Airlift may have hit a billion, but is it for real?

There is more than meets the eye in Airlift’s evolution from mass transit startup to a quick commerce unicorn

There is a new unicorn in town, and its name is Airlift. Profit has confirmed that the erstwhile mass transit startup will soon be announcing the $1 billion valuation. This announcement will come with another announcement that the startup has managed to raise another successful round - $350 million (approximately Rs 63 billion) this time. Add the previous $85 million they raised and their funding alone accounts for more than half of what has been raised in total by Pakistan’s startups this year.

As they sit poised to become Pakistan’s first unicorn tech startup that derives the bulk of its value from Pakistan operations, it is worth looking at how Airlift got here. In the past three years, Airlift has been conceived, been launched, raised money, been brought to its knees by Covid-19, been reimagined during the pandemic, has raised a record breaking $85 million in series B funding, and is now on the brink of announcing a billion dollar valuation and a second record breaking series of funding.

This journey has been celebrated, questioned and scrutinized. Back when they raised their initial $85 million in funding and declared a valuation of $275 million, the market was rife with rumours that there was something amiss here. Industry sources were suspicious, and soon enough rumours were abound. The scrutiny could easily have been the result of competitors being alarmed at Airlift’s significant gains which could be detrimental to their own business.

At the core Airlift is very much a story of success. That is because they have played the startup game well and have consistently managed to stay relevant and keep the money rolling in. There are, however, certain aspects of the startup playing field in Pakistan (and elsewhere) that mean there is often less to this success than meets the eye.

Beginning with their great pivot from mass-transit to grocery delivery, and going all the way down to their record valuations, this is the brief yet very telling history of Airlift. Our main characters are Usman Gul, the dedicated CEO of Airlift and Aatif Awan - the venture capitalist who took a huge gamble and now wants to see it pay off. This is the story of Airlift and all it stands for.

The evolution of Airlift

In late 2018, Usman Gul and one mysterious Daniyal Khan conceived the idea of Airlift - a mass transit system to provide an alternative to dilapidated public transportation. For the first six months, Securities and Exchange Commission of Pakistan (SECP) records show Daniyal Khan was the CEO but very little is known about him. The man is a ghost with no public profile, no mention in Airlift’s media coverage, and no Linkedin profile. After this initial period, Usman Gul took over and there has been no looking back since.

Airlift’s model was simple - they would hire privately owned buses on rent and run them through selected routes all over the cities they were operating in. The users would book their seat on these buses through the app, arrive on time at designated bus stops, and then be taken to the bus stop closest to their destination - you know, how buses work but through an app.

The idea gained some early momentum, and vast fleets of privately owned buses with the Airlift branding on them started popping up everywhere in Lahore and Karachi. Airlift offered five free rides to new customers, and during office hours these buses ran filled with salaried passengers and students commuting to their universities.

Things really started heating up around the summer of 2019. In July, Airlift got its first taste of competition when the Egyptian company Swvl entered Pakistan. Swvl, which has now been acquired in a $1.5 billion SPAC (Special Purpose Acquisition Company) deal decided to launch decentralised mass transit operations in Egypt back in 2017. It entered Pakistan after raising $42 million in June of the same year. After the SPAC deal, SWVL is somebody else’s headache now. Why it’s a headache comes below.

Swvl had raised $30 million in November 2018 and $8 million in April 2018. While Swvl did not have any immediate plans to enter Pakistan, it was probably because of Airlift’s presence that they wanted to enter the market early and not let Airlift cement its feet and let Airlift threaten SWVL in other geographies if it grew in Pakistan. The next month, in August 2019, Airlift got its first public validation as a serious business that had investors’ attention when the startup announced a seed round of $2.2 million (approximately Rs347 million) - then Pakistan’s largest seed round with participation from international investors, one of which was Aatif Awan.

Aatif is a former Linkedin executive turned investor who launched his own fund by the name of Indus Valley Capital (IVC) to invest in startups primarily in Pakistan. A little over two months down the line, Airlift scored $12 million (approximately Rs1.8 billion) in Series-A financing - again Pakistan’s largest Series-A funding round at that time, giving an impetus to the public perception that mass-transit was a serious business. The eyes were turning and international investors had started looking with interest at Pakistan. In the times to come, Airlift’s big rounds would get investor attention on the rest of Pakistani startups as well.

