Ladies and gentlemen, if we can get your attention for a moment, the bond market of Pakistan would like to make an announcement: the recession is over. We repeat, the recession is over. The economic recovery can now begin. Unfortunately, while this good news has been telegraphed clearly throughout the country’s financial community for the last few weeks, the subtext appears to not be fully appreciated: the bond market is also signaling some serious causes for concern.

At this point, you may be thinking to yourself: what is the bond market and why should I care? Well, you should care because you are probably a more active participant in the bond market than you are in the better known – but smaller – stock market. And, more importantly, the bond market can affect you in ways that the stock market – or most other markets – cannot.

In its simplest terms, a bond market is just that: a market to buy and sell bonds, which in the case of the Pakistani market, almost invariably means government bonds. Unlike stocks, which represent a share in the ownership of a company, a bond is a promise to pay; essentially a loan, with a fixed repayment date, and interest rate.

How big is the government bond market? As of June 30, 2019, the total size of the domestic government bond market stood at Rs20.7 trillion, according to data from the State Bank of Pakistan. For comparison, as of October 17, 2019, the market capitalisation (the total value of all publicly listed stocks) of the Pakistan Stock Exchange stood at Rs6.7 trillion and has never gone higher than Rs11 trillion.

More importantly from the perspective of the ordinary person, government bonds are where over half of bank deposits are invested, and determine the cost of borrowing – and, therefore, the extent to which businesses have the ability to expand their operations.

So, what exactly is happening in the bond market? And what does it mean for the economy?

A brief introduction to bond mathematics

This article will use some concepts in bond mathematics, and while it is not necessary for most people to understand the details, it is helpful to understand directions of movements in bond prices and interest rates (which move in opposite directions from each other) and what that means. If you know how bonds work, feel free to skip this section

As we stated earlier, a bond is simply a loan: it has a fixed amount that needs to be paid back, at a specific time period, as well as interest payments (usually semi-annual) that need to be made.

Most corporate bonds in Pakistan are variable rate, meaning the interest rate resets every year. Most government bonds, however, are fixed rate, which means that they pay the exact same interest (as a percentage of their face value) every single year until maturity.

This matters because as interest rates change, investors’ willingness to buy certain bonds increases or decreases. For instance, if you own a bond that yields an 8% interest rate and you bought it for Rs1,000 per bond, and the interest rate reaches 12%, why would you want to continue owning that bond when you can buy a new one that yields so much higher?

If you then went out into the market to try to sell the bond, nobody would be willing to pay Rs1,000 for it. They would be willing to pay a lower price which would make those interest payments (Rs40 every six months, in this example) be worth the same – in percentage terms – as the 12% interest rate they could receive on the new government bonds.

In other words, if interest rates go up, the price of existing bonds (which by definition have a lower interest rate) will go down to ensure that their yield-to-maturity becomes equal to a comparable new bond. Conversely, if interest rates go down, existing bonds become more valuable and therefore rise in prices.

We have skipped over several concepts, not least of which is yield-to-maturity, which is the effective interest rate on a bond until its maturity date, based on its face value, stated interest rate, and current market price. We will not delve into how yield-to-maturity is calculated, but it is the way to compare interest rates on bonds of different prices and different maturities.

The yield curve

One more key concept: in general, the longer the time to maturity of a bond (maturity meaning when the full repayment is due), the higher interest rates investors will demand, at least under normal circumstances. The reason: the longer the time to repayment, the more things can go wrong, and the more likely it is that the loan / bond will not be repaid.

