In committing to exchange rate peg, PTI is repeating Ishaq Dar’s folly

The nature of Pakistan’s system of parliamentary governance is such that, while the budget is one of the most important pieces of legislation every year (the only bill explicitly mentioned by name in the Constitution), it is also among the least debated bills in the legislature. The only place in Parliament, ironically, where there is any debate of any kind is the Senate finance committee (ironic, because the Senate as a whole is not even allowed a vote on the budget bill, the only bill excluded from their powers.)

So it is somewhat discouraging to see how the Senate Finance Committee operates in the era of the Imran Khan Administration. Consider the following scene.

Senator Talha Mahmood of Khyber-Pakhtunkhwa (JUI-F) proposes that the State Bank of Pakistan be required to maintain a peg for the exchange rate of Rs150 to the US dollar, and the committee approves the motion unanimously and without debate. Did we mention that while they asked a lawyer, an accountant, a mathematician, and several civil servants to weigh in on the matter, not a single economist was invited to deliver their testimony or recommendations on matters of … you know… economic policy?

Of the two chambers, the Senate is supposed to be the more deliberative body, its members elected not in a general election, but by members of provincial assemblies, and thus allowing more cerebral politicians who may be ill-suited to electoral politics, to enter Parliament. And the Senate Finance Committee, seeing as how it is the only part of the Senate that is meant to have any kind of oversight over the budget at all, is meant to have the most capable of senators on it.

That is decidedly not the case at the moment.

Far from being engaged in offering substantive oversight over the government’s actions and policies, the senators on the committee appeared to be so lethargic and perfunctory in performing their duties that they did not even bother reading a three-page document presented to them on taxation and trade policy, and insisted that the civil servant at hand “read to them out loud the ‘crux’ of the proposed policy amendments.”

This may not be corruption, but it is gross incompetence and dereliction of duty on the part of elected members of Parliament.

Small wonder, then, that they pushed through a policy that is likely to have disastrous consequences for the country and likely mean that Prime Minister Imran Khan’s pledge that this International Monetary Fund (IMF) bailout be the last will become a joke.

Repeating past mistakes

Here is a shocking statistic: in US dollar terms, Pakistan’s gross domestic product (GDP – the total size of our economy – has shrunk by 10.3% in the fiscal year ending June 30, 2019. Here is an even bigger shock: the last time the economy shrank by this much was in the immediate aftermath of the 1971 war, in fiscal 1973, the first full year after that calamitous conflict.

The cause of this stunning collapse is by now well-established, if not entirely well understood. Former Finance Minister Ishaq Dar held the exchange rate at an artificially high level and drained scarce Pakistan’s foreign exchange reserves in order to do so. The exchange rate, like most macroeconomic levers, is a bit like a rubber band: the longer you stretch it beyond its normal shape, the greater the force with which it will hit you when are you ultimately forced to let go.

Dar held the rupee in an unnatural position for far too long, and that is why the exchange rate collapsed like a ton of bricks when he – and the government of Pakistan – could no longer hold on. In rupee terms, the economy is not actually doing too badly. It has slowed down, but economic activity, even adjusting for higher rupee-denominated inflation, is still growing. It is only in US dollar terms that the economy has seen a severe contraction, the likes of which has not been seen since 1973.

Nonetheless, Pakistan does not compete against other economies in rupees and, more importantly, it does not buy what it needs from other economies in rupees, meaning the shrinking of the size of our economy relative to others matters, and will hurt the economic wellbeing of its citizens unless something is done to fix the problem.

Unfortunately, while the Pakistan Tehrik-e-Insaf (PTI) led government loves to – correctly – pin the blame for the shambles the economy currently finds itself in on the preceding Pakistan Muslim League Nawaz (PML-N) led government, it appears that the Imran Khan Administration is committing itself to the same macroeconomic folly as the Nawaz Administration, indeed folly that can be traced as having roots in Pakistan’s economic establishment as far back as the Liaquat Ali Khan Administration.

(Oh, you thought Pakistan’s founding generation was better? No, they were just as grossly incompetent as the current lot, sorry to disappoint you.)

At Profit, we have previously discussed a detailed history of this insane policy – including an explanation as to why it is insane – and will not repeat ourselves here. However, it is important to recognise that there are some in the Senate, including some who voted for this resolution, who realise just how asinine this policy is and how damaging it will be to the country’s economy.

Senator Farooq Hamed Naek of Sindh (Pakistan Peoples Party) acknowledged, when asked by Profit, that the proposal to peg the rupee to a specific value of the dollar was absurd. But he had nothing to say during or after the discussion in the committee meeting itself.

Other members of the committee simply said that allowing currency devaluation causes inflation, but failed to answer questions about how sustainable it is to have the currency crash every few years and cause massive spikes in inflation, followed by recession, which is what happens under the current policy. A floating exchange rate, on the other hand, would allow for a slightly elevated level of inflation, but within a narrower, more predictable band, and cause far fewer crashes and recessions.

