Pakistan’s agricultural sector is under strain from every direction. In a recent written reply to parliament, Finance Minister Muhammad Aurangzeb painted an alarming picture of the country’s agriculture sector. Crop failures, low yields, farmer migration to cities and compounding climate and economic crises have all laid waste to Pakistan’s most important economic sector. Add to this the devastating floods that hit the country in the monsoon season and you have a tale of crop loss, dead livestock, displacement, and major cash flow problems.

In fact, cash flow is enough of a problem that a significant portion of the letter addressed the falling credit disbursement to the farm sector by the government’s frontline agriculture support institution, Zarai Taraqiati Bank Limited (ZTBL). Total disbursements from ZTBL have fallen by 54% in the past two years from Rs 85.56 billion in 2023 to Rs 39.66 billion in 2025. For a bank created in 1961 to serve agricultural development, the contraction reflects deeper structural weakening, and the failure of the government to act as the financier for the agriculture sector.

While these recent woes seem to spell a doomsday scenario, behind the scenes, Pakistan’s commercial banks have been picking up the slack. Disbursements of agricultural credit by commercial banks increased by 16.2% from Rs 2.2 trillion in 2024 to Rs 2.58 trillion in 2025.

The increase is no coincidence. Over the past few years, the State Bank of Pakistan (SBP) has encouraged the country’s commercial banks to pick up the slack when it comes to providing financing to the agricultural sector. Historically, Pakistani banks have shied away from agriculture. With little understanding of crop cycles and the exact needs of farmers and even less effort to try and figure it out, lending to farmers has largely been collateral based and short term.

Clearly that is changing, and the shift is palpable. Only last month the Bank of Punjab told analysts that a third of their total loan book consists of lending to the agriculture and SME sectors. Even a decade ago this would have been unheard of. Among the top five banks, UBL increased their agricultural disbursements by 40% from Rs 164.7 billion to Rs Rs 231.6 billion. Similarly, even small banks that had previously been ignoring agriculture entirely have seen a slight shift. Sindh Bank had the single largest increase in disbursements at 440% compared to the previous year, although this was more a function of their disbursements in the previous year only being Rs 11.7 crores.

Among Islamic Banks, BankIslami stood out. It increased its disbursements by 88.6%, going from Rs 18.6 billion last year to Rs 35.1 billion this year. Overall, the Islamic Banking category actually saw the single largest percentage increase in agricultural credit disbursement amongst all banking segments at nearly 30%. In 2024, Islamic Banks disbursed Rs 136.6 billion in agricultural credit. In this last financial year that number had risen to Rs 177.4 billion.

The data is clear. Pakistan’s struggling agriculture sector needs better financing, and further encouragement from the SBP seems to have worked. Banks are improving their agricultural portfolios, credit and disbursements from commercial banks are going up. The only major commercial bank that has been disappointing with its performance in agricultural disbursements was the government owned National Bank of Pakistan (NBP), which saw a year-on-year increase of only 1.5% and barely reached the halfway mark of their credit expansion plan.

But out of all the commercial banks in Pakistan, the one that stands out the most is HBL. Last year, instead of giving targets to different banks for agriculture lending, the SBP asked banks to set their own credit expansion plans. HBL gave itself the largest target, aiming to have agricultural loan disbursements up to Rs 350 billion. They outperformed their own expansion plan, achieving 108% of their target by bringing their total disbursements to Rs 377.9 billion, more than any other bank in the country.

The change is seismic. Think of it this way: the only other bank to rival HBL on the agricultural front is the majority-owned Government of Punjab bank, Bank of Punjab (BOP). As we mentioned earlier, a third of BOP’s loan book is agricultural and SME financing. Not only this but these loans account for only about 8% of this exposure. While this is impressive, it is only achievable because a significant part, nearly 76.59%, of the agricultural lending is on the back of risk sharing with the Government of Punjab, leaving only a small proportion uncovered. As the largest agricultural producer in the country, it makes sense for the Government of Punjab’s bankers to be involved in agriculture and for the provincial government to support them.

But what was in it for the HBL Group? Why did Pakistan’s premier Bank and its subsidiaries decide to focus on a sector that has historically been ignored by the financial services industry? Where did the decision come from despite the significant risks the agriculture sector poses in the fast-changing age of climate change? The shift began earlier than many might think.

