out essential services for Pakistan. But once a real estate project is done and sold, that is it as far as the developer is concerned. They move on and build something else in a different location. Even if Engro were to consider what would at this point effectively be a bailout of Emaar in Pakistan, what would they do even if they managed to finish building the Crescent Bay project and sell all of the apartments (a big if, one might add)?

Engro is unlikely to see itself as a real estate development company. So why bother investing in a massive, capital-intensive asset that does not have the potential to be a long-term investment?

A broader vision

If there is one phrase that would describe Engro’s approach to how it is thinking about its investment strategy, it is “purpose-driven capitalism”, an almost idealistic vision of the ability of capital – and those who wield it – to change the world they inhabit for the better by investing in things that people need, and making money along the way.

“Purpose” is a word Samad Dawood used repeatedly in his interview with Profit, suggesting that it is a concept that is top of mind for the board, and likely a key deciding factor in how the company will make its decision. As chairman of the board’s investment committee, Samad is likely to have considerable influence on the ultimate outcome of those deliberations.

The investments that Engro is considering do not have a unifying commercial theme, other than the fact that they each address a critical piece of the infrastructure that Pakistan needs for its economic development and currently does not have.

In that respect, the old spirit of Engro – imbued into the company’s soul by its first post-1991 CEO Shaukat Raza Mirza – appears to be alive and well: the notion that the company should be the vehicle where the best of Pakistani corporate talent meets a large pool of capital and seeks to solve some of the country’s biggest and most complex challenges.

Regardless of what direction they take next, regardless of what project they choose, if Engro can keep that spirit alive within its workforce, it will likely find itself succeeding financially.

Managing Editor, Profit Magazine. He can be reached at [email protected]

View all articles →2 Comments

No comments yet. Be the first to join the discussion!