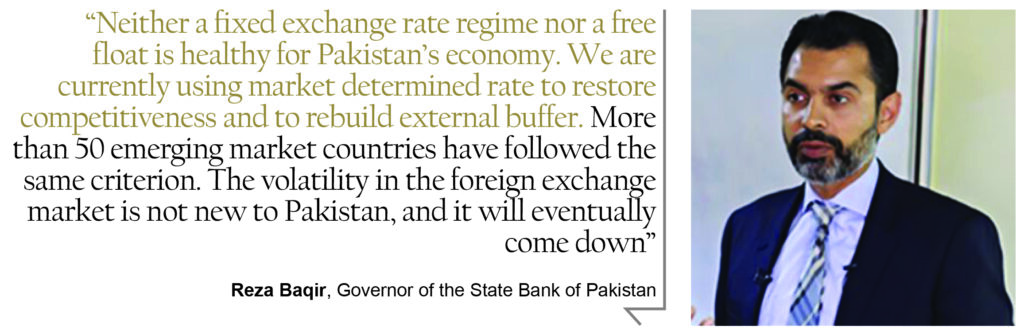

Meanwhile, even as the Senate has asked the central bank to control the exchange rate, the State Bank of Pakistan (SBP) itself appears to be trying to create a little more wiggle room for itself, not committing to a market-determined exchange rate, but trying to stay away from a peg as well.

In a briefing held at the SBP headquarters in Karachi this month, State Bank Governor Reza Baqir said that: “Neither a fixed exchange rate regime nor a free float is healthy for Pakistan’s economy. We are currently using market determined rate to restore competitiveness and to rebuild external buffer. More than 50 emerging market countries have followed the same criterion. The volatility in the foreign exchange market is not new to Pakistan, and it will eventually come down.”

Yet the governor also appeared to slightly contradict himself by stating that the market-determined exchange rate also needs occasional intervention from the central bank. But can Pakistan afford to expend further resources on these "occasional interventions"?

The inflation threat

Here is the threat everyone always cites when saying that the exchange rate needs to be kept stable: that it impacts inflation, which in turn affects the poor the most. This is partially true, but does not reflect a broader context: the poor are particularly badly hit by the periodic crashes far more than slightly elevated inflation.

And here is the part nobody seems to be talking about: yes, inflation is higher this year than last year, but since when does 13% inflation sound calamitous in the Pakistani context? How is it that the currency collapsed by over 25% last year, but inflation only went up by 12-13%? Simple: because inflation, amongst other factors, depends a lot more on global oil prices than it does on the value of the rupee. And since global oil prices are stable – and low – a collapse in the value of the rupee has not resulted in skyrocketing inflation.

Shooting long-term growth in the foot

The problem, of course, is that the government knows that normal economic activity would not justify an exchange rate that stays at one level for very long, which is why they are beginning to crack down on economic activity, which is a bit like trying to stop bleeding in one’s arm by stopping the heart: technically, it will work, but now you have a bigger problem to deal with.

Among the measures being considered: reducing the amount of cash people are allowed to carry outside the country on foreign travel from the current limit of $10,000 per person to $3,000 per person. Other provisions already affecting commercial transactions: hidden limits on repatriation of profits by investors or sale of shares by foreign investors if it means cash leaving the country.

The problem with all of these measures is that they trade short-term stabilisation for long-term stability and growth. Consider the following fact: if you do not know that you will be able to take your money out of a place, no matter how safe or lucrative the investments there, why would you ever put your money in there? Why would any foreign investor take the government’s promises about facilitation on their investments seriously if they can see previous foreign investors’ cash trapped inside the country?

The purpose of any investment, after all, is to create a cash flow that one can use. Foreign investors, by definition, live outside the country and therefore, at some point, will want the cash to leave the country, even if they are very long-term investors.

Even more absurd is the government’s crackdown on foreign assets and criminalisation of moving money outside the country by citizens of Pakistan. Why on earth is this illegal to have money outside the country? Why does the government believe that the best way to get wealthy Pakistanis to move their money back to Pakistan is to force them to do so and to make it illegal to move it out?

Last we checked, the rich manage to find a way to move money out of Pakistan anyway and every crackdown means that they are less and less inclined to ever move it back. Did you know, for instance, that banks in Pakistan held nearly $10 billion in foreign currency deposits in May 1998, shortly before the Nawaz Administration froze their accounts and forbade them from accessing their own money?

That number dropped to $0.2 billion by 2004, as people kept withdrawing as much money as they could over time until there was almost none left. Do you know how much there is in foreign currency deposits at Pakistani banks now? $7 billion. More than 20 years later, the level of foreign currency deposits has still not recovered.

This is despite the fact that the government eventually lifted that policy and never tried anything like that since. Once you lose the trust of the people, it takes decades to earn it back. And in the meantime, Pakistan continues to keep falling behind its neighbours.

6 Comments

No comments yet. Be the first to join the discussion!