Changing perspectives

In February 2024, on the occasion of the ceremony marking the launch of HBL Zarai Services Limited, Sultan Ali Allana, Chairman – HBL said, “We have been actively pursuing programs and introducing solutions for the growth and progress of the Agricultural Sector since the privatisation of the bank in 2004. Alhamdullilah HBL Group today is the single largest institutional provider of financial services for this segment of the economy, directly impacting over 350,000 farmers. With the formation and launch of HBL Zarai, Insha’Allah, we will be able to host advisory and input services along with offtake and warehousing right at the farmers doorstep through Deras – dedicated distribution and service centres etched among the heart of the farmlands thus ensuring food security and income enhancement for the farming communities throughout the country.”

The remarks had not come from nowhere. Agriculture has always been a hot topic. The devastation of the 2022 mega-floods had put Pakistan’s climate driven farming crisis on the global map. For the banking industry, it was a moment of concern. Agricultural lending was already considered a risky business, and the threat of climate-induced disaster was shaking the foundations of what everyone, including farmers, knew about the farm business.

“We know that agri-financing is riskier. And if a bank wants to just do low-risk banking, then this sector is challenging. We need to keep in mind that there will be bad years like we are having with the floods, and there will be good years where we get major bumper crops,” says Aamir Kureshi, Head Products Transactional Services & Solution Delivery of HBL. According to him, the potential in agriculture not only outweighs its downsides, but is key to our country’s progress. Farmers, as he explains, genuinely want to make it work.

“As Pakistan’s premier bank, we have observed one thing. Even when a farmer is impacted by no fault of his own, they generally remain credible borrowers. We have seen most farmers revive themselves over 2-3 crop cycles. Their land is not going anywhere, and neither are they. They depend on the land and take what they get from it, which means recoveries are not the biggest concern.”

Behind the scenes, HBL Group management had made a conscious decision to focus more on the agricultural sector. In the years since, HBL Group has invested in sector expertise, building products that are aligned with crop cycles rather than collateral, and understanding farming as a practice rather than a credit category.

The most visible expression of HBL’s commitment towards the agriculture sector emerged in the formation of HBL Zarai Services Limited. Announced at the very same launch event, HBL Zarai Services Limited is unique in the history of Pakistani banking. For starters, it is the first time SBP has given approval to a bank to set up a fully owned non-financial subsidiary.

HBL Zarai Services Limited, you see, does not provide financial services. Its purpose is to provide facilities and services to farmers and rural communities ranging from storage space and farming equipment to seeds, fertilizer, and agronomic advice. Essentially, it is an agricultural consultancy that also doubles as a one-stop shop for the average farmer. HBL Zarai Services Limited launched its operations with a “Dera” in Burewala in February 2024. The concept behind it is simple. If Pakistan’s agriculture is to thrive, it does not just need banks to finance farmers. It also requires that farmers have access to other agricultural services that understand their needs.