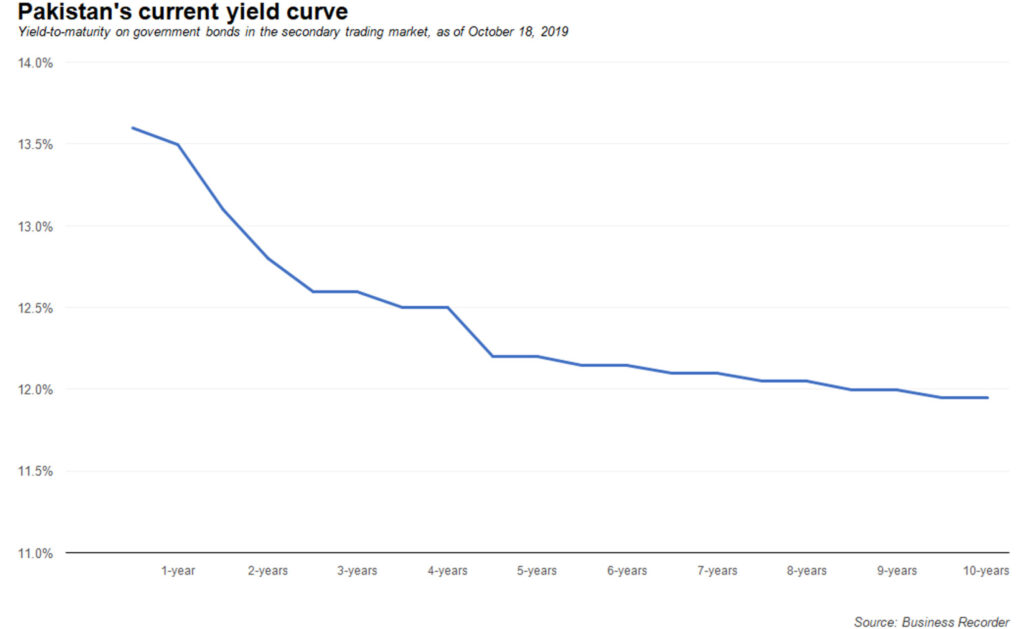

That last point is particularly crucial, because it forms the basis of a concept known as the yield curve. The yield curve is a graph of the average yield-to-maturity of bonds against the time to maturity. Under normal circumstances, it should be an upward-sloping line: as time to maturity increases, so does yield-to-maturity of the bonds.

When the slope is curving upwards normally, there really is not much to say about the curve. It is only when the curve inverts that matters start to get interesting.

An inverted yield curve refers to the phenomenon, usually relatively brief and anomalous, of when short-term interest rates are higher than long-term interest rates. That signal is generally taken to mean something important in most economies, though its interpretation can differ widely depending on the type of economy in question.

The inverted yield curve

In the United States, the economy where the very concept of a yield curve was invented, an inverted yield curve almost invariably means one thing: the onset of a recession. Why? Because in the United States, an inverted yield curve happens when investors believe that the prospects for the economy have dimmed, and that the economy will be slower, with corresponding lower inflation, and thus lower interest rates than ones that currently prevail.

Here is how it works. Let us suppose that interest rates on a one-year bond are 4% and the interest rates on a 10-year bond are 6%. If you believe interest rates will go down, you will also believe that the value of both bonds will go up. However, you also do not know when that will happen, making it less likely that you will want to buy the one-year bond, and making it a much safer bet for you to buy the 10-year bond.

As a result, investors start buying more long-term bonds under the assumption that they will gain more value as interest rates decline during a recession. That, in turn, becomes a self-fulfilling prophecy: as more investors buy those bonds, their prices rise, and hence their yields fall below short-term interest rates, even before the recession actually arrives, making an inverted yield curve a leading indicator of a recession.

However, as you can see, that phenomenon relies on a certain set of assumptions about the relationship between inflation, interest rates, and the nature of the economy.

Specifically, it assumes that the economy has a normal rate of inflation that slows down during a recession, and that the central bank, broadly speaking, sets interest rates to be positive in real (inflation-adjusted) terms. While that second assumption is mostly true in Pakistan, the first assumption is not. And that has to do with the particular dysfunctions of Pakistani society.

But before explore that, it may be helpful to figure out just when the yield curve inverts in Pakistan, and what clues that might have as to what it means.

