Cement Sector: Upward growth trajectory to continue on the back of CPEC

The cement sector over the last six years and the industry itself has seen a growth in volume every year something that is also reflected in the huge return on investment cement stockholders have enjoyed. Considering the heavy investment the Chinese have made in Pakistan with the China Pak Economic Corridor (CPEC) and the barriers to entry for new entrants it seems the growth will continue for few more years to come. We spoke to Maple Leaf cement CEO and All Pakistan Cement Manufacturer Association (APCMA) Chairman Sayeed Tariq Saigol for his view on the industry as a whole going forward.

Profit: How do you think CPEC could play out for the local cement industry?

SS: While I am not sure in terms of the quantity of cement that would be used, the perception of CPEC is very positive. It’s a good story. Everybody is excited about it. I see the general activity in the market increasing because of this perception; indirectly, because of the sentiment that CPEC creates.

If you talk to anybody today, they are talking about CPEC even if they have nothing to do with the construction industry. They are looking at CPEC for property prices rising and influx of people. Even the foreign fund managers, globally, are looking closely at CPEC. I met someone from England the other day who runs a fund and he was very positive about Pakistan. When I talked to him but about terrorism and all, he said that yes those are all valid problems but the CPEC story provides a very positive outlook.

Also China has to make an example of this CPEC route in Pakistan for them to be able to move forward in other countries. If they fail here, then the future is in question. So it is very important for China to prove this as part of their global strategy.

Profit: There is skepticism that under CPEC, our imports would increase and some Chinese cement companies will enter the Pakistani market by acquiring a smaller manufacturer like Dewaan Cement and introduce price competition that has somewhat been missing from the cement industry and reduce the margins. In other words most of the benefits would accrue to the Chinese companies as opposed to the Pakistani companies. What do you think?

Profit: There is skepticism that under CPEC, our imports would increase and some Chinese cement companies will enter the Pakistani market by acquiring a smaller manufacturer like Dewaan Cement and introduce price competition that has somewhat been missing from the cement industry and reduce the margins. In other words most of the benefits would accrue to the Chinese companies as opposed to the Pakistani companies. What do you think?

SS: To address the cement part specifically even if a Chinese cement company comes, the CPEC project will buy from whatever cement plant is closest to them along the route. Freight cost is a very big element in this picture. So if they acquire the Dewaan plant in the South for example, which is ‘Saadi cement’, instead of the ‘Pakland plant’ in Karachi then Saadi cannot supply goods to a project that is taking place in Baluchistan. Those goods will have to come from a plant that is closer to them - they just won’t be competitive.

I am also not that worried about a Chinese player coming here or a local player who is expanding because the sites on which you can expand now are limited. There are limited sites for new plants. So whether that comes from an international player or whether that comes from a Pakistani company I think that is going to be part of the normal expansion that is going to take place.

Profit: The last five years have been exceptional for the shareholders of Cement companies especially that of Kohat and Maple leaf. However it seems the ‘Bull-Run’ has finally ended. What should the shareholders expect going forward and why?

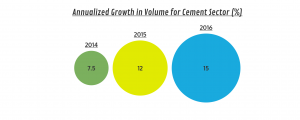

SS: Growth has been good in the past couple of years; it has been increasing every year. Three years ago we saw 7.5%, then 12% and this year we are looking at upwards of 15% growth (annualized growth in volume averaged out for the country).

As the utilization of the industry is going to go up, obviously the profitability of the industry will go up and as a result the returns to shareholders and markets will continue to go up, at least for the next two years.

Profit: You expect further growth even though there are plans of cement companies to add further capacity which could reduce utilization of current plants?

SS: First of all the moment that a plant decides to expand, it will be at least 30 months before they can get into fully commercialized production. If you look at it right now, there are two plants coming up in the South, but there are no other plants in the pipeline even though some companies have announced plans to install new plants.

However there is a big difference between announcing plans and the ground work actually starting. There are a lot of issues like land availability, leasing problems and difficulty raising capital, just to name a few. Therefore not all plans to install new plants will be executed. Secondly, there is a high potential for the growth rates to continue.

So some plants in the local market will expand and part of that expansion may be from a foreign player but so long as the growth rates continue then I think in a two-year or three-year cycle there shouldn’t be any major issues.

However in a longer period, say a five-year cycle it is difficult to predict because every commodity business will have a down cycle. I have yet to see that not happen. So there will be a down point in the cement side also. That could be because of consumption, or capacity or whatever that may be. But I don’t see that downside coming before three years.

Profit: Considering that there is limited possibility for new leases and licenses, do you think that if a new player comes in it will be through acquisition?