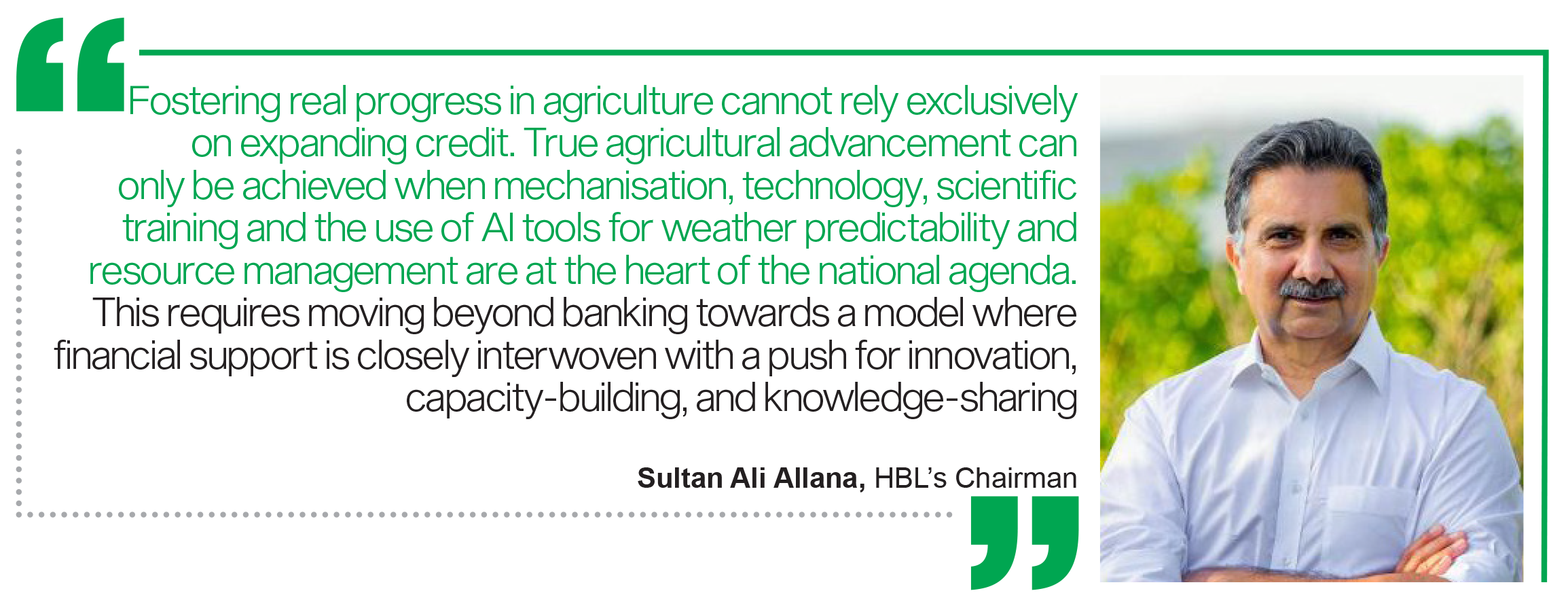

In this way HBL Zarai Services Limited acts both as a service for farmers, but also as an arm of the bank that can connect with agrarian communities and help to understand their needs. It is a sentiment that was re-enforced in a recent op-ed written by HBL’s Chairman, Sultan Ali Allana. “Fostering real progress in agriculture cannot rely exclusively on expanding credit. True agricultural advancement can only be achieved when mechanisation, technology, scientific training and the use of AI tools for weather predictability and resource management are at the heart of the national agenda,” he writes. “This requires moving beyond banking towards a model where financial support is closely interwoven with a push for innovation, capacity-building, and knowledge-sharing.”

