Every day, the call to prayer is made five times a day to remind you of your obligation to pray. Every year, announcements regarding the beginning of the Holy month of Ramadan and Zill Hajj remind you of your religious obligation to fast for a month and perform Hajj at least once in your lifetime, depending upon your financial situation.

However, in the case of Zakat, the announcement is a little more understated. There is no announcement on the mosque speaker and no committee to come on television and remind you of this religious obligation. The only reminder comes from the government of Pakistan when it announces Nisab each year, which is a minimum rate that is used as a threshold to determine if Zakat is obligatory on you.

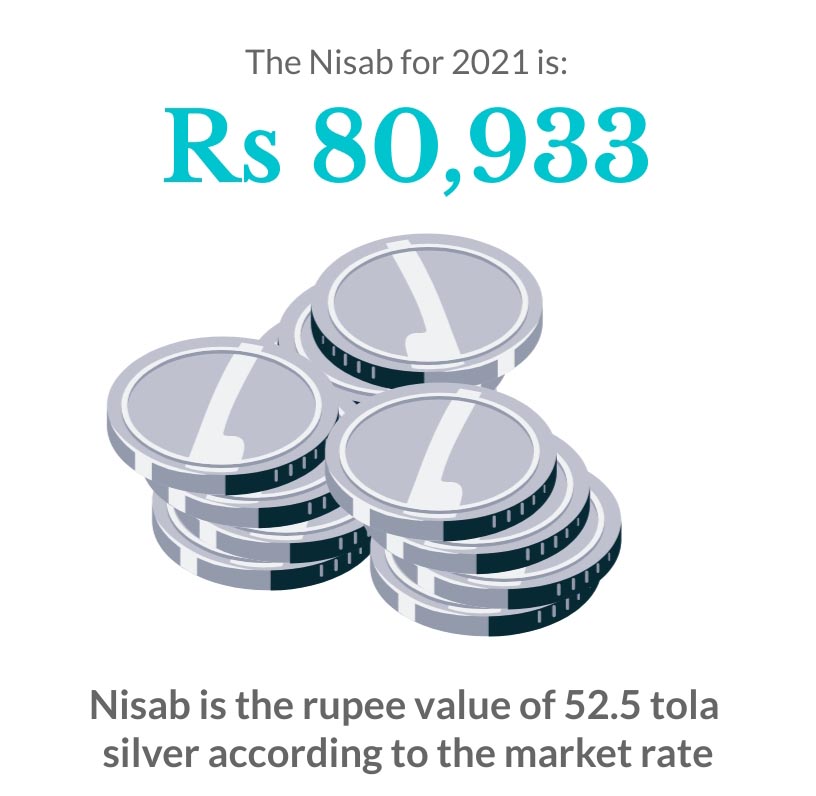

For this (lunar) year, the government has fixed Rs80,933 as Nisab for Zakat. Based on interviews of Islamic scholars, Profit explains what is included in Nisab and how you can calculate your Zakat obligation.

Working definitions and calculations

While the government has fixed the Nisab limit, quite simply, Zakat is obligatory on each and every Muslim who is in possession of wealth and income that is equal to or greater than the Nisab limit. Each Muslim, if they want to find out if Zakat is obligatory on them, therefore, has to calculate their own zakatable net-worth (ZNW).

ZNW can be calculated individually by simply calculating the difference between the value of one’s zakatable assets and one’s zakatable liabilities (explained later). For instance, if person A owns assets worth Rs100,000 and their liabilities are Rs10,000, the difference between their assets and liabilities comes out to Rs90,000, which is that person’s zakatable net-worth. Since this value is greater than the Nisab limit set by the government, Zakat is obligatory on this person.

However, there’s a certain distinction between the assets on which Zakat is due. While calculating ZNW , all forms of assets cannot be accounted for. For the purpose of Zakat, the following assets are to be considered normally i) gold and silver, ii) currency in any form iii) tradable goods. (Livestock and agriculture produce are not covered in this article, as they entail special treatment).

Gold and silver is zakatable in all forms, for whatever reason it is owned, whether it is under use or not – so this includes any gold and silver jewelry if it is worth more than the Nisab amount. Zakat is also due on any currency you hold, whether it is savings in a box at home, bank deposits, or money that you have lent to someone. It also includes committee savings, money that is saved for Hajj or marriage, and bonds. Essentially any cash that you are holding without the intention to spend it has Zakat due on it. The third category is trading goods. This is a little more complicated to categorise, and for this the conscientious person must peruse their intentions more closely. For the purpose of Zakat, anything would be considered a trading good if it was acquired with the purpose of reselling it. So if you buy a plot, for example, with the sole intention of selling it in the future, that piece of real estate is a Zakatable asset. The value of such assets is calculated on the basis of their approximate sale price rather than their purchase price. However, if the intention for buying was to one day use the real estate, or to simply park excess liquidity in a long term asset with no intention of selling it for now, it would not become part of the zakatable net worth.

