U Bank appoints new CEO as financial report delay lingers

Mohamed Essa Al Taheri replaces Kabeer Naqvi as the acting President and CEO of U Bank

KARACHI: In a surprising turn of events, on October 18, it was announced that Kabeer Naqvi, CEO of U Microfinance Bank (U Bank) had resigned. The next day on October 19, according to a press release by the bank, Mohamed Essa Al Taheri was announced as the acting President and CEO of U Bank.

Al Taheri has been associated with U Bank as a member of the Board of Directors and worked with e& Group as the Group EVP Financial Policies and Systems. He holds a master’s degree in International Business from the University of Wollongong, Dubai, and brings over 20 years of professional experience from working with HSBC Bank, Dubai Commercial Bank, and the Development Board of Dubai Government.

The appointment of Essa Al Taheri comes soon after the resignation of Kabeer Naqvi, who earlier held the position of President and CEO of U Bank. He had been associated with U Bank since 2015.

However, according to multiple sources in the microfinance industry, Naqvi was forced to resign. They claim, U Bank’s board of directors had also asked the upper management to resign as well, due to concerns over the CEO's aggressive expansion strategy and alleged artificial growth tactics. However, a source privy to the industry, disclosed that the resignations were later retracted on the announcement of the new management.

When Profit contacted Naqvi for a comment, he said he “was leaving on his own accord” and that he “will be joining his family in Chicago.”

Profit reached out to Misbah Naqvi, a member of the board of directors of the bank but she declined to comment. Profit also reached out to other members of the senior management but received no response.

Delay in publication of financial statements

The latest period for which the financial statements of U Bank are available is the first quarter of the calendar year 2023 during which it made a profit of around Rs36 crores.

Following this report, no financial statement have been released. Usually, banks release first-quarter reports of January to March in late April or early May, half-yearly reports of January to June in late August or early September and third-quarter reports of July to September in late October or early November. Annual reports are usually released three months after the accounting year's end, as the reports need to be audited which takes some time. Sometimes, banks do not release their reports according to these timelines if there have been excessive losses.

In fact, U Bank has a history of delaying releasing financial statements. The 2023’s first-quarter reports were released in July. The annual report 2017 was released in June 2018, six months after the accounting year ended. The third quarter report for 2022 was released in November, a little over the normal timeframe.

Since the microfinance bank has not released the reports for the second quarter of 2023, and now it is time to release the third quarter’s report, there is speculation amongst the microfinance industry that the bank has experienced significant losses.

According to a source in the microfinance banking sector, U bank's financials presented an overly optimistic picture of the company's performance. One example, as quoted by a source privy to the matter, was regarding the implementation of IFRS-9. The bank classified a significant portion of its Covid-era rescheduled portfolio under stage one of the expected credit loss model which implies that there was no significant decline in credit quality. However, according to source, the classification was erroneous as the recoverability of these loans was contentious and the management was aware of the fact.

U Bank’s strategy

Unlike other big telecom-based microfinance banks (Telenor Microfinance Bank and Mobilink Microfinance Bank) that had set their sights on branchless banking, U Bank took a more conventional brick-and-mortar strategy.

Naqvi had been spearheading an ambitious campaign to open new branches in urban cities like Karachi, Lahore and Islamabad. In a previous interview with Profit in June 2023, Naqvi said, “We did not try to turn it into a telecom company. We said that this is a bank, and its mission is microfinance. Just like a bank, its balance sheet will grow. It will have liquidity, strong cash reserves, a treasury function, Islamic banking, digital banking, and even conventional microfinance. It will also have an urban unit responsible for deposit mobilisation. If all these elements are in place, (only then) will this institution thrive and last for the next hundred years”. These new branches were essentially to bring in low-cost deposits.

The deposits did increase but the bank mostly attracted high-cost deposits from other banks and firms. These deposits are not sticky.

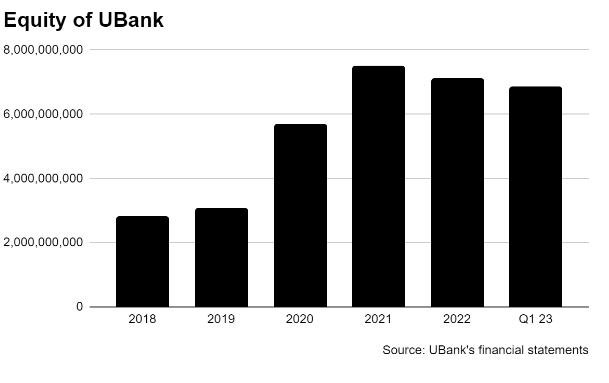

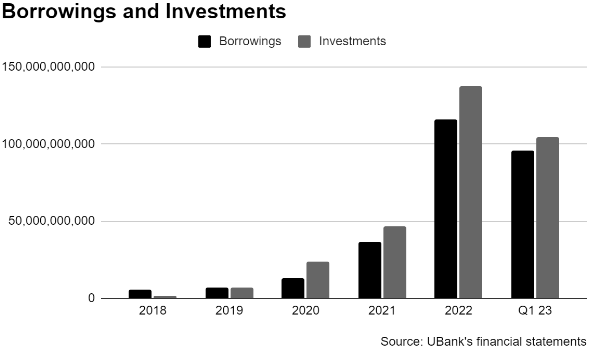

Moreover, in 2022, U Bank’s balance sheet increased by three times. U Bank used its deposits to purchase money market mutual funds (MMFs) or government securities (T-bills). Then, it pledged those very PIBs to the same banks or even a third-party bank, allowing U Bank to borrow additional funds through repurchase agreements with a small margin. With the borrowed money in hand, U Bank repeated the process of purchasing more Tbills. This cycle continued, spinning a web of financial maneuvering so much so that while the size of assets increased from Rs 10,458 crore in 2021 to Rs 22,130 crore in 2022, net assets have declined from Rs 749 crore in 2021 to around Rs 709 crore in 2022, a decrease of Rs 40 crore.

In other words, it became a highly leveraged bank, as it had accumulated a lot of government securities. In case of change in interest rates, the bank could have incurred significant mark-to-market losses. According to a source, the board had concerns over the aggressive expansion strategy and alleged artificial growth tactics.

The author is a business journalist and a member of the staff. She can be reached at [email protected]

View all articles →44 Comments

No comments yet. Be the first to join the discussion!