Could PMEX transform the Pakistani farm for the better? Maybe

The commodities exchange could change the way farmers raise capital and the way agriculture is conducted in the country, but it needs the supply chain infrastructure to catch up

In the heart of downtown Chicago stands an imposing art deco skyscraper that houses an institution perhaps more responsible for turning the United States into an agricultural powerhouse than any other: the Chicago Board of Trade building, which houses the trading floor of what is now known as the Chicago Mercantile Exchange (CME).

Although commodities trading has been around for a long time – indeed, the first written records of human civilisation are those of forward contracts for the delivery of grain at a future date – the Chicago Board of Trade (CBOT), founded in 1848, was the first organised commodities exchange in the world that still exists to this day. Since its merger with the CME in 2007, it has been the largest commodities trading exchange in the world.

So, what exactly is a commodities exchange, and why is the one in Chicago so important to the economic development of the United States? And can the Pakistan Mercantile Exchange (note the similarity in the name to US exchange) serve the same role for Pakistan? The PMEX management certainly seem to hope so and are working to help make that happen.

How futures contracts work to hedge risk

Commodities exchanges allow farmers to manage one of the biggest risks they face in their business: that of commodity prices. If a farmer is planting cotton and expects to reap the crop in the next three to four months, they need to be able to have some sense of how much money they can expect to get for their crops.

A futures contract allows a farmer to promise to deliver a specific quantity of an agricultural commodity (for example, rice), of a specific breed and quality (say, Irri-6 at 85% unbroken), and a specific time and location for delivery. The farmer pays a small cost for the contract, but in exchange gets the certainty that they will be able to get an exact price for their product.

Why does that matter? Because if a farmer has certainty about revenue, then they can raise financing to invest further in their land (better seeds, fertilisers, pesticides, etc) and production equipment (tractors, harvesters, etc.) against their future cash flows. This can make all the difference in the world for farmers, both in terms of the productivity of their land and, by extension, their own incomes.

Of course, this arrangement is not without its risk to farmers: prices could go up during the growing season, which would mean that the farmer would lose out on the potential upside. However, that is usually a trade off most farmers are willing to make in order to protect against the downside risk.

The bigger risk is natural elements – floods, droughts, pests, etc. – that can devastate a crop. The futures contract protects the farmer against price changes, but also obligates the farmer to deliver a specific quantity. If part of the crop is damaged, or yields are unusually lower, the farmer is still legally obligated to buy the crop – probably at a much higher price – from the open market and ensure delivery.

To protect against such eventualities, most developed country have some form of crop insurance, usually at least partially subsidised by the government, which protects farmers in the event of natural disasters.

Why commodities exchanges are needed, especially in Pakistan

As stated earlier, one of the biggest reasons why commodities exchanges can help farmers is because they allow them to have predictable cash flows against which they can raise financing. And while these exchanges help farmers in every market, they could be especially useful in the Pakistani market, with a more limited universe of lending options for farmers.

One of the options that farmers have in order to secure financing is to borrow against the value of their land, which is typically worth several times their annual cash flow needs. In theory, this should be easy for farmers to do. However, in practice, this ends up being quite difficult.

“An average, B-grade acre of land costs about Rs1 million in my area,” said Ghulam Mustafa Chaniho, a farmer based in Khipro, in Sanghar district in Sindh. “But banks are not willing to lend anywhere close to that. They lend at the value of the land that is registered at the provincial revenue department which, like everywhere else in Pakistan, is much lower than the actual transaction value. For that acre which would cost me Rs1 million to buy, I can get maybe a Rs40,000 loan against it.”

In other words, the banks are far too conservative in their lending to farmers, as a result of which, agricultural lending in Pakistan remains abysmally low, considering the fact that agriculture itself accounts for over one-fifth of the size of the Pakistani economy.

Yet, if farmers were able to secure their revenues through buying commodities futures contracts, and further securing their risk through crop insurance, it is entirely possible that banks would be more willing to lend to them against their future revenues, which would fundamentally expose the banks not to the farmers as their counterparties – which they evidently want to avoid – and instead commodities traders and financial institutions, which are likely to be a more acceptable credit risk for the banks.