Receivables in all forms also need to be included for calculating zakatable net worth. Though for receivables that you are unsure about if they would be received or not, deferring is allowed and when these receivables are collected, paying Zakat would be applicable for the previous years as well.

Similar to receivables that are doubtful, bad debts, which are receivables that have close to no chance of being recovered, can be also taken out of ones ZNW calculation, but with one extra distinction: If a bad debt is recovered, Zakat on it will not be due for the previous years.

Liabilities can range from short-term liabilities to long-term liabilities. Few examples of liabilities can be loans taken for personal use, utility bills, employee salaries, Zakat for previous years. It also includes committee installment if the committee savings have been collected in full already. Liabilities can also come in form of taxes payable to the government or installments for goods that have been purchased.

For the purpose of accounting Zakat, only liabilities that are payable immediately are considered. For instance a loan installment that is due when you are calculating your Zakat obligation. But if you have a liability of a loan that is due next year, it can not be accounted for calculating Zakat in the present year.

A particular distinction is made about loans that are taken to procure raw material for production of trading goods. These loans are considered liabilities and can be discounted while calculating Zakat. Whereas loans procured to buy fixed assets can not be discounted.

So this is the very simple formula. You look at your assets and whether or not they fit any of the five categories on which Zakat is due, and then you calculate your liabilities. Subtract the liabilities from the assets, and if the amount you have left is over the Nisab limit set by the government, then you will have to pay 2.5% of that amount as your Zakat, which is the standard rate.

Let us take an example. Assume you have savings worth Rs100,000 and you possess gold worth Rs100,000 and you have no outstanding receivables. Both savings and gold are zakatable. On the liabilities side, you have, let us say, Rs15,000 in utility bills, Rs15,000 again in children school fee and another 15,000 in loan payment that is due immediately, your total liabilities would add up to Rs45,000. Your ZNW would be the difference between the value of assets and liabilities, which in this case is Rs155,000.

Since Rs155,000 is above the Nisab limit of Rs80,933, Zakat is obligatory to pay. Going by the standard rate of 2.5% (which is applicable not on the Nisab limit (Rs80,933) but on the individual Zakatable net worth amount (Rs155,000 that you calculated), the amount due in Zakat for this person would be Rs3,875 (2.5% of Rs155,000).

(Note: In case Nisab is not fixed by the government, the standard rate is the rupee value of 52.5 tola silver according to market rate. In case a person only possesses gold and has no other asset, the Nisab rate in that case would be rupee value of 7.5 tola gold)

On calculating Zakat for businessmen and shareholders

Paying Zakat each year is a very personal and sacred process for Muslims. Of course, there is no Zakat due on a company or an organization, because businesses do not have a faith and are exempt from this kind of religiously mandated taxation. But most of the time, questions that come to religious scholars are about jewelry, and real estate and savings. However, while businesses do not owe any Zakat, for the people that own them the net Zakatable assets of the businesses would become part of their individual ZNW.

Let us start with the case of a business that one own’s partially or fully. In case of a medium size business structured as a partnership or a private limited company, for instance, Zakatable assets are going to be computed based on one’s shareholding in the business. So if you own a company and hold 51% of the company, whereas your partner holds the remaining 49% of the company, how will Zakat be figured out? The calculation is simple. If the company has current assets worth Rs 50 million and current liabilities worth Rs25 million, the total value of Zakatable assets would be Rs 25 million. The Rs 25 million would be paid off according to ownership percentage. You (with 51%) would be required to pay Zakat on Rs 12.75 million, which amounts to Rs318,750 at 2.5%. Your partner (with 49%) would be required to pay Zakat on the remaining Rs 12.25 million at 2.5%, which comes out to Rs306,250. And in case the business is owned completely by one person, Zakat would be calculated on 100% ownership.

Then there are instances, like in the case of publicly listed companies, that shares are bought that also reflect ownership in the company. If you are a shareholder in a company, Zakat is obligatory on you regardless if you have bought shares for the purpose of trading or if your intention is to keep the shares and receive dividend income on them. In the case the shares were bought to trade, ZNW is going to be calculated on their market price. This means that your shares are like other tradable goods and their Zakat value is what the market price of these shares is.

For instance, if you are a shareholder in Engro Corporation and own 100,000 shares that are in your possession on the date Zakat is due, Zakat would be applicable at 2.5% of the market value of these shares. For more clarity, if your Zakat is due on the 3rd of Ramzan. The closing price of Engro Corporation’s share for the 3rd of Ramzan was Rs289.10 per share. For the 100,000 shares of Engro Corp that you own, the cumulative market value of these shares based on the closing price on the day your Zakat is due computes to Rs28.9 million. At 2.5%, Zakat on these shares comes to Rs722,750.