When and why yield curves invert in Pakistan

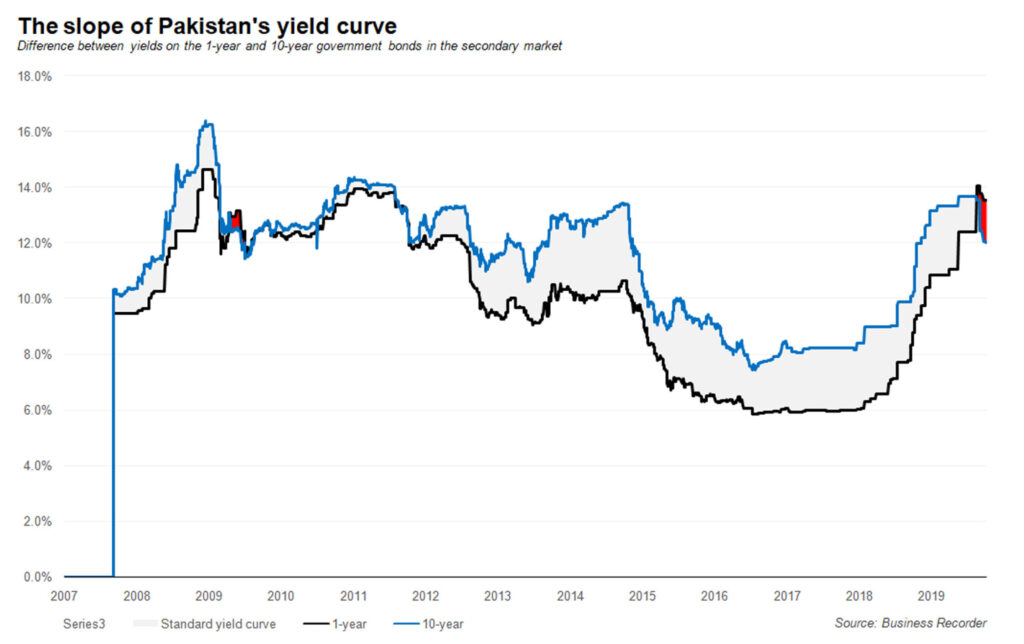

We must caveat our analysis by saying that our dataset – which relies on Business Recorder’s data on secondary market trading in government bonds – only goes back through to September 2007, so it only covers two major recessions in Pakistan’s economic history. Nonetheless, the data from both of those recessions is very compelling and paints a logical, if somewhat counterintuitive, picture.

To conduct this analysis, Profit looked at the differences in the yield-to-maturity between the one-year government bond and the 10-year government bond and examined which periods that number turned negative (meaning when the 10-year bond started yielding less than the one-year bond).

There were two clear periods of when this happened: the first one started on April 9, 2009 and continued, with some minor interruptions, through October 3, 2009, a period of almost six months. The second significant period started on August 19, 2019 and appears to be continuing as of the writing of this article. There was one other relatively brief period of negative yields which lasted from August 25, 2011 through October 7, 2011, which we will address later.

The two clearest periods of negative yields both have one thing in common: they both occurred shortly before or shortly after the end of a fiscal year of negative nominal growth in the gross domestic product (GDP) – the total size of the economy.

In other words, unlike in the United States, where the inverted yield curve is a leading indicator of a recession, in Pakistan, it is a lagging indicator of a recession and usually marks the beginning of a recovery.

How does an inverted yield curve in Pakistan mean completely the opposite of what it means in the United States? The answer lies in the differing structures of the two economies, and the role that currency crises play in both inflation and recessions in the case of Pakistan.

Pakistan’s recessions typically tend to be the product of a fundamentally insane policy decision that the country’s leadership has been repeating since 1949: a belief that, somehow, there is a magic number for the rupee’s exchange rate against the US dollar that must never change.

This, quite obviously, is not something that a country like Pakistan, with its perennial trade deficits and lack of significant foreign investment flows can keep up. As a result, periodically, the government’s attempts to control the price of the rupee fail miserably and it comes crashing down, not with a steady dribble of depreciation, but with a crash that frequently brings down with it the whole economy.

When the rupee crashes, that also causes a spike in the inflation rate, since Pakistan is now (and has been since at least the late 1990s) a net importer of energy. If the rupee price of energy goes up, so does the price of everything else, which causes a spike in inflation. In short, while in developed economies, a recession causes a decline in inflation as businesses maintain or even cut prices to try to stay competitive, in Pakistan, businesses are forced to raise prices because they are facing a sharp rise in their cost of production or doing business.

So now put yourself in the shoes of a Pakistani bond investor: if you think the worst is over for the economy, and that the recovery has begun, what do you think will happen to inflation, and thus to interest rates? You will expect them to decline from their sharply high levels, which means that – in an economic recovery – you would expect interest rates to also decline.

Knowing what you know about expected interest rate movements, if the one-year bond is available at a yield-to-maturity of 12% and the 10-year bond is available at a yield-to-maturity of 14%, you would be better off buying that 10-year bond because its price would rise faster. So that explains why the yield curve inverts.

What it does not explain, however, is why the yield curve inverts after the recession is over, and not during it. After all, in the US, the inversion happens before the event it predicts happens. Why not the same for Pakistan, which would mean that the inversion should happen before the recovery (and thus during the recession)?