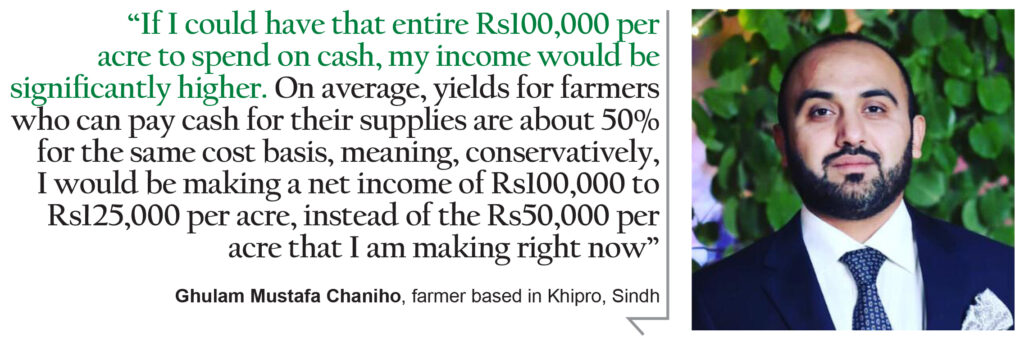

“On average, for one acre of land in my area, for the crops that I grow, my costs are about Rs100,000 per acre, and my revenues are about Rs150,000 per acre,” said Chaniho. “Right now, I spend that entire Rs100,000 on credit and pay back when my crops are harvested. But what that means is that I cannot always get what I want. So, for example, my land might need more potassium fertiliser instead of urea, but the supplier who gives me credit only has urea, which means that is the only fertiliser I can use, even though it will result in lower yields than if I could use potassium fertilisers.”

“If I could have that entire Rs100,000 per acre to spend on cash, my income would be significantly higher. On average, yields for farmers who can pay cash for their supplies are about 50% for the same cost basis, meaning, conservatively, I would be making a net income of Rs100,000 to Rs125,000 per acre, instead of the Rs50,000 per acre that I am making right now.”

In other words, there could be a massive improvement in farmer and landowner incomes, which in turn would spur growth in the entire rural economy and the wider Pakistani economy as well. Food production would go up, and food prices would come down as a result. Better cash flow would mean greater agricultural productivity increases, and agricultural water consumption would go down as more farmers switch to drip irrigation instead of flood irrigation.

All of this would be enabled if the market for local agricultural commodities’ futures contracts would take off.

PMEX and its business model

But while these domestic commodities contracts exist, currently, the overwhelming majority of contracts traded on the Pakistan Mercantile Exchange have nothing to do with Pakistani agriculture. Indeed, measured by notional value of the contracts (not the same as the actual amount of cash trading hands), the most traded derivatives contracts on the PMEX are equity indices, which amount to bets that speculators make on the direction of the benchmark KSE-100 index, the index that tracks the level of stock prices listed on the Pakistan Stock Exchange. Equity indices account for half of the entire notional value of contracts traded on the PMEX.

Notional value refers to the full economic value of the contract. For example, let us suppose that a farmer buys a wheat contract to deliver Rs1.5 million worth of wheat at a specified time and place. The farmer will buy that contract for probably something like Rs15,000, and the commodity broker who arranges for that contract will get a small portion of that Rs15,000 as a brokerage fee, probably in the range of Rs150 or less. And PMEX will make a small portion of that Rs150 commodities brokerage commission.

The above numbers are for illustrative purposes only and actual trading numbers could be vastly different. But it tells you just how big the notional value can be relative to the amounts of money actually trading hands on the PMEX.

For the fiscal year ending June 30, 2019 – the latest period for which financial data is available – the total notional value of contracts traded on the PMEX was Rs2,912 billion, up 102% compared to the previous year. Yes, you read that correctly: the volume of trading on the PMEX doubled in one year.

The trading of equity indices suggests that the PMEX is moving from being just a commodities exchange to full fledged derivatives exchange. A derivative is a financial instrument whose value is reliant on the value of another financial instrument, such as equity indices contracts, whose value is derived from the value of the KSE-100 index, or other similar indices.