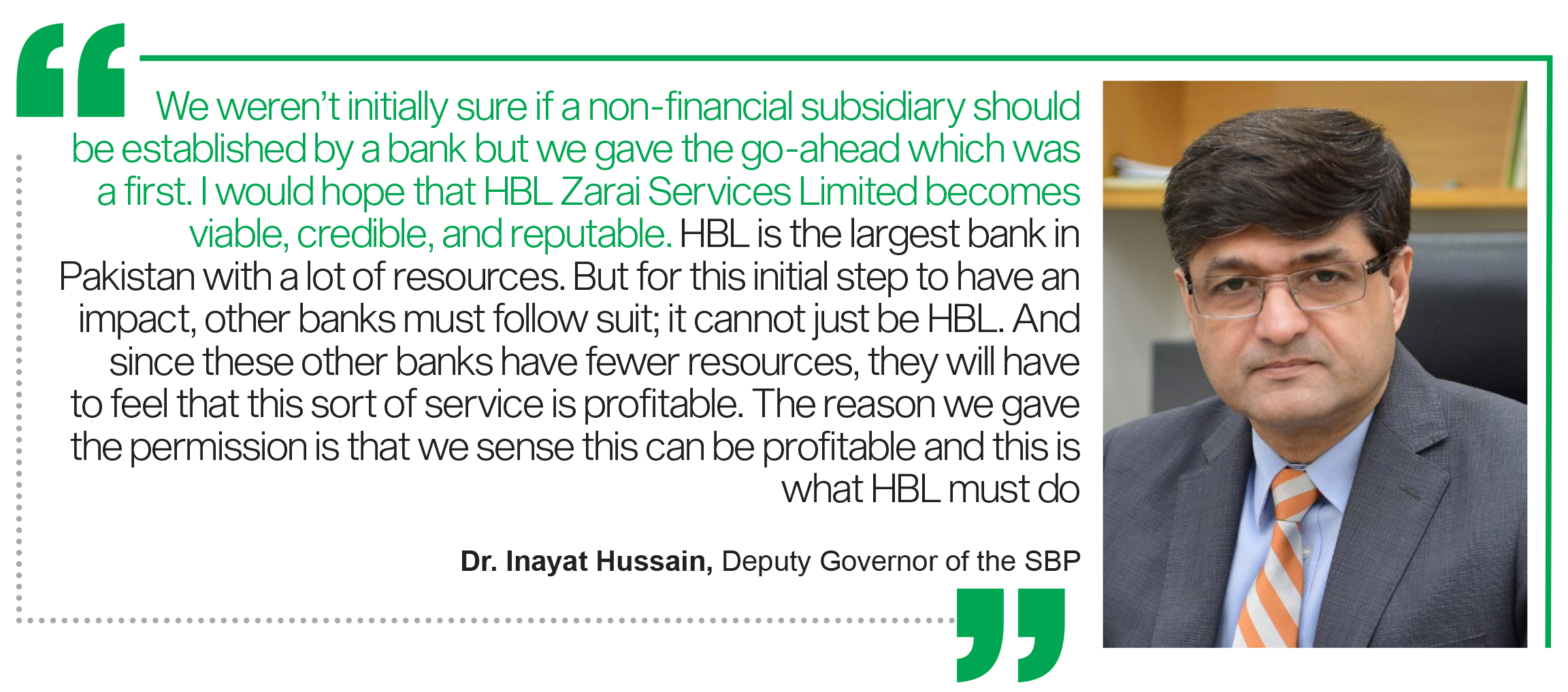

It was this spirit to go beyond just banking and credit that made HBL Zarai Services Limited such an attractive prospect and also earned it the SBP’s approval. In fact, HBL Zarai Services Limited marked an unusual regulatory departure. At the subsidiary’s launch, Deputy Governor of the SBP, Dr. Inayat Hussain explained: “We weren’t initially sure if a non-financial subsidiary should be established by a bank but we gave the go-ahead which was a first. I would hope that HBL Zarai Services Limited becomes viable, credible, and reputable. HBL is the largest bank in Pakistan with a lot of resources. But for this initial step to have an impact, other banks must follow suit; it cannot just be HBL. And since these other banks have fewer resources, they will have to feel that this sort of service is profitable. The reason we gave the permission is that we sense this can be profitable and this is what HBL must do.”

HBL Zarai Services Limited was created to solve a long-standing problem: credit alone had not translated into agricultural transformation. The bank wanted an institution capable of working directly with farmers, understanding crop and livestock practices, and providing technical support beyond the remit of traditional lending units. In conversation with Profit, HBL Zarai Services Limited CEO, Amer Aziz described it as a ‘bridge’. “The original idea behind HBL Zarai Services Limited was to bridge the long-standing gap between financial services and the actual on-ground needs of farmers. We realized that while access to finance is critical, it alone cannot transform agriculture and this vital insight led to our ‘more than just a bank’ approach,” he explains. “HBL Zarai Services Limited operates as an enabler for HBL’s agri-financing business by de-risking agriculture at the ground level. We help farmers adopt better practices, use quality inputs, and connect to stable markets; all of which improve their creditworthiness. Our on-ground teams also generate New-to-Bank agri-banking leads for HBL,” he adds.

HBL Zarai Services Limited is, to put it mildly, the beating heart of HBL’s shift towards agriculture. It is the foremost expression of intent from the bank regarding its approach towards agriculture. But HBL Zarai Services Limited is not where HBL Group’s involvement and intent begins and ends. As Sultan Ali Allana, Chairman – HBL, opined in his recent Op-ed, HBL’s strategic intent could best be summed up as ‘Beyond Banking, Sowing Change’. The Bank and all its subsidiaries are working in tandem to operationalize this strategic intent. Profit spoke with the senior executives of HBL Group all of whom spoke the same language.

How the rest of HBL shapes up

Within HBL’s own framing, this broader direction shapes its multi-subsidiary approach. In an interview with Profit, Muhammad Nassir Salim, President & CEO – HBL, explained how the different arms of the HBL Group play their part in Pakistan’s agriculture sector. “Within HBL Group, there are not one but multiple entities playing their part in enhancing Pakistan’s food security by mitigating the myriad challenges faced by the agricultural sector. Whether it’s lending to farmers (HBL), providing insurance (HBL Microfinance Bank), agronomy services (HBL Zarai Services Limited) or creating an alternate asset class for savings (HBL Asset Management Limited)”.

HBL Group – this includes the HBL Bank and the HBL Microfinance Bank – is the single largest lender to the farming community with a loan portfolio of over Rs. 100 billion.

At HBL Microfinance Bank, agriculture and livestock have become central to the business model. The institution now serves more than 176,000 agricultural borrowers and maintains a portfolio of Rs 54.4 billion, representing 56 percent of its conventional loan book. “Microfinance acts as an entry point for financial inclusion. Once a farmer gains access to a loan, they often begin using other financial services. This progression builds long-term resilience for households and contributes directly to rural development,” said Amir Khan, the HBL Microfinance Bank’s President & CEO.

“At HBL Microfinance Bank, agriculture and livestock will always remain our focus area. The growth of agriculture directly translates into the growth of the microfinance sector. Our studies indicate that while the potential client base for microfinance in Pakistan stands at around 40 million, only about 12 million are currently being served. More than half of those still unserved are directly linked to agriculture, showing the scale of the opportunity and responsibility before us.”