The round was announced in the beginning of November 2019. By October, as per numbers available with Profit, Airlift had crossed the threshold of 10,000 bus bookings per day, generating annualised revenue of $1.42 million. Subsequent injection of $12 million Series-A financing pushed bookings to over 17,000 per day in November, over 22,000 per day in December and over 33,000 per day in January, having grown over 200% between October and January.

The strategy at play here is called Blitzscaling. Derived from the German war strategy in World War 2 known as ‘Blitzkrieg’ meaning ‘lightning war’ - the term was a portmanteau coined by LinkedIn founder Reid Hoffman. The core value of the strategy is spending money to gain customers by giving incentives and cheap rates. Essentially, you are burning lots of cash, fast, to attract users to the platform in the hopes that your product will become essential to them, and competition will not be able to keep pace. Later on, when Airlift would make its quick commerce pivot, they would use the same technique. Even though this would be the technique that got their mass-transit model in trouble in the first place.

Blitzscaling makes sense on some level since it does result in rapid growth. And Airlift’s investor, Aatif Awan, was one of the key people in charge of implementing Reid Hoffman’s blitzscaling ideas at LinkedIn. But this growth then needs to be backed by solid business fundamentals and an unwavering resolve.

While Airlift was growing and showing great numbers, the problem here was that these bookings were not happening naturally. With competition heating up from Swvl and customer acquisition a constant expense, keeping up the growth and keeping Swvl at bay was coming at the expense of a cash burn of over $1 million minimum each month. Staying true to Blitzscaling, Airlift investor Aatif asked for more money in an email to investors.

In an update to investors sent on January 29, 2020, Airlift told its investors that “Airlift’s current cash runway goes until mid June, giving the company 4.5 months to secure additional capital.”

Airlift was promising its investors that they were about to strike gold if they just kept up their effort and belief for a bit. By February, the startup would have scaled to 41,000 bookings for buses, aiming to hit 50,000 rides by March. By the start of March 2020, the company had a little over $5 million in its purse which gave it a runway till June 2020.

In a scenario where Covid-19 had never happened, Airlift was going to continue operating as it was. And why would it not? Things were looking up after all. Weren’t they?

What investors didn’t necessarily know

There was nothing wrong with Airlift asking for more money from investors. There was also nothing wrong with them presenting a rosy picture. To be fair, Airlift must have thought that they were going to win the battle. What they did not tell investors, and understandably so, was that the horns they had locked with Swvl were now digging into their skull and causing serious headaches.

As mentioned earlier, the main motivation for Swvl to enter Pakistan was to not allow competition to brew in another country in the region. If Airlift had been allowed to operate freely in Pakistan, it could one day have challenged Swvl in its international expansion plans. So when Swvl raised $42 million in June 2019, the first thing it did was use some of that funding to enter Pakistan in July 2019. Sources that have worked with Swvl told Profit that they entered Pakistan in a rush to stop Airlift from possibly becoming big enough to challenge it in other geographies. This meant they entered Pakistan in a bit of a hurry, without realising that Airlift was not sure it would really break through in Pakistan, and international expansion was not even a distant dream for them.

At this point, the major cost in Airlift’s operations was on the supply side. Both Airlift and Swvl were renting out buses, and they kept raising how much they were willing to pay bus owners to try and undercut each other. In the last month before shutting down because of the pandemic, January 2020, Airlift burnt $1.54 million in cash to keep its operations afloat. Out of this, an overwhelming $1.12 million was spent on the buses and their maintenance.

Swvl did much the same, and both companies found themselves spending money in the hopes that the other would blink first and the space would be open for them to do whatever they wanted. No one was willing to bring their cost down just yet. And that is when they were both saved by the bell.

Covid-19 to the rescue?

Right at the precipice of destruction, a light emerged. Airlift and Swvl were two warriors engaged in an epic battle. Exhausted, wounded, and unable to turn away because of their egos, they suddenly found themselves with an honourable way out - a larger threat that required them to turn their attention elsewhere. Ferdowsi or Homer could not have scripted it better.