The answer is both obvious and somewhat painful: data frequency. In the United States, bond traders have mountains upon mountains of data that tell them whether and when to expect a recession, and hence the market moves much more quickly. In Pakistan, unfortunately, while some economic indicators have frequent signals, most are issued on a very infrequent basis, almost invariably by a handful of government departments. Hence, Pakistani bond traders simply cannot have a clearer sense of when to expect an economic recovery until it has already started.

The 2011 inversion

So then why did the yield curve invert in 2011? The 2008 recession was long over and 2010, while not a great year, was not terrible either. Why the inversion? That particular inversion had to do with an experiment that had taken place in the first half of 2011 that died in the latter half of that year: a central bank that actually tried to rein in the federal government’s profligacy by raising interest rates.

But once Shahid Kardar, then the governor of the State Bank of Pakistan had reached his limits and was summarily fired from his job in July 2011, the bond market corrected for the expectations that interest rates would remain elevated. Once bond traders realized that Kardar’s departure meant a reduction in rates again, the yield curve inverted.

Yes, you read that correctly: the bond market gave Shahid Kardar his very own send-off through the yield curve. He may have lasted less than ten months in office, but he may – quite possibly – be Pakistan’s only central bank governor with that distinction. Well played, sir. Well played.

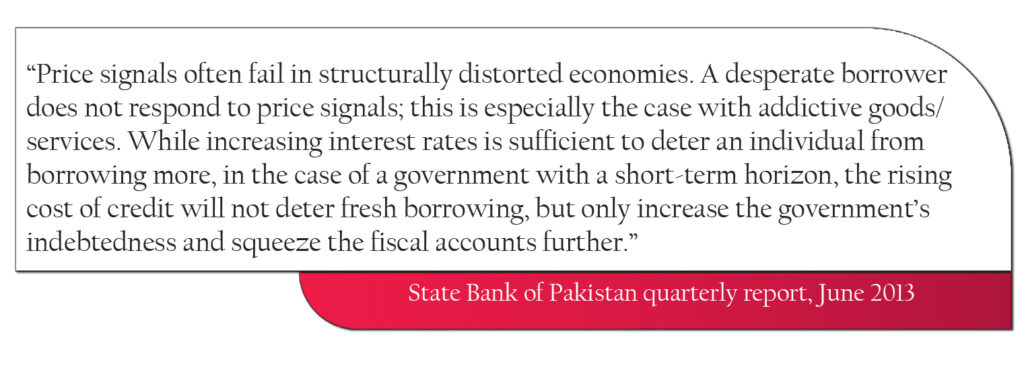

The longer-term impact of this ouster was that, by 2013, the State Bank of Pakistan had economists writing papers describing the federal finance ministry’s borrowing habits like one would ordinarily describe a heroine addict: twitchy, oblivious to pain, and making a series of poor life choices.

In a bit of subversive competence, in June 2013, the State Bank managed to publish their research as part of their more publicly well-known quarterly report and described the finance ministry in the following way: “Price signals often fail in structurally distorted economies. A desperate borrower does not respond to price signals; this is especially the case with addictive goods/services. While increasing interest rates is sufficient to deter an individual from borrowing more, in the case of a government with a short-term horizon, the rising cost of credit will not deter fresh borrowing, but only increase the government’s indebtedness and squeeze the fiscal accounts further.”

No, ladies and gentlemen, that was not editorial comment about the heroin addict: that is language from official documents produced by the State Bank of Pakistan describing the Federal Ministry of Finance. What a glorious time to be alive!

So what if the yield curve inverted?

So the yield curve inverted because Pakistan’s economy is about to recover. Big whoop. Everyone knows that already. Why should anyone care about the yield curve at all then?