SS: Acquisition will be the approach for a new player to enter the market. For them to secure a new site the will have to work with the government in the land acquiring process, which will take a very long time and as I mentioned there is not a lot of availability of sites.

I think that current cement players are also having problems in expansion because apart from issues with land availability there are now environmental concerns as well that the government is taking very seriously. The Kallar Kahar and Chakwal area for example may not ever have another plant due to the impact it will have on the environment.

That leaves some parts of Central Punjab and certain parts of South Punjab. Expansion in Hattar and Islamabad area, for example where the Fauji cement plant is, will also be very difficult because that area is going to be part of the new airport there as Islamabad expands.

Existing cement plants in the area are having difficulty because the government is asking them to curb production as the area is becoming increasingly populated.

Profit: In the recent past the cement sector has increased its reliance on local consumption. Why is that the case and should we expect to see the same trend in future?

SS: There has been growth in the country resulting in increased demand and consequently increased utilization in the local market. There has been a reduction in exports as well which is largely driven by the fact that the areas where we were exporting as a country have new cement plants coming up.

So the reduction in Afghanistan market has a lot to do with Iranian cement flowing in there; reduction in East African market has a lot to do with new cement plants coming in the East African market. Same is the case with Iraq, which used to be a big Pakistani cement importer has over the years become self-sufficient with new cement plants becoming operational.

Profit: In that case how is Iranian cement cheaper in Afghanistan than Pakistani cement?

SS: There are parts of the Afghanistan market which are more competitive for Pakistan, such as Kabul area and certain other parts. But if you go towards the side of Pakistan border with Afghanistan i.e. Chaman area, there it is closer for Iran to come in. So it is a logistical play.

Similarly Pakistani cement going through Wagah to Amritsar and Haryana areas is cheaper in terms of freight. Even though India has 30-35 per cent excess capacity today, it is still not feasible for them to bring goods from the South where all the limestone is and deliver it to areas closer to Wagah. So freight is an integral part in the radius in which you are selling cement. Therefore a plant in Iraq will surely make exports disappear for us.

Profit: Back on the domestic front, is there any fear of cheaper Iranian cement flooding its way into the local market, perhaps through smuggling given how our own cement is relatively expensive because of government duties?

SS: Everything that is locally manufactured in Pakistan has certain government protection, whether it is cement, pipes or furniture. But I think that Pakistani cement industry is still quite competitive. Smuggling however is something that you cannot do much about, it’s a different ball game altogether. The pricing doesn’t really fit into the picture and this is also true for fertilizers, cement, oil and diesel.

That being said, smuggling is not that big of a problem as it is not happening on such a large scale. As soon as CPEC routes start becoming operational the closest cement plants are going to be from Pakistan. Iranian cement will also be limited to the smuggling aspect, because by bringing cement through legal channels they would have to go through Karachi and their goods have to be cleared, and that involves paying clearing charges and duties. So when all that is added, the Pakistani cement will always be more competitive.

Profit: Do you think that there is anything that the government can do with respect to export of cement?

SS: Cement manufacturing globally is a localized business. Anywhere in the world where exports and imports take place, they are temporary and only fill a gap. Japan used to export to America but that was for a specific time period. So export of cement can only take place in times of shortage. So if there is a shortage in Pakistan for CPEC then Iranian cement can flow in.

Profit: We are told that cement industry is one of the most competitive industries in Pakistan and it has significantly reduced the cost of manufacturing, especially in energy, how did this happen?

SS: In Pakistan lot of cement plants have put up wastage recovery plants, which capture all the excess gases that would otherwise go out into the air. Their heat, which is very low heat, is captured and converted into usable electricity. Initially there was no technology to do it, in the last 10 years this technology has come in. We recover around 16MW of power from it. Many cement plants have doing that which is the major reason for the energy efficiencies that cement plants have had. Although it costs around Rs 3,000 crore to set up such a wastage recovery plant, the return is very good and there are no running costs, just the one time capital expenditure.

Profit: The industry came across higher FED (Federal Excise Duty). What has been the impact on prices and volumes?

SS: The argument made by the cement association has been that cement is not a luxury good so excise should be reduced. There have been moments with various governments where excise duty had been reduced and then there were moments when due to budget deficits and bigger economic concerns that excise duty was increased.

But I think cement prices have generally been quite stable in the past two-three years and have actually reduced a little bit despite the increased excise duty, because the cement industry has worked a lot for cost reduction, vis-à-vis wastage recovery plants. So part of it was absorbed and part of it went into the market. I think that the current price levels don’t have that much effect on a consumer, a person building a house or a factory.

Cement is a very small proportion of the total project cost; therefore even though the government has increased the duty and the price increases by 10-15 rupees a bag as a result, it does not affect the demand.