As soon as the Covid-19 pandemic hit, Airlift shut shop. They shut down their buses even before the government officially announced a lockdown and a closure of public transport. This was the responsible thing to do, but Airlift responded very quickly - almost unusually so. For a startup banking on keeping their momentum up, they did not even try to introduce social distancing on their buses and instead put an abrupt end to their operations. According to CEO Usman Gul, it was in the days right after this that the core team at Airlift realised that the business model they were giving everything to was not worth it.

Yet sources close to Usman Gul and familiar with Airlift’s idea have said that this realisation had come long before the pandemic started. According to them, Airlift’s business model was unviable in Pakistan and this was something Usman Gul and the rest of the team knew only months after beginning the company in 2019. Customer retention was low, and promising numbers like growth in new users were massive because of the discounts on the rides. This is why Airlift was not going to turn profits anytime soon - never maybe. Despite this, they were willing to plead for investor funds, convince them that their idea was working, and ask for more money to spend on their mass transit project as late as March 2020.

Why would they do this? For starters, changing course before an unprecedented event like the pandemic would have made their investors lose faith in them. Investors rarely appreciate a dilly-dallying CEO that changes course on whims and wishes. If they could not stick to their first idea, why would their second be any better? It would have needed some Don Draper-level pitch to get everyone on board. The other factor was Swvl - and the battle that the two companies found themselves inextricably embroiled in.

Add to this marketing costs, and you have a very unviable business model. Airlift realised this pretty early to some extent, and turned to the rickshaw method of even trying to rent out their buses as ad space. However, none of this was enough to stop the rot. According to sources, Airlift in its first year took a loss of over Rs1.2 billion, which testifies that the unit economics of the business were terrible.

In an email response to Profit Gul, however, conveyed that the mass-transit model continues to be an incredible market opportunity and one that Airlift is quite excited about. “Amidst Covid-19, however, we're not sure if this is the right bet to get behind. If and when the pandemic subsides, we would be very interested in re-exploring transit. The success of Swvl is a validation of the transit model,” he said.

The comment from Gul, however, comes after his earlier acknowledgment in an interview with Bloomberg that the company did not really believe in the model of selling air-conditioned bus rides through an app.

But despite that, the company was raising new funds. “Airlift has also secured $9 million of a $10 million Series-A extension on the same terms as Series A. If you'd like to participate in the remaining $1 million or can make intros, please let me know,” wrote Aatif in an email to LPs of the fund, sent at the onset of the pandemic.

“With this new cash infusion and reduced burn, the company has de-risked materially. In the meanwhile, they are investing in improving the core product as well as the routing engine that reduces empty distance and hence the unit economics. They are also experimenting with some ideas that would diversify the business so that it has some tailwinds from covid. I'll share more on this in due time,” he wrote further.

Airlift and Swvl were either too proud or too scared to tell their investors this was not working out. And since Swvl had more money than Airlift, the latter was more desperate and continued to ask for more money despite knowing that it was a lost cause. Covid-19 provided the perfect cover. It gave Airlift a second lease on life and the rare opportunity in the startup world to go back to square one. Airlift would now not come across as wayward, but quick on their feet. Innovators not dreamers.

The pivot - who is really in control?

The pandemic appeared as a blessing that allowed both Airlift and Swvl to pivot gracefully. Very quickly, before even waiting to see how the pandemic would play out, Airlift moved into groceries while Swvl added to its services and started providing mobility solutions for corporates and intercity travel for consumers.

However, as the pivot panned out, questions started to emerge over who was in control of Airlift, the CEO or Aatif Awan? As an investor, Awan was actively involved in the company, sources allege, even when he wasn’t supposed to be. He was holding daily phone calls with Gul, discussing the pandemic, and finding new investors. Gul allegedly exhibited a desire to keep investors happy and let Awan steamroll him.

Airlift has denied this, saying that Airlift’s strategy has been led by the team. “Airlift operates on a decentralised decision-making framework, one in which decisions are made by those closest to the information”. Furthermore, Gul said that the investors were partners on the capital markets front and were not involved in operating the business and/or formulating strategy.