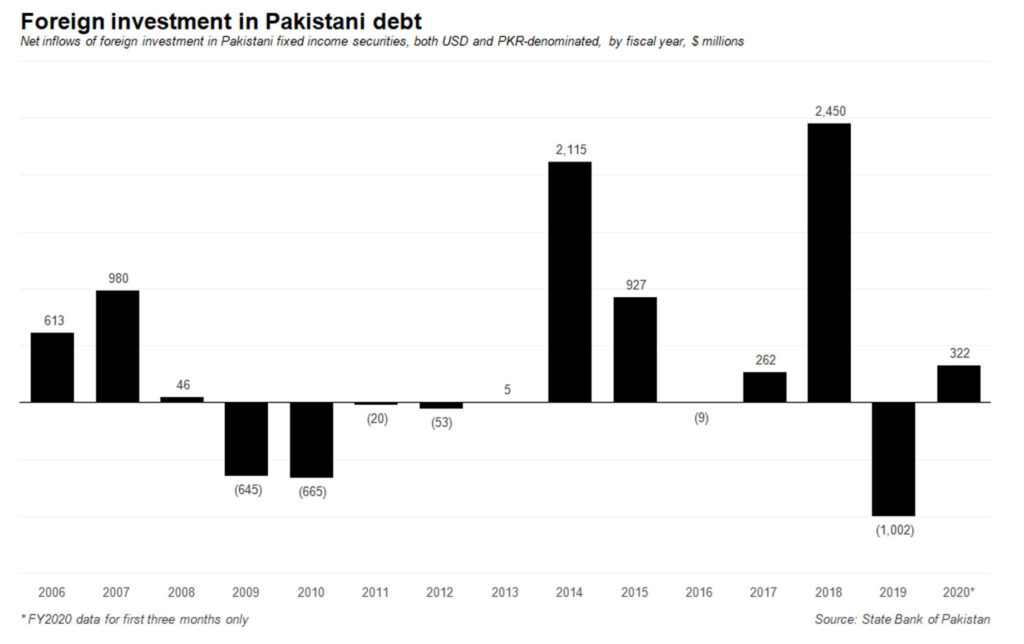

Because of the reason as to why it is inverting this time: significant inflows into the rupee-denominated government bonds from foreign investors, which recent news reports suggest have reached $354 million since July of this year. Yes, local bond market investors would have likely caused an inversion on their own too, but having foreign investors pump in money into the bond market is a somewhat bullish signal for the economy… up to a point.

While, in general, it is good for the country to receive investment from foreign sources, since it signals global confidence in the country’s macroeconomic indicators, the problem with the current flow into the rupee-denominated bond market is that all of this is what is known as “hot money”: temporary flows of cash chasing higher yields that will leave the second it can find something better elsewhere.

Given the fact that Pakistani economic crises tend to occur with a sudden collapse in the price of the rupee, does anyone seriously believe that having this hot money enter the country would do anything other than significantly worsen the next financial crisis in the country?

One suspects that a highly respected economist like State Bank Governor Reza Baqir is well aware of the nature of Pakistan’s economic distortions and how this flow of hot money is unlikely to be helpful in the medium to long run. Indeed, if the flows of this hot money investment were to continue to accumulate, they may well approach creating a crisis for Pakistan similar to the 1997 Asian Financial Crisis.

Unfortunately, the State Bank has no good options here. If it lowers interest rates too soon, it risks encouraging government borrowing which would even further crowd out the private sector from the banking sector’s lending activities, and further slow down the economy. If it seeks to curb the flows of foreign money through regulatory means, it would be cutting off a source of dollars at a time when the economy can use all the foreign investment it can possibly get. The bank is damned if it does and damned if it does not.

Ultimately, however, the country is likely better off without the flow of hot money and remaining a destination for a smaller, but more sophisticated set of foreign investors who would seek to do business in Pakistan in the long run rather than seeking the quick buck to be made from the current set of high interest rates.

More importantly, given the fact that the finance ministry is best thought of as a heroin addict when it comes to borrowing, it is probably not a good idea to provide the addict with a new crack pipe (i.e. a new source of borrowing). The situation is bad enough without the finance ministry getting even worse ideas about how to continue relying on flaky hedge funds for their more permanent needs for capital.

When it comes to suppliers of addictive substances to an addict, the State Bank should act like a responsible sponsor and just say no on behalf of their ward.

WHAT DO YOU SAY ABT NEXT M.P.S, THE PRESSURE FROM BOTH SIDES IS EQUAL, PULLING UPWARDS=IMF+INFLATION+$ PARITY, DOWNWARDS=INDUSTRY

TELL ABT FORWARD RATE, IS IT AVAILABLE, WHICH SIDE MAY BE USEFUL, SHORT OR LONG.

$354 million equal to only Rs. 55 billion, thats alone is not significant enough to invert the yield curve at all when you have have Rs. 2 trillion on average bids being placed in every auction.

US$354 Million may not be significant but it is the the FX market reaction once this money starts flowing outwards. Egypt is a good example where the bond market has attracted a lot of FX and FX reserves have increased however despite significantly lower inflation, reducing interest rate to single digit has become a challenge to the Central Bank of Egypt.

Comments are closed.