Buy now and pay later with a twist - no extra charges

Platforms like QisstPay are trying to solve cash cycle problems for prospective shoppers

It’s a Sunday night. You’re sitting at your laptop and you’re browsing through the website of some clothes retailer or looking at shoes. You spot something you really like and suddenly you’re mesmerised. It’s a shirt, or a pair of shoes, an imported chocolate, or an alarm clock for that matter - it could be anything really, that bit doesn’t matter. What matters is that you want it, and sitting at home on Saturday just window shopping online your finger is absolutely twitching to move the product from the shopping cart to check out.

What do you do? You move towards the button that says ‘BUY’ and you stop yourself. No, it is the end of the month and there are a few more days until you get paid. And the rent is due first and you still haven’t paid your internet bill. The few thousand rupees you’ve got left in your account are to get you through the next pay day. You whinge but you do the sensible thing to empty the shopping cart. You shut your laptop and go to sleep, and that impulse buy you almost made will now forever be lost.

Somewhere in some ecommerce headquarters, a marketing or sales person died a little on the inside when you emptied your shopping cart and made the smart decision. Because last minute hesitancy while shopping is a serious problem for ecommerce retailers and platforms.

It happens to everyone of course. But that is a lost sale for a merchant because you have to manage your finances according to your pay cycle and in this setting, you lose and the merchant also loses.

Cart abandonment is a big problem for eCommerce merchants. Globally, the percentage of customers that add products into a cart but do not complete the transaction is roughly 70%, meaning that out of every 10 orders that are added to the cart, only 3 are actually purchased. According to an official at one of Pakistan’s big fashion retailers, the cart abandonment rate in the apparel industry is 50%, whereas the checkout abandonment rate is 20%. Checkout abandonment is when a customer has initiated the checkout process but leaves the website without completing the purchase.

The rate for cart abandonment and subsequently checkout abandonment, will certainly decrease if consumers have more buying power in general, or if a service that gives them an option to ‘Buy Now, Pay Later’ facilitates the transaction by reducing the initial payment and spreads the rest over a period of time.

This is what startups like QisstPay are trying to introduce. But this is not the kind of Buy Now Pay Later (BNPL) system we are used to in Pakistan, because there is no interest or additional cost charged. Instead, the BNPL apps make money because websites where you use BNPL platforms to purchase an item are benefitting from getting the sale immediately and give a cut to the apps - which is how they make money. Will it work in Pakistan? Profit investigates.

Not what you’re thinking

At least as a term, BNPL is nothing new in Pakistan. For high value items like motorbikes and cars or even electrical appliances like air conditioners, we are used to this system. Goods traders offer consumers electronic products, cars, bikes and expensive household items, which a family on a budget would not be able to afford to pay for in one go, installment plans to make the purchase more affordable. A low initial upfront payment would get you the product and the rest would be spread over a period of weeks or months. To avail this facility, however, the trader might require a few people to vouch for you so that in the case you default, the trader could recover the amount from the guarantors.

The catch here for the trader is that he is going to charge you a certain percentage on top of the original amount of the product for financing your purchase. The actual amount you pay as financing cost could be ludicrous, which increases consumer’s debt burden, crippling purchasing power in the longer run. Buy now, pay later, is financed by banks as well with the same arrangement in place. They charge the consumer an interest amount as a cost of financing that purchase on top of some additional charges like processing fees. Likewise, credit cards can finance purchases at zero rate but if the credit card payments are rolled over, charges can go up exponentially.

Now you see this draws up a rather sorry picture of the Pakistani consumer. They have a low disposable income in a country with soaring inflation rates and only a few financing options if they have to make a hefty purchase. They end up relying on this kind of BNPL system popularly known as ‘qistain.’

In fact, for the moment, forget financing options for big purchases. Most people in the low income bracket are not able to afford making purchases in one go for everyday consumption items such as groceries. People end up having to split their expenses in small purchases throughout the month for effective cash management to make things go smoothly for the family money-wise.

But the startup concept of buy now, pay later is different. The above examples more or less fall in the definition of consumer financing that has an interest element, or rentals. The startup concept of BNPL is to enable consumers to make a purchase, without having customers pay anything extra on top of the product price.

QisstPay is one of the startups that has officially unveiled its plan to launch the BNPL service by the end of this quarter. Another startup, Spotii, which has operations in the UAE, is also reportedly launching in Pakistan, and KalPay is the third one. Buy now, pay later essentially solves the problem of cash management for more purchases for consumers which eventually helps merchants get better conversion and sales.

What’s the quantum of decrease in these rates BNPL can bring for merchants? While none of the BNPL startups have officially launched yet in Pakistan to quote hard numbers for increase in sales at merchants that actually occurred, QisstPay claims that their service is likely to increase sales between 10-30% for merchants.