Awan’s interest is natural. Airlift is one of the core investments of Indus Valley Capital and in Airlift he has invested in his personal capacity as well. ACRA filings show that Awan owned 11.21% shareholding, not much less than CEO Usman Gul’s 11.8% until Airlift’s Series-A round. Aatif and the fund he manages own around 21% of the company, making them collectively the single biggest shareholders in the company out of 52 listed shareholders and investors.

It is not the wildest stretch to say that the pivot towards grocery delivery was thought up by Aatif Awan, and that he is the one pulling operational strings. Awan has long been interested in the quick commerce business. He had previously been involved in talks to invest in a grocery delivery startup a few years ago and had an idea of what the business required.

Insiders and people from the grocery startup in question have gone so far as to say Aatif Awan used his past knowledge of the startup he was willing to invest earlier into to gain valuable insights into the company. That claim is one that cannot reasonably be ascertained or be a cause for blame. The tactics sound more coincidental than underhand. But they do point to one thing - Aatif Awan has more than a little operational pull at Airlift. Profit reached out to Aatif for comments, who said that much of the information, without specifying which bit, was false. On the other hand, Gul remained quiet on a question about Airlift’s pivot towards grocery delivery.

The valuation blackbox

On July 1, 2020, Airlift officially announced moving into the grocery delivery business with another investment of $10 million in an extended Series-A round. Under the new model, Airlift would be setting up its operations to make swift deliveries through a network of dark stores to deliver groceries in a short span of 45-minutes under the quick-commerce model. A few months later, the grocery delivery promise was reduced to 30 minutes.

Just over a year later in August 2021, Airlift announced raising a record $85 million in Series-B funding, and a valuation of a little over a quarter of a billion dollars ($275 million). Within the industry, claims that the company had misrepresented its numbers to investors to secure a big amount at a big valuation came quickly on the heels of the announcement.

Sources with knowledge about how quick-commerce works say that Airlift’s claims to investors are not possible. Sources inside Airlift also say that Airlift’s claim was exaggerated. A prominent supplier of one of the large FMCG company’s products also said that Airlift’s procurement from them was less than others.

The company then was not valued at $275 million (as claimed) and instead only negotiated a valuation cap of $275 million with the investors - all of that based on growth that it had been able to show to investors. According to Airlift’s pitch deck presented to investors ahead of the Series-B round, and available with Profit, Airlift claimed to have reached annualised GMV of $27 million for the second quarter of 2021. The GMV number was also confirmed by Gul in an email response to Profit. Gul further said that Airlift had exceeded $50 million in annualised GMV as of September 2021

The increase in the GMV was 175% more than the GMV in the first quarter of 2021, which was reported to investors at $9.8 million. On a non-annualised basis (the actual GMV for the quarter), that’s $6.75 million for the second quarter made in three months (April-June 2021). Airlift claimed to its investors that the average order value for the quarter was Rs1,285. Market sources say this number is problematic (read, too high) to claim.

The quick commerce model is one in which the average order value is small. Airlift categorises itself as a quick commerce delivery for all household essentials. But billboards put around in Lahore and other advertisements on social media have been around groceries more than other categories such as electronics. And when it comes to groceries, quick commerce is about instant fulfilment, meaning you require the product instantly.

These are small value products and operations are set up according to that. So when Airlift says it is between Rs1,285 or $7.70 average order value, it means that most of the customers are ordering large value items which is not the way quick commerce operates. People familiar with quick-commerce operations believe that is not possible. For context, pandamart, which is bigger in terms of scale than Airlift and processes more orders daily, then had an average order value of around Rs750.

A higher average order value is possible if there are big orders, and big orders are placed on both Airlift and Pandamart by the very neighbourhood stores that these startups are out to disrupt. In our survey of the neighbourhood convenience stores, store owners told Profit that enticed by the discounts, they buy from Airlift themselves and because they are buying for the purpose of selling, the orders are large, running in thousands of rupees, which can inflate average order value. Market sources claim that Airlift delivers approximately 30% of its orders to stores.