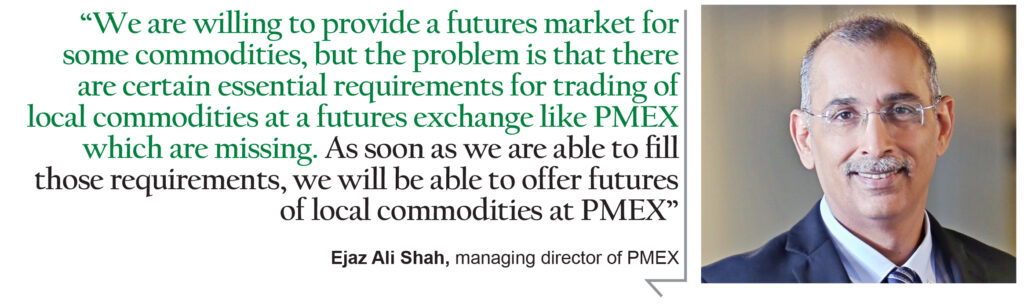

This is not to say that commodities trading is not a large and important part of the PMEX trading volume, But the vast majority of the commodities traded on the PMEX are international commodities. “These markets are global markets. Since the commodities-based futures traded at PMEX are global in origin, PMEX has no option but to be a price-taker,” said Ejaz Ali Shah, managing director of PMEX, in an interview with Profit.

However, Shah explains, in some commodities such as the red chili, Pakistan is a major global producer and its prices can move the global market. PMEX offers traders the opportunity to trade domestic red chili futures contracts.

Why not have more local commodities trade on what is Pakistan’s largest commodities exchange? (Technically, it is not the oldest, since the Karachi Cotton Exchange, founded in 1933, does allow for some form of cotton trading, albeit a very rudimentary form.) The problem is not with the PMEX or with a lack of interest in trading local commodities. The problem is the infrastructure necessary to trade local contracts.

The infrastructure problem

Shah explains: “There are stages related to agriculture value chains which need to be in place before futures based on a wide-range of local commodities can be offered at an exchange like PMEX. A very simplistic question I am often asked is how come local commodities like rice and grain aren’t traded. In order to have a vibrant futures market, you need a well-developed spot market with the proper agri-value chain in place.”

If you take one look at the spot markets in Pakistan and compare them with the rest of the world you would see that they are almost as primitive as the first spot markets to have existed. “Our spot markets need a lot of improvement at the moment as in terms of infrastructure, processes and value-chain linkages as they are quite primitive,” notes Shah.

What is the spot market? It is the place where traders go to buy agricultural commodities directly from farmers and it is called a spot market because the commodities are bought and sold ‘on the spot’, at prices determined there and then. That then begs the question: what is missing from the local spot markets?

The problem, as with most things related to economic activity in Pakistan, is the lack of an infrastructure that allows people who do not know each other to trade with each other in a manner where both parties can be mutually assured of an honest trade, and contract enforcement in case there is a problem.

One critical piece of infrastructure that is missing from the current Pakistani markets: collateral management, something that the government is seeking to address by setting up a collateral management company (CMC).

“The idea is to register warehouses and make them adhere to standards set by the CMC based on specific product requirements,” said Shah. “This would help in assuring that standardisation is introduced in Pakistan for warehousing of agricultural commodities.”

In other words, if I am buying a ton of basmati rice, I want to know that it is basmati rice and not the lower grade Irri rice. And if I ask for 95% whole grain, I want some assurances that it is 95% whole grain and not, for example, 85% whole gain and 15% broken grains. And while we are at it, I would like some assurances that the grain is clean and does not have insects crawling all over it.

The collateral management company, currently in the process of formation, would help address these standardisation concerns. Each batch of agricultural commodities that would be brought over to the CMC’s warehouses would go through a quality check process, and – once quality and quantity has been verified – the CMC would generate an electronic warehouse receipt (EWR).

