KARACHI: A much-awaited staff level agreement was announced by the IMF on July 13, however, the statement carried dour warnings of significant challenges ahead. Most importantly, Pakistan’s projected external financing needs for FY 2022-23 were $35 billion as per the IMF Staff Report issued in February of this year.

According to data from finance ministry sources, FY 2022-23 will see loan repayments of $21 billion and a projected current account deficit of $12 billion. Coupled with building reserves of up to $5 billion, the external financing needs could be around $38 billion. In his pre-budget press conference, Finance Minister Miftah Ismail said, “we need $41 billion over the next 12 months” to cover the Current Account Deficit and amortisation payments as well as to build reserve cover to three months of imports by end FY 2022-23. But this figure could include payments in the month of June 2022 as well, and may not reflect external financing needs for FY 2022-23.

The statement just released says only that Pakistan faces “higher financing needs in FY23,” implying that this figure is likely to be revised upward by the time the Memorandum on Economic and Financial Policies (MEFP) is released following board approval.

News of the agreement had begun trickling out of government circles as early as the night of July 12. The first reports hit social media and news websites (including in Profit) during the day on July 13, and that same night Ismail took to the airwaves on the Shahzeb Khanzada show to announce that an agreement has been reached on all outstanding issues with the Fund and a formal announcement is expected any minute. By the time the Fund issued its press release all newspapers had already gone to print and were unable to carry the news in their print editions.

The announcement released early morning on July 14 points to significant risks ahead. This was the first working day after the Eid holidays and financial markets saw significant turmoil. Risk premiums on Pakistani bonds skyrocketed, the exchange rate dipped and yields demanded by banks in the first T-bill auction since last week’s 125 basis point hike in the policy rate also climbed relentlessly.

London-based bond traders and analysts tell Profit the spike in risk premium on bonds is not Pakistan-specific but is happening across emerging markets, especially high yield ones, on the back of interest rate hikes by the Federal Reserve as the latest data showed inflation crossing 9% in the United States. Markets expected further rate hikes by the Fed, fueled by a 100 basis point hike by the Bank of Canada on July 13.

Rate hikes in advanced industrial economies suck capital out of riskier emerging markets as investor fly into the relatively safer higher yields on offer in those jurisdictions.

On Thursday last week, these premiums were inching down as confidence slowly seeped back following the Fund’s announcement. Bloomberg reported the Sukkuk maturing in December 2022 rose by to 90.4 to a dollar after dipping to 89.5 a day earlier, while the April 2031 maturity also strengthened by 0.2 cents.

Wednesday, July 13, also saw the exchange rate drop to PKR 211 to a dollar in both the interbank and open markets, dipping by PKR 2.20 and PKR 2.50 in each, respectively. On Thursday both opened at PKR 210.3 and PKR 209.5, respectively.

Yields demanded by banks also spiked on Wednesday in the first treasury bill auction to be held since the policy rate hike of last week. Profit carried that story earlier.

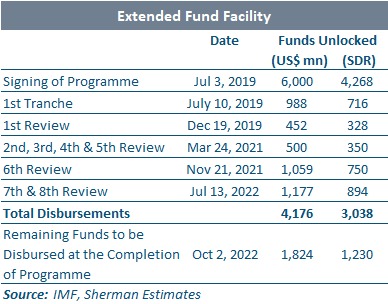

As the Fund programme moves towards resumption, the schedule of disbursements has been revised to reflect the possible extension till June 2023 as well as a possible enhancement of disbursements by $1 billion.

From Sherman Securities

The Fund statement points towards both domestic as well as global pressures for why Pakistan is in need of a bailout.

“A difficult external environment combined with procyclical domestic policies fueled domestic demand to unsustainable levels,” it says. The prolonged period of negative real interest rates, that had to be unwound in a rush via a 775 basis point hike in the policy rate since November 2021, provided a strong impetus to growth but also gave rise to pressures on the external account that depleted the foreign exchange reserves and placed great pressure on the exchange rate.

“The resultant economic overheating led to large fiscal and external deficits in FY 2021-22, contributed to rising inflation, and eroded reserve buffers,” says the statement.

Going forward the government is expected to return a primary surplus of 0.4% of GDP in its fiscal balance by the end of FY 2022-23, which will require strong revenue performance as well as tight expenditure control. Stemming the continued growth in the circular debt, expected to see a flow of PKR 850 billion in FY 2021-22 according to the Fund statement, is another priority singled out for mention. It also calls for “proactive monetary policy” which responds strictly to inflation and “greater exchange rate flexibility”. The staff report from February 2022 pointed specifically to interventions in the foreign exchange market. “The volume and frequency of FX intervention and other administrative measures have been increased to manage the FX market as current expansionary macroeconomic policies led to heightened depreciation pressure on PKR in 2021,” that report said.

Once the programme resumes in earnest following board approval, the practice of import restrictions via bans and cash margin requirements as well as administrative processing delays will need to end. The State Bank will need to acknowledge the higher yields demanded by banks in T-bill auctions as a market reality rather than an avaricious practice to be stamped out. Power and gas tariffs will need to rise sharply to curtail the continuing flow of circular debt. In short, more interest rate rises, further currency devaluation and higher utility bills await the business community as programme implementation gets underway in earnest.