Of course there would be some consumers too that would once in a while order large value items but the frequency of such orders would be less. An insider at Airlift told Profit that the average order value of Airlift in Q2 2021 was around Rs1,000-1,100, but fell when the company expanded into smaller cities like Gujranwala and Sialkot in July. The purchasing power in these cities is low as compared to KLIs (Karachi, Lahore and Islamabad) and would hence skew the overall average order value.

Moreover, Profit has observed over time that the company added high-price items such as mobile phones, protein shakes, and vape kits, worth thousands of rupees, which are also beyond the scope of being household essentials. A single purchase of any of such products, available at discounted rates on the Airlift app or website, can easily move the average order value up.

Even if we believe that the company’s average order value was as it was claimed, it would mean that to yield $6.75 million GMV for the quarter, it would require 9,633 orders per day. In its investor presentation, the company claimed that it was doing over 10,000 orders per day when it was operational in three cities only.

The source at Airlift corroborated to Profit that the 10,000 order number was exaggerated and that the company’s average orders daily would be around 5,000-6,000 per day on average. “Orders have gone through the roof from August onwards. There has been a massive increase in volume and the company has increased its presence and warehouses many times over. But in the months of April, May and June, we did not even have many warehouses,” says the source.

Our source further says that Airlift had an estimated 8 dark stores overall in April, 10 in May and 12 in June. On average, a dark store delivers 500-600 orders per day, which averages to 5,000-6,000 orders. Think of this another way: pandamart had 20 dark stores in Karachi, Lahore and Islamabad in May 2021 and delivered 13,993 orders per day. It had 28 dark stores in June and was doing around 14,600 orders per day. So Airlift with less dark stores than pandamart claiming to be delivering more orders on average is an unlikely scenario.

On the other hand, a supplier of two of Pakistan’s prominent FMCG companies also said that Airlift’s procurement from them was less than others. This is what the market is crying foul about; that Airlift secured a huge investment with questions around the authenticity of its numbers.

How did they show growth to investors?

For investors, the company growth shown to them to secure the investment is not what it seems. If Airlift was doing 5,000-6,000 orders per day instead of the claimed 10,000 plus daily orders, even at the $7.7 (Rs1,285) average order value, the total GMV for the quarter would be somewhere between $3.5-$4.2 million, which is slightly above half of what is claimed. On an annualised basis, it would come down from $27 million to only over $14-16.8 million.

But with the earlier mentioned discrepancy in the numbers, it became apparent that investors had been convinced that the company was worth investing in and hence a massive round was raised. In a tweet on August 18 this year, Harry Stebbings, one of the investors in Airlift’s Series-B round, cited “far superior unit economics than western models” as one of the reasons he invested in Airlift.

The problem is that if the numbers are not what they really are, the unit economics falls apart and investors' expectations of growth are less likely to pan out. Add to that the Series-B round was raised as SAFE investment, according to an investor email seen by Profit, a thorough due diligence might not have been done by most of the investors.

The investors in the round are said to be mostly angel investors, without participation from a prominent VC. Because names like Harry Stebbings and Josh Buckley had participated in the funding round, this becomes a situation where investors are willing to put in money because they see others putting in money.

Together with the growth it was able to show, this is also how Airlift was able to negotiate a valuation cap of $275 million. In an interview with TechCrunch, Airlift CEO Usman Gul claimed that the company’s valuation following the $85 million round was $275 million.