Things become a little different, however, if you purchased these shares with the intention of receiving dividends at the year end. Zakat in this case would be calculated based on the zakatable book value of the shares rather than the market value of these shares. In this case, for the purpose of calculating Zakat, the Zakatable assets of the company need to be calculated after discounting the Zakatable liabilities of the company to compute Zakatable value of the share you own.

Roughly, the difference between the current assets of the company and current liabilities would give the value of Zakatable assets of the company. Let’s take the case of Engro Corporation again. The value of total outstanding current assets of Engro as per the latest annual report 2020, is Rs226.5 billion. Whereas the total outstanding current liabilities of the company are Rs143.26 billion. The total Zakatable value of the company comes to Rs83.24 billion.

The Rs83.24 billion amount, however, is of the total outstanding shares of the company. A simple division would yield the value of the individual Zakatable share. In the case of Engro Corp, the total number of shares as on December 31, 2020, are 576.1 million. Based on these numbers, the value of a single share comes out to Rs144.4. Since you, as an individual, own 100,000 shares in the company, the total monetary value of your shares that are Zakatable would be Rs14.4 million. That is the amount that is Zakatable at 2.5%, which comes out to Rs361,000.

(Disclaimer: The calculations above represent the general framework around calculating Zakat in simple cases. The case of Engro Corporation in this piece is used as an example to illustrate the general framework around calculating Zakat if you are a shareholder in a public company. The case of companies like Engro Corporation is a little nuanced, however, since such conglomerates further have ownerships in other companies. Therefore, it is best to consult a shariah scholar to understand any nuances in individual cases before undertaking any calculations and giving Zakat)

When is Zakat due?

It is a little tricky pin this one down, especially if you haven’t been paying Zakat while you have been making assets for yourself. For instance, if you are thirty years old but started earning from the age of 20 and made assets on which Zakat is due, the date on which you first time became Sahib-e-Nisab, that is achieved enough wealth that Zakat was obligatory on you, is the date you should pay your Zakat each year.

So if a person became Sahib-e-Nisab on the 1st day of Muharram, each year onwards, his Zakat obligation would be due on the 1st of Muharram. It is on this day that he should calculate all his assets and liabilities. It is important to note that Zakat date is to be determined according to lunar years. All the gains in wealth prior to this day would be accounted for in the calculation of Zakat, whereas all the losses the day after would not be deducted from Zakat. Therefore, it is important to monitor one’s career progression and when for the first time a person becomes Sahib-e-Nisab.

However, it might be a little difficult for some people to ascertain when, for the first time in their life, they became Sahib-e-Nisab. Scholars consulted for this piece said that in case a person is not able to remember the exact date, he or she should take an educated guess around when they might have for the first time become Sahib-e-Nisab. For instance, when someone received his first salary might be the day when Zakat became obligatory on them. For some women, it might be the day of their marriage when they received dowry from their parents and Zakatable assets like gold or silver came into their possession.

It is only in the case that someone has not even the slightest idea that when was the first time he or she became Sahib-e-Nisab that the person can arbitrarily choose a date in the Islamic calendar to be the date when he pays Zakat. Each year onwards, he would calculate zakat obligation on the same date.

It also goes to dispel the notion that Zakat should only be paid, as beliefs exist, on the 1st of Ramzan only. No, Zakat can be calculated on other dates as well, depending on what date the person has chosen for himself in case he does not remember when was the first time he became Sahib-e-Nisab.

However, there is a condition under which the date can change. The Zakat date can be changed when a person goes totally bankrupt and is not Sahib-e-Nisab anymore. In this case, his Zakat date would be the date when he becomes Sahib-e-Nisab again.

Editor’s note: This article is based on interviews of scholars of the Sunni Hanafi school of jurisprudence, which is followed by the majority of Pakistanis. For specific questions please write to us at [email protected] and we will try our best to get these answered by competent shariah scholars.

MashaAllah great explanation

Zainab online Quran learning institute is one of the Pakistan’s most prestigious academies which offers Quran online reading classes to people all over the world. In the meanwhile, we are here to teach the Quran to you and your child. So that they can easily understand Allah’s message. This is the Best online Quran reading institute in the field of education system comparatively to others. Finally, If you want to success in whole life then it is very important to recite Quran by heart and word by word. Hence, Our teachers are well-trained and experienced in teaching the Quran to you and your child. Thus, Your children will benefit from both male and female teachers.

We are the online Quran Academy providing the platform for those who want to learn Quran online. We have both male and female teachers available who can teach you Quran online. Our teachers are well trained and experienced. We are providing different courses for students who want to learn Quran online. Nazara E Quran, Kalma and Namaz, Tajweed and tafseer.

Online quran academy, Online Quran learning, Online quran teaching, online quran teachers, online quran tutors, online quran teacher, kalma and namaz, tajweed and tafseer, tajweed, tafseer.

hydraulic cement

termite shield