Some industries are naturally going to benefit more from the service than others. Fashion for example. According to an official at a fashion retailer, BNPL is going to be attractive for their brand especially on occasions such as Eid days as there are no payment deferments offered by retailers. “As one goes up in terms of prices, BNPL becomes an attractive option for customers. For example consumer products, or any product that has a price point above Rs5,000,” they say.

“For the apparel industry, when there are occasions, shopping ticket size goes up substantially. Rs20,000-25,000 could be your average ticket size. On that basis, this becomes an attraction for customers to defer payments and potentially shop more products than without the service. Grocery could potentially be a good vertical as well because average ticket size goes up if you buy in one go.”

The idea is simple. If you are a consumer and want that lawn suit that costs Rs5,000 but also do not want to mess up your cash cycle, you can simply choose a service like QisstPay on the checkout page online on the website of the retailer, in-store where you can pay with QisstPay through a link sent to your cell, or at the QisstPay website and mobile application where it will list products of merchants it partners with, while you are making a payment and the Rs5,000 is going to be split up into payments for you. Four in the case of QisstPay (Note: QisstPay says that they would have more installment options for customers but refused to share before they launch).

You’d be required to pay an initial upfront payment, while the remaining is going to be split into 3 monthly installments. QisstPay pays the merchant in full and recovers the monthly installments from you directly. It’s a win-win for everybody.

The scope

But you cannot simply buy anything using QisstPay, for now. The limit for purchases is from Rs1,500 to Rs35,000 for consumers, with bigger purchases that will be coming in the future. The startup, QisstPay, does not run a credit check on you, there’s no ID card required to sign up and the eligibility is assessed through what QisstPay said was their proprietary algorithm. “We are not giving credit or a loan. There is no such underwriting. We are a fund management company that helps people better manage their money,” says Jordan Olivas, CEO at QisstPay.

According to QisstPay, they don’t have to assess creditworthiness; they just have to know if the person is real or not and the ‘secret algorithm’ approves the purchase. “We have the information that they submit to us and we make our decision based on that data.”

When we talk about banks, consumer lending forms a tiny proportion of their overall lending portfolio because of the high-risk nature of such lending which increases the cost of such financing by banks, and makes it further painful and expensive because of the concomitant costs associated with recovering such loans. While a lack of interest on the part of banks to lend to consumers gives a room to players like QisstPay to fill the gap, it also begs a question that why players like QisstPay would be willing to offer BNPL to consumers that banks consider have a high risk of defaults. Banks, by default, have marked low-income borrowers as high-risk and low-income is what Pakistan is with average income for salaried persons standing at Rs18,136 in 2019, according to data from Pakistan Bureau of Statistics.

QisstPay does not assess credit before a consumer’s purchase. So from where does the conviction that consumers won’t default on their payments come?