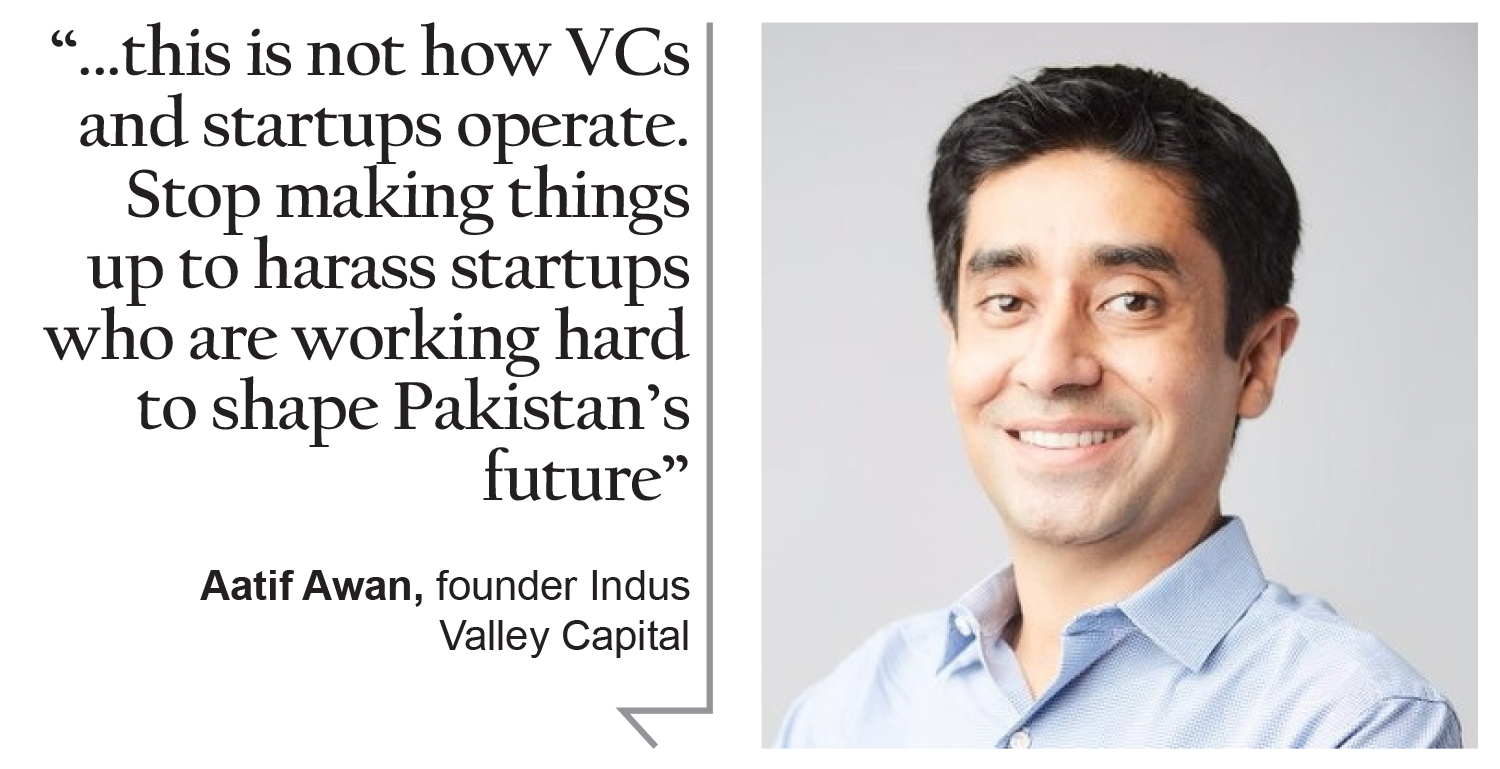

Profit reached out to Aatif to seek comments about Airlift continuously raising funds for mass-transit business despite the business not holding great potential, his unusual involvement at Airlift, the pivot towards groceries, and the allegations of misrepresentation of numbers. “Much of above is completely false,” Aatif said in a WhatsApp message.

When asked what was false precisely and what was true, Aatif said: “All of it is either false or does not make any sense as this is not how VCs and startups operate. Stop making things up to harass startups who are working hard to shape Pakistan’s future.”

A subsequent request was made for an interview but no response was received from Aatif.

Profit reached out to Airlift to verify the authenticity of numbers claimed to investors, and about Airlift’s pivot, raising funds for the earlier business despite the little promise and Aatif’s involvement. Gul responded to all as factually incorrect and, in particular, said about numbers claimed to investors that “Airlift operates on an open data infrastructure, which means that Airlift investors have real-time access to the internal data systems.”

This would mean investors can see what is going on at the company, the order numbers, and value, if there was something wrong, the investors had the means to know it right away. This is where the waters get a little murkier.

Information rights of startup investors are usually restricted to monthly or quarterly reports and access to granular information is not given. Why? Because investors have vested interest in adding value to the investments that they make from their fund and startup founders are unlikely to grant granular level access to investors to keep them from using the information in case investors end up turning to a competitor.