Profit: Even though the industry is competitive and coal prices globally are not that of 2008 prices in Pakistan are still on the rise, why is that so?

SS: If you look at the last twelve months, the cement prices have been coming down. There are also large price variations in different markets. In KPK the price levels are maybe 10-15 rupees lower than Central Punjab.

In Karachi prices are higher than in Lahore. This is because of lot of cement plants that came into production over the past decade were more concentrated towards Rawalpindi, Chakwal, Hattar and other areas of Islamabad. That expansion led to excess capacity there making the region more competitive and cheaper than the South.

So I think that generally the prices will remain stable unless there is a shortage. If there is a shortage then prices go up. But I don’t see prices going up because utilization is going up and people are expanding their market share.

Profit: Cement companies are not known for advertising, such as paint companies who advertise heavily even though that is also a commodity. In your industry how does one decide between different brands, what differentiates your brand considering that prices are similar?

SS: There is a lot of difference in prices. Today I am 15 rupees more expensive than my second competitor. If you go to the market and you get Maple Leaf, it’ll be more expensive because we are a premium brand.

I think every company has their own marketing strategies in place, I cannot speak for others in the industry but my view is that most of the brands have been established on historical basis. I don’t think that the industry has been heavily engaged in branding activities to differentiate themselves in certain ways.

For example the only two cements that used to come in the market pre-privatization in Lahore and Islamabad were Zeal Pak and Maple leaf. Both were owned by the government but after privatization, Zeal Pak closed down and Maple leaf remained. This is how our historical value has been built. In Rawalpindi Maple Leaf will be one of the cheaper brands, because historically Fauji cement and Askari Cement Limited (AWT) have been selling there.

Maple Leaf has spent a lot on branding but all our branding is below the line, on distribution level. We have a value chain and we think our value chain starts from the truck driver to the mason, because this is the decision making chain, the logistics chain and the supply chain.

But there are no tricks of the trade. People do try to gain market share and that is why there are different prices in different markets and various people have different strategies for marketing, but it is all primarily on the basis of price differentiation.

Profit: As per reports cement companies keep their margins high by having a quota system. Also there are reports that most companies are running idle capacity which gives the perception that there is a cartel. How would you respond?

SS: That is something that I cannot comment on but I can give you an indicator to look at. There are big pricing gaps and differentials in different markets. In the last year and a half the cost increased, excise duty increased but the cement industry was not able to pass that on fully, some regions were able to do it more, other regions much less.

Then if you look at the utilization of cement industry, plants are operating from 60 per cent utilization all the way to 102 per cent utilization. So these are things for a judgment call that people have to make.

Profit: If there is no as such cartel then why is it next to impossible to get a new license even though Pakistan has a huge potential of Limestone? Especially for those who do not have an existing stake in the industry?

SS: There is no license that is required as such. If you go today to apply for a lease in Punjab, and I’m told in KPK as well, for a new site, it is not as straightforward as the provincial governments are now looking to put in place a new, stricter leasing policy for all mines and minerals. In the past you could just go and apply and get a lease. This is not limited to just limestone, rather all minerals.

The Punjab government is working on a strategy to revamp how leases will be given out in the future. It is not a barrier to entry, they are just in the process of making these rules and regulations about how leases will be allocated, whether there will be a bidding process for them, how long you have to use the lease for etc.

People took coal leases all over Punjab as you know and nobody has done anything with them. There are only donkeys and carts taking mining there. So I think that the government wants to make a regulatory framework of how leases will be used. Mineral is the wealth of the state and it has to be utilized at the most optimum level.

The second perspective is that over the last couple of years and especially under the current government, the environmental damage that can be caused by mining is being very seriously considered. So now there is a whole thought process behind it and it just cannot be a free-for-all scenario like before. New cement plants can come and will come but I don’t think that it’s going to happen tomorrow.

It is not as such good news for players already in the market either. Will they be able to renew their lease or what basis would be needed for renewal, will they be able to expand or acquire new land, and these are all valid questions now. So the government is trying to regulate not just the cement industry but the whole mining and mineral industry.

Profit: Please tell us about the future plans of Maple Leaf Cement, and of the decision to set up a 40MW coal-fired power plant.

SS: The 40MW plant is going to come online in just under 12 months. We have already announced in our last board meeting that we are looking to expand out cement capabilities. We are working on it and right now we are looking at maybe another plant of 7,000 tons per day, at the existing site. So right now we are in the process of evaluating it and studying it. We haven’t started the construction as yet, but we are in the final stages of evaluating it.

Comments

No comments yet. Be the first to join the discussion!