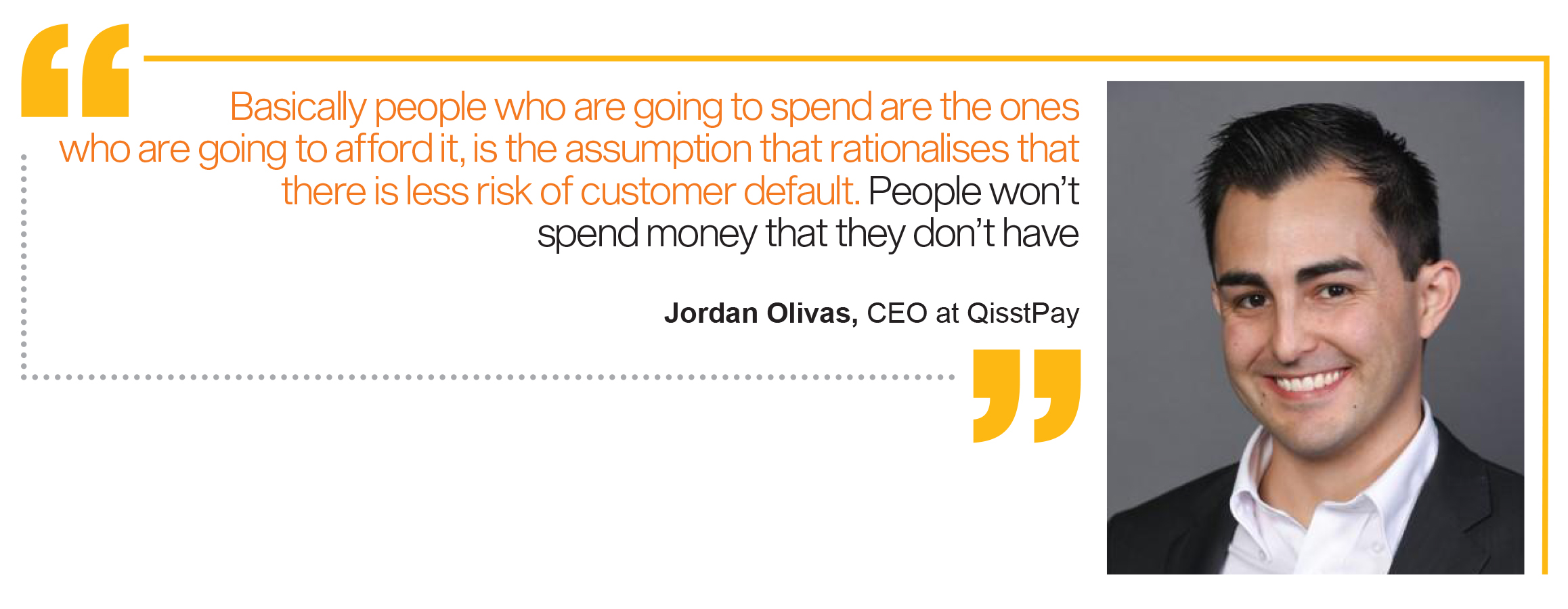

“BNPL is going to help consumers increase spending. What we have noticed based on data is that the only consumers that increase their spending are the ones that do not default. So the ones that default, actually don’t overspend more than what they originally buy anyway. Basically people who are going to spend are the ones who are going to afford it, is the assumption that rationalises that there is less risk of customer default. People won’t spend money that they don’t have,” says Jordan.

“The good customers actually increase their spending and will not be late on their payment,” he claims.

Though the startup said recovery measures were in place, it refused to disclose exact details about it.

Unlike your other financing options like the cash-based traders that require guarantors or banks that have minimum salary requirements and an account with the bank to let you avail the financing facility, QisstPay does not have any such requirements and it does not even charge anything to the customer while he is making a purchase, or even if he is late on the payments schedule. The only penalty a customer would have is that QisstPay is going to block the defaulters account, and he would not be able to make any more purchases unless his outstanding balance is cleared.

“At the end of the day, the average order average is going to be very low and it does not make sense to go on and recover let’s say a shirt. So rather than having a recovery option, QisstPay will nudge the customer to ask if they want to delay their payments. We would do that for customers calling in and asking to delay or defer their payment with no fees instead of trying to recover payments from them,” says Jordan.

That should get one wondering how the service makes money, then? For starters, everything is not on the house and QisstPay is going to charge users an account reopening fee if they are ‘very, very late’ on the payments. But the main income is going to come from charging merchants for the service that now enables them to get better conversion and higher sales.

“It’s a percentage of the sale that we charge to merchants and how much we charge really depends on the vertical the merchant is in. The percentage charged varies from middle single digits to below teen (13%),” says Jordan.

“It really depends on the merchant. What is their volume, order value, what the risk profile of the merchant looks like,” says Jordan.

According to sources, however, the percentages being charged to merchants for BNPL do not make sense from the perspective of making money for the business. Startups like QisstPay are going to be using venture capital money to finance BNPL purchases. QisstPay has so far raised a million dollars and is in the process of raising another venture round, claiming that the new round is going to give them a $30 million valuation from $4.5 million valuation in the previous round.

According to the source, a BNPL service has recently signed a fashion retailer at 6%, which does not make sense from a returns perspective with all the costs associated with running the business. According to the source, it would make sense if the percentage charged is above 10 but would merchants be willing to sign up at 10%?

The fashion retailer Profit spoke to said that even 6% was too high for them. However, as Jordan says, they would be willing to negotiate percentages with merchants which shows their willingness to negotiate smaller rates, at least in the beginning.

All this points towards the typical startup ethos of seeking growth at the expense of profits. UAE-based Spotii has already made an exit worth $16 million this year, after its initial launch in 2019. Perhaps, it would go the same way for QisstPay, after all, according to Jordan, making QisstPay a lucrative business is not his concern right now but growing it is.

An exit, however, does not necessarily mean the service is going to stop. In fact, it could lead to service being available at a bigger level. Spotii’s expansion into Pakistan comes on the back of the exit by the founders of the company.

Some limitations for the growth of BNPL would be that it requires a debit or a credit card that a customer would have to put in the QisstPay application for automatic repayment of the installment obligations. It’s a small number of debit card holders in Pakistan, with unique bank accounts at 66 million for a population of over 200 million. Credit cards are further less. Moreover, most of the merchants in Pakistan prefer to deal in cash. It would be interesting to see if BNPL services are able to get merchants into the digital economy through the allure of better sales conversion on buy now, pay later platforms.

But for the customers that will be able to use BNPL services, it is going to be a jackpot. However, the caveat is that the attraction underpinning BNPL for consumers is that it is going to make products look cheap, and products that look cheap can lead to impulse buying which can add on to the future debt burden.

As BNPL has set the stage in Pakistan, it remains to be seen how consumers will spend. We can only pray that they spend wisely.

The author is a staff member and can be reached at [email protected]

View all articles →Comments

No comments yet. Be the first to join the discussion!