A couple of startup investors Profit spoke to said that under the information rights, it is highly unlikely that all investors would get such access, especially the ones that are low-ticket investors. They called Airlift’s claim that its investors had access to internal systems mostly a spoof. They did, however, confirm that investors under their rights can ask for an immediate audit of the company.

Only one set of investors, however, are most likely to have such access: ones that have put a lot of money into the startup and occupy a seat on the board. Aatif Awan is one of the two investors that we know of who occupies a board seat at Airlift. Harry Stebbings, who joined the Airlift board following the Series B investment, is the second board member.

Profit reached out to multiple Airlift investors to confirm CEO Gul’s claim whether investors had live access to Airlift’s internal systems or not. None of the investors responded to queries regarding this.

Profit reached out to Airlift again requesting access to the same systems to reconcile the numbers claimed to investors, offering to sign a non-disclosure agreement to protect the confidentiality of the company, and also offering to publicly put down rumours of alleged fudging of numbers to investors, if the claimed numbers could be reconciled with actual numbers. The access was denied to us.

Instead, Profit was served a legal notice by Airlift, and Aatif Awan. The notice claimed that by asking questions and trying to ascertain the claims of numbers being fudged, Profit had caused damage to their reputation. Profit has responded to the legal notice.

[Editor’s note: During the drafting of this story, Airlift approached Profit to inquire about a marketing arrangement. No such arrangement was entered into.]

After this, a letter has also been circulating amongst Airlift investors claiming Profit is publishing a story because of a rejected marketing proposal, even though it was Airlift that approached Profit for such an arrangement. Airlift and its investor are free to offer an explanation of how the numbers reconcile and we will promptly publish their explanation and revise our story accordingly. However, as of the publishing of this story, which has been months in the work, Airlift has refused to respond to the allegations.

The valuation kerfuffle

Airlift chasing a billion-dollar valuation is because quick commerce startups around the world have been able to get very high valuations in record times. They have also been able to raise very high sums of money because quick commerce picked up during the pandemic. Europe’s Gorilas and Flink, US-based JOKR, and Turkey’s Getir all became unicorns this year along with massive rounds raised.

How startups get valued during a funding round depends on what sort of valuations peer startups are getting around the world. Quick-commerce is hot around the world and there is a demand for such deliveries because of the pandemic, which means there is going to be growth. Other startups have been able to grow and have raised funds at massive valuations, which for Airlift means that if it is also able to show growth, it would be able to get a similar amount of funding at internationally comparable valuations.

Pakistan has a massive population of 220 million and if Airlift is able to show growth in Pakistan very quickly, investors would be willing to invest high amounts of money and give them a bigger valuation. Airlift’s pitch of international expansion has also been similar to other startups in quick commerce that have become unicorns and with all of that combined, it isn’t surprising that Airlift was able to raise $350 million and get unicorn status.

There is a strong case to be made here that Airlift kept its actual numbers under wraps ahead of the $85 million investment, which means that future projections of the GMV and unit economics also fall apart.

The bet is risky. Is it worth it?

If Airlift is able to grow big enough at the end of the day to do a massive number of deliveries to consumers and/or stores, the volumes alone would put it in a strong position to go back to manufacturers to negotiate discounts and better margins for Airlift. The revenue for startups like Airlift comes from the difference in the sale price and purchase price. So if Airlift, on the back of large volumes, is able to negotiate a lower purchase price, its unit economics turn favorable, and might turn the business profitable sooner rather than later.

It has strong competition in pandamart which would pull down Airlift’s growth and could only be dealt with if Airlift had more money. Market sources tell us that Airlift’s orders currently stand at 17,000 daily from around 30 warehouses, whereas pandamart has scaled to 50 dark stores and is currently doing 22,000 orders daily.

Disruption of neighborhood convenience stores is also difficult. In a survey carried out by Profit of around 50 neighbourhood stores located in high-income neighbourhoods, such as DHAs in Lahore and Karachi, most of the shop owners said that they had not yet seen any decrease in sales because of delivery apps like Airlift and pandamart. Only a handful of stores that did say their sales had declined, saw a slight decline but were unsure if it was because of the apps or because inflation had increased. They had seen a similar decline in sales in earlier periods of inflation. Moreover, all of them had their delivery service and delivered orders in the neighbourhoods they served by taking orders on phones.