“Once [verification is] completed, they [CMCs] will generate electronic warehouse receipts (EWRs) that will be issued and traded at PMEXs platform,” said Shah. “The mechanism for EWR will be a game changer in revolutionising the agriculture landscape of the country. It is expected that it will reap myriad benefits for all key stakeholders.”

He explains: “First, it would enhance farmers’ access to agricultural credit and improve their profitability. Second, it would help the government in documenting the agricultural sector resulting in enhancing the tax-net, grading and standardisation of commodities, reducing post-harvest losses and improving the country’s food security. Third, it would help banks in mitigating risks by allowing agricultural commodities as an alternate collateral. Fourth, it would encourage investors to set up high-standard warehouses throughout the country. Lastly, this mechanism would also play an imperative role for PMEX in materialising its vision of bringing trading of all local agricultural commodities on its platform and showcasing them to the international market.”

Warehousing and standardisation of commodities, in other words, are a necessary precursor to a vibrant commodities market. Shah called these two the “building blocks which are essential for the future of local commodities”. He notes that without the correct integration of these two, a vibrant local commodity market cannot exist. “Once these are in place, only then will the futures exchange be able to perform as a futures exchange for local commodities.”

In the absence of these two ingredients, PMEX has found its efforts to introduce trading of local commodities lacking traction. “We are willing to provide a futures market for some commodities, but the problem is that there are certain essential requirements for trading of local commodities at a futures exchange like PMEX which are missing. As soon as we are able to fill those requirements, we will be able to offer futures of local commodities at PMEX,” said Shah.

Shah said that the PMEX does not want to serve primarily as a market for international commodities, which is what it is today. He said that the purpose was to bring local commodities on the exchange platform. “We are working very hard. We’re working with anyone who is supportive. We understand that the exchange will eventually get its spark from the local commodities which will help PMEX realize its true potential.”

Speaking on the potential, “We are a country that produces a lot of commodities, some of the finest qualities in the world. All we need is a proper infrastructure to manage these commodities. What we can provide is a market, local and international for these commodities. What is required is packaging, processing and marketing of these commodities to both local and global customers.”

In order to tackle and address the shortcomings, the PMEX is moving on two tangents. While some commodities need packaging and processing, they also need a market. As a result, the PMEX developed a two-pronged strategy. “On one hand, we are all set to play our due role in the recent initiative taken by the Government of Pakistan for establishing the mechanism for trading of Electronic Warehouse Receipts (EWR) for the development of the agricultural sector in the country. On the other hand, we are working a Global Trading Platform (GTP) which will showcase Pakistani commodities to the global audience.”

The Alibaba of Pakistani commodities?

That last bit about the GTP is something that is unusual in the world of commodities exchanges, and is an idea that is inspired less by its peer exchanges in other parts of the world and more by Chinese e-commerce platforms, specifically, Alibaba.

“In essence we’re trying to set up the Alibaba of commodity trading,” said Shah. “You can be sitting anywhere in the world and you can get onto our portal. That’s the idea basically.”

He explained that the GTP will showcase local commodities of the country to the global market by offering foreign buyers the ability to purchase agricultural as well as non-agricultural commodities with convenience and confidence of quality assurance in accordance with international standards. The GTP will cover: trading, storage, packaging, transport and export of the commodities with accessibility as convenient as a click of a button.

PMEX envisages that GTP will transform the local commodity markets by linking farmers directly to the international market, improve price discovery and induce transparency in the commodity value chain, reduce transaction costs and increase Pakistan’s agricultural exports.

“We feel international buyers will prefer PMEX which is a national institution guaranteeing quality, by playing the role of a Central Counter-party (CCP). The buyer doesn’t have to do due diligence if he/she is a new buyer. If you’re an old buyer the cost will be less than an exporter because the middle man is removed. Bringing sellers and consumers closer would enable both to get a better price,” said Shah.

One problem the company might run into with this business model: commodities traders who export Pakistani agricultural commodities are likely to be some of the PMEX’s biggest clients on the domestic trading side and will not like seeing the exchange effectively setting itself up as a competitor on the export side.

Managing Editor, Profit Magazine. He can be reached at [email protected]

View all articles →2 Comments

No comments yet. Be the first to join the discussion!