According to Amir Khan, insurance continues to be a big problem. “Insurance on a wide scale is the need of the hour. HBL Microfinance Bank currently offers two kinds of insurance to farmers, one is credit-linked life insurance, and the other is asset insurance of tractors financed through us. Insurance has always been important, but in the current scenario of extreme weather events, and increasing vulnerabilities, it has become absolutely critical. Farmers form one of the most vulnerable segments of society, and while insurance can protect them, many still see it as an additional cost rather than a safeguard.”

A parallel recalibration has taken place at HBL Asset Management Limited, CEO Mir Adil Rashid described the shift: “About three years ago we were a very traditional asset management company. We had a product line up that focused on fixed income and capital markets. Since then there has been a realisation that a sustainable Pakistan heavily relied on the agriculture sector. Our thinking changed. We began thinking of out of the box products that will offer diversity in financial products the industry has to offer, but also be long-term beneficial to the economy.”

“Our commodities are mismanaged,” says Mir Adil Rashid. “In the same year we end up importing and exporting the same products. On top of this the government sometimes pays these farmers subsidies. If a farmer is getting his financing needs met through informal channels and is paying 40-50% interest on these loans, of course he will need a subsidy. If the industry can service these farmers then the subsidy can be used in better ways.”

The road ahead

HBL’s leaders also connect the strategy to future market opportunities. “Everyone has a renewed and pronounced focus on agriculture in recent years. On an industry level attitudes have definitely changed”, said Aamir Kureshi. “I believe one turning point was when the country was under financial stress a few years ago.” He referenced the 2021–2023 crisis of foreign exchange shortages and record inflation, during which banks earned substantial returns on government securities due to high interest rates. That environment, he suggested, highlighted the need for more sustainable, real-economy growth”.

“Many people still do not realize that dairy and livestock form a larger part of Pakistan’s agricultural sector than crops. Historically, there has been a lack of understanding about this — both among the general public and within the banking sector — but that is now changing,” says Aamir Kureshi. “We have also observed that most crop farmers are, in fact, also livestock and dairy farmers, even if only on a subsistence level. Traditionally, agricultural financing has focused on major crops such as wheat, cotton, and maize. However, a few years ago, we began testing and expanding our presence in the dairy sector as well. Today, roughly 15% of our overall agriculture portfolio is dairy-focused.”

“There is still a long way to go. Banks must also develop a clear understanding of the livestock lifecycle, which is far more complex than traditional crop cycles. That said, we have already begun shifting our focus toward the dairy and livestock segments — particularly livestock — as it represents a larger, yet still significantly underpenetrated, opportunity within the agricultural economy.”

Still, systemic constraints remain. The average farm size continues to shrink — from 6.4 acres in 2010 to 5.1 acres in 2024 — and 97.5 percent of farms operate below 12.5 acres. Farmers have expanded cultivated area to 89 percent of total farmland, and gross cropped area has grown from 67.9 million acres to 82.7 million acres, reflecting intensified land use. Yet major crops saw a combined 13.5 percent drop in production in the most recent year.

Without crop insurance, natural catastrophe coverage or reliable water management systems, both farmers and lenders remain exposed to climate volatility. Executives across the sector argue that any long-term expansion of agricultural finance requires government participation in insurance frameworks.

Within this landscape, HBL Group’s model represents one of the most coordinated attempts by a private bank to build a comprehensive agricultural ecosystem. It combines credit, advisory services, microfinance inclusion, investment products and institutional alignment across subsidiaries.

Aamir Kureshi told Profit, this is a market where competition is not an issue. “I keep saying that the market potential and need for agri financing is incredibly high. The more banks that want to participate the better. In fact, if more banks want to come in, we are even willing to help them.”

HBL’s model is one that other banks can follow. It shows that a sustained focus on agriculture is not just workable, but it will also be good for Pakistan’s larger economic picture. And given how large the agriculture sector is in Pakistan, there is more than enough room for other banks to take the plunge.

And as HBL’s President & CEO, Muhammad Nassir Salim said, “HBL knows its role in leading the way. We’re glad to see other players now replicating different forms and versions of essentially the same model. It’s encouraging because banking-sector penetration in agriculture is still below 10%, meaning 90% of farmers remain in the informal sector. The more we equip them with modern agricultural skills — like laser levelling instead of flood irrigation or adopting drip irrigation — the more productivity will rise. These interventions can uplift Pakistan’s agricultural economy by up to 40%. They will create prosperity at the grower level and build a strong knowledge base, which is exactly what we need.”

Competition, it seems, is not the issue here. When it comes to Pakistan’s agriculture sector, the issue is survival, and there are no two ways about it.