Pakistan is going to form the bulk of Airlift’s operations because, in contrast to Pakistan, Airlift’s dark stores in South Africa, the only country Airlift has yet expanded to, are estimated to be 9. So the bulk of the value for Airlift’s business is coming from Pakistan. South Africa would also not be an exciting market for investors and growth potential would be limited given that South Africa’s population is only 59 million, which is about only a little over a quarter of Pakistan’s.

Who is responsible?

The question is, who is responsible for concerns surrounding the accuracy of numbers? One obvious person to whom attention turns when this question is asked is the CEO. He has to earn a return for himself and investors more than himself from whom millions of dollars worth of investment were secured. It is going to be a terrible legacy for Gul to have failed a startup that raised multi-million dollars in funding. On the contrary, it would be a great legacy if Gul created a Pakistani tech unicorn in a record-breaking period.

On the other hand, a strong case is to be made that Aatif Awan knew all along what was happening and was involved in what was happening. There are obvious blueprints of Awan working closely with Gul during the pandemic, his involvement in how the company pivoted, and the likelihood of him having access to Airlift’s internal systems.

The incentive for a fund is also clear: a fund manager has to generate returns for investors in the fund. So if Airlift is able to get a $1 billion valuation now and exits later at an even higher valuation, the fund that invested would get better returns to investors than if the valuation was low. Moreover, it is in a fund manager’s interest to pump money into a startup that is doing well. So if Airlift is doing well on the back of inaccurate numbers, the fund manager has a cause to invest more from the fund into that startup because it is doing well. And as more funds are deployed to a single startup that is doing good, the fund manager can close the fund quickly and raise a new fund.

The management fee alone of these funds can turn out to be pretty big. Because any exits are going to happen over a 7 or 8-year horizon, it is the fund management fee that the manager gets as compensation. The management fee is usually 2% of the size of the fund, per year.

As mentioned earlier, the exit for a company is going to come after a few years and during that time, the manager can deploy multiple funds and earn hefty management fees each year. So even if the startup fails, the fund manager will still make good money.

Was the investment in Airlift worth making a further investment? Aatif would think so. In an email sent to Indus Valley investors, Aatif offered to set up an SPV (special purpose vehicle) to make an investment into Airlift’s Series-B round. The fund could not make an investment directly because it had reached a concentration limit for the Airlift investment, but had an allocation to invest in Airlift because of its pro-rata rights.

Pro-rata rights are rights an investor has to keep up his shareholding in a company in later financing rounds. Investors usually exercise pro-rata rights in companies that are doing good. But in the case of Airlift, there was no mention in funding announcements of any prior investors, like First Round Capital or Shorooq Partners, following on in the Series-B round.

The email also mentioned that most of the earlier investors, including Indus Valley Capital were taking their pro-rata in the Series B round. Clearly, IVC has a vested interest in Airlift but prior investors not exercising their pro-rata rights means they do not consider it to be a good investment anymore. Who took their pro-rata rights, except IVC, is unknown. But if a VC like First Round Capital did, it would have been worth mentioning in the email because it would have given confidence to other investors too.

If in fact, this is a case of misrepresentation to investors, two possible names come to mind. CEO Gul and investor Aatif, who could have done it in cahoots with each other. In any case, the investor is most likely to get away from it unscathed, and that too with some money, because of a disclaimer: “While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy,” Aatif wrote to investors in the same email in which he told them how Airlift was doing great with $27 million in annualised GMV and over 9,000 order per day.

That one email in and of itself says a lot about how Airlift has gotten where it has. When the startup revolution happened in Pakistan, the expectation was that with young, bright minds coming to the fore this would be a clean, open, slate where things could be built. Even Airlift should not be immune to questions on the property of its numbers. More than anything else, the worrying part is that it has also proven it has something to hide and that it does not want to open up about it no matter what.

The author is a staff member and can be reached at [email protected]

View all articles →23 Comments

No comments yet. Be the